For economic commentary and analysis, go to the Bonddad Blog

CBS Marketwatch wrote a story over the weekend titled, "Will Lemming Loans Drive US Economy Off the Cliff?" The story highlights the basic problems created by the current mortgage market. If all of the predictions below come true than we are in some serious trouble. However, I think the more likely scenario is some of the possibilities below will come true partially, meaning the mortgage market won't crash, but will instead limp along for longer than we would like.

First, let's highlight the basic problem which is the continual increase in higher risk loans.

What this diagram demonstrates is over the last 5 years, the number of higher-risk mortgages has increased each year. For example, in 2001 subprime and Alt-A (which is essentially one step above subprime) comprised roughly 10% of new mortgage loans. By 2006, that total had increased to about 40%. In other words, 40% of new loans in 2006 were made to borrowers who were considered higher risk.

Another way to look at this situation is the number of qualified lower risk purchasers were probably already homeowners by roughly 2003 - 2004. The main borrowers who were left were higher-risk borrowers with lower credit ratings. This would partially explain why the number of higher borrowers increased over the last 5 years -- they were the only ones left to loan to.

The article is partially based on a report from Credit Suisse titled, "Mortgage Liquidity du Jour".

Let's look at three areas that the subprime/mortage shakeout will impact:

Increased inventory

More than 1 million families will lose their homes in the next few years, by one estimate. Another study predicts 2.2 million foreclosures.

First, note that these are estimates. In reality, we have no idea how many homes will be added to inventory. I have seen estimate from 500,000 to 1 million. Personally, I think the 2 million is a bit high. However, what does matter is the inventory of homes available for sale will increase.

At this point it's important to note the total available inventory available for sale has increased since last year. According to the National Association of Realtors, the total inventory of homes available for sale was 2,985,000 in February 2006 and 3,748,000 in February 2007, or an increase of 25%. That's a lot of inventory to sell. And this is at a time when the number of purchasers is decreasing.

Econ 101: increasing supply = lower prices.

A Shrinking Pool of Buyers

Tougher mortgage underwriting standards will eliminate about 20% of the potential buyers, including 50% of the subprime buyers and 25% of the Alt-A buyers, according to estimates by Credit Suisse.

20% of the market will go away because purchasers can't get a loan. Tightening credit standards will disproportionately impact the subprime market. Considering the number of subprime/Alt-A loans has increased from 10% of total new mortgages in 2001 to 40% in 2006, the tightening could impact the housing market fairly severely.

Econ 101: few buyers = lower prices.

Prices

So far we have increased inventory from the increase in foreclosures, an already high level of raw inventory and fewer buyers from tightening credit standards. All of these will work to lower prices.

I have seen wildly divergent figures for the projected price decline. The only way to see who is right is to wait and see.

However, the median price of existing homes is down 1.3% from year ago levels and 7.5% from July 2006, when the median price of existing homes probably peaked at $230,200. Prices increased .9% from the previous month in the latest existing home sales numbers. However, prices have steadily declined since July of last year, making the most recent increase just as likely a statistical blip on a decreasing price line.

Two complicating Factors

In a weak market, some homeowners facing a large payment shock would find it difficult, if not impossible, to refinance their loan or sell their home for what they owe on it. About 13% of the owners who face a mortgage rate reset this year have less than 5% equity in their home, and therefore will not be able to refinance unless they have other assets.

If prices fall 5%, the percentage with no equity would grow to 23%, according to Christopher Cagan, director of research for First American CoreLogic, a mortgage research firm in Sacramento. And if prices fall 10%, it would jump to 35%.

This is where the situation could become far more negative. As prices drop, homeowners will have less equity. That means the possibility of refinancing their loans will decrease, increasing the risk of foreclosure.

And then there's the chilling effect of a slowdown on consumer spending. According to Federal Reserve data, consumers have taken about $3 trillion in equity out of their homes in the past five years, adding about 7% to disposable incomes every year. That boost kept the economy humming and has driven the personal savings rate below zero for the first time since the Great Depression.

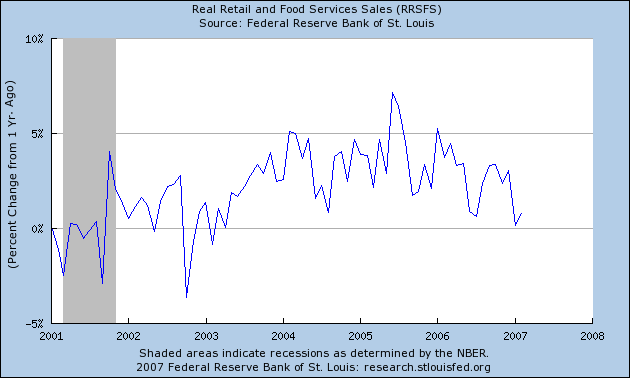

Here's a chart from the St. Loius Federal Reserve of the year-over-year percent change in retail sales adjusted for CPI:

These numbers jump around, so the latest decline may not indicate a move into 0% territory. The US consumer is very resilient, and will find a way to spend in practically any market.

However, it's also important to remember the latest drop in year-over-year coincides with negative housing news of the last 6+ months. These two incidents are correlated, but we may not have causation -- one event causing another. Put this is the "food for thought" category.

Conclusion 1: Inventory will increase and available buyers will decrease. Prices will keep falling, albeit gradually.

Conclusion 2:

In dollar terms, the scale of the potential losses from resets of adjustable-rate mortgages is insignificant when compared with the size of the capital markets. Cagan estimates losses of just $112 billion out of a $9 trillion mortgage market, leading him to conclude that mortgage resets won't break the economy or the financial system.

This is going to be with us for awhile. It's going to take at least a year and probably longer for this whole situation to shake-out.

Here's a bit of related news from Bloomberg:

U.S. homeowners are falling behind on their payments 33 percent faster than they did last year, according to a report by California-based RealtyTrac, which researches data on Americans entering the foreclosure process.

In February, foreclosure proceedings -- from default notices for late payment to auctions and repossessions -- rose 12 percent from a year earlier, affecting 130,786 properties, or one in every 884 U.S. households, RealtyTrac said.

Falling or little-changed home prices are making it difficult for homeowners to sell or get new mortgages on homes they bought or refinanced with adjustable-rate mortgages.