A big thank-you to New Deal Democrat for this diary's title. If memory serves, he used it in a previous comment thread.

The US economy is at an important crossroads. There are three distinct camps of thought. The first is the inflationary crowd, who look at rising commodity prices aided by a declining dollar. The second is the "soft landing" camp which argues the economy’s growth will slow but will not fall into a recession. Finally, there is the recession crowd, which thinks the economy will fall into a recession within the next 12-18 months, largely as the result of the housing market and its related problems. As of this writing, no one camp can claim its argument is superior than the others. Instead, we have a combined mish-mash of economic numbers.

The Inflationary Camp

There are two main arguments the inflationary camp makes. The first is the continuing rise in commodity prices. Here is a daily chart of agricultural prices.

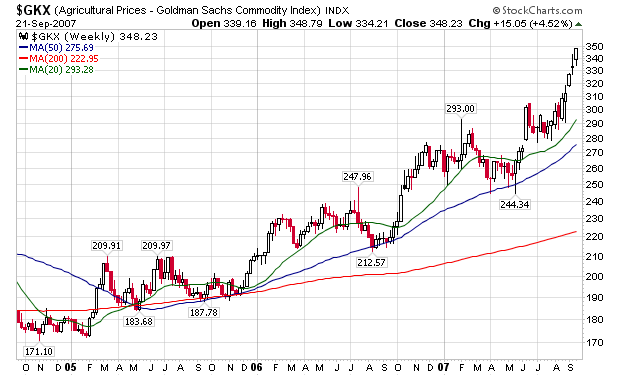

Here is a chart of weekly agricultural prices.

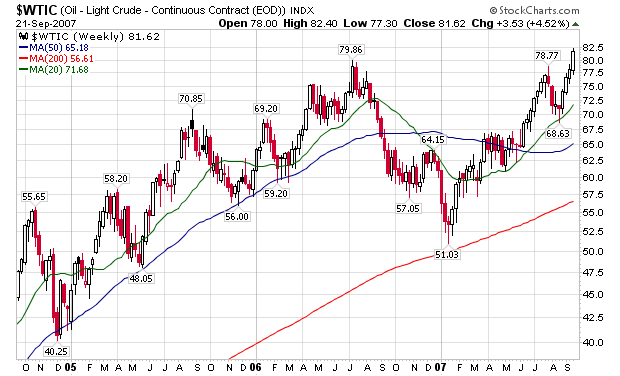

Here’s a weekly chart of oil prices – which are trading at historically high levels.

There is also copper:

And cattle.

And gold:

The point of these charts is to illustrate that basic commodities – the raw materials of products – are increasing in price at high rates.

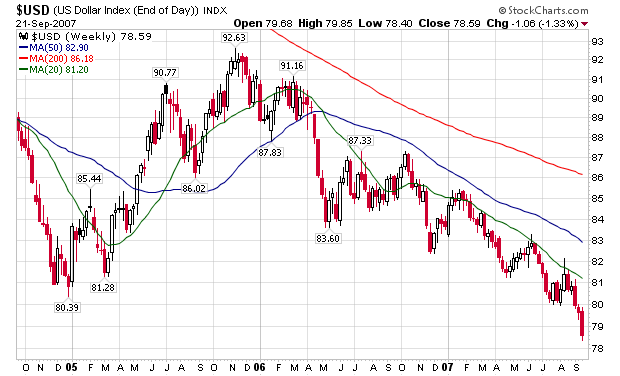

Because most commodities are priced in dollars, the dollar’s value has an impact on commodity prices. The Fed’s rate cut last week occurred when the dollar was trading near all-time low levels. The dollar dropped as the result of the rate cuts with many traders stating the obvious: the Fed is going to sacrifice the dollar’s value. A lower dollar is also by definition inflationary.

The rising inflation camp has strong data points to back-up their arguments.

The Soft-Landing Argument

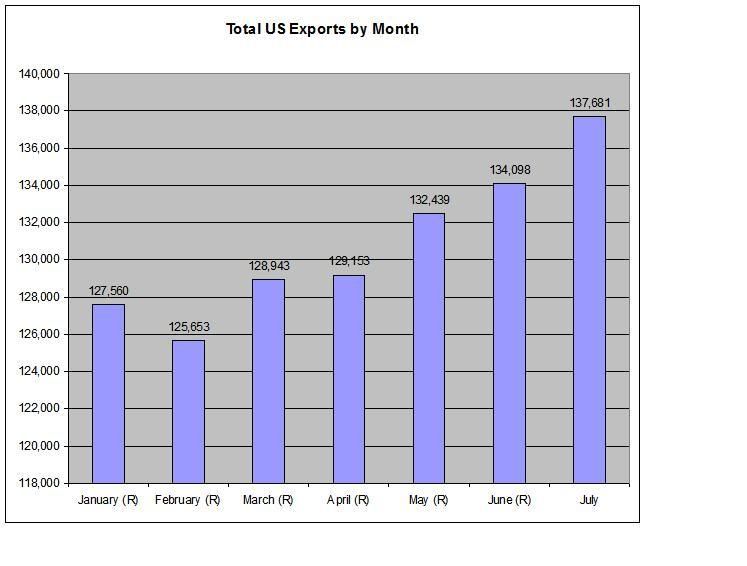

The "soft-landing" crowd has two arguments. The first is rising US exports. Thanks to a cheap US dollar, US exports are now more competitive across the globe. As a result, exports have been increasing at a strong rate for most of this year. Here is a chart of US Exports for this year:

Helping this process along is the overall strength of the global economy. Outside the US everybody is doing fairly well. This means that larger US companies that have a strong international presence should benefit.

The second argument made by the soft landing crowd is the overall resilience of the US economy. The bottom line is the US is an incredibly strong economy and country and it has the ability to withstand a tremendous amount of economy strain. 9/11 should have destroyed the economy for some time. Instead, we slowed down but pick-up again pretty quickly. In short, this is not an ephemeral argument to be dismissed lightly.

The Recession Argument

Housing is central to the recession argument. First, let’s backtrack to explain why housing is in terrible shape. According to the National Association of Realtors, the total inventory of existing homes for sale is 4,592,000 – by far, the largest amount on record. As a result, home prices are dropping:

The annual returns of the U.S. National Home Price Index, the 10-City Composite, and the 20-City Composite shows all three still yielding negative returns as of June 2007. The quarterly S&P/Case-Shiller(R) U.S. National Home Price Index -- which covers all nine U.S. census divisions -- was down 0.9% from Q1 2007 and down 3.2% from Q2 2006.

At the same time, there is a credit contraction in the secondary mortgage market. Lenders are tightening their lending standards, making it more difficult to obtain a loan. The bottom line is despite the numerous calls for a bottom in the housing market, it doesn’t look at thought the market is anywhere near a bottom.

On top of that, the recent employment report indicted the economy lost 4000 jobs in August. In addition, the latest employment report revised June and July’s payroll gains lower. This is only on month’s data, so it is always possible the trend could reverse.

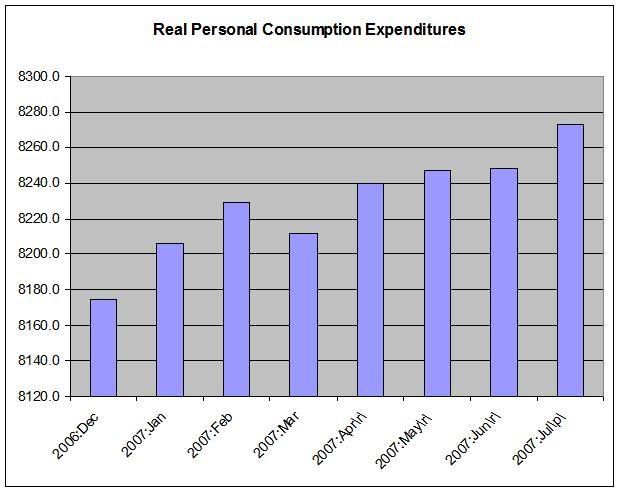

Personal consumption expenditures increased in the latest report, but that was after they somewhat stalled over the Spring. Here is a chart of personal consumption expenditures in 2000 chained dollars, seasonally adjusted to their annual rate.

While these aren’t terrible numbers, they aren’t that great either. The US consumer could be doing a whole lot better.

So – where does that leave us?

Not in a good place. None of the above mentioned scenarios are good. The best the US economy can hope for right now is a soft landing. It is possible the Fed rate cuts came at the right time and the economy will move into a period of lower growth. However, the inflationary and recession camps also have strong arguments. The bottom line is we don’t know. But at the very best right now we can expect a period of sub-par growth.