As this week-end claims its second major bank CEO (Chuck Prince leaving Citigroup just a few days after Stan O'Neal was forced to leave Merrill Lynch), the financial world is bracing itself for more bad news.

As bad news have kept on coming relentlessly from investment banks, with new write downs from Merrill Lynch ($7.9 bn), UBS (SFR 4 bn), monoline insurer FSA ($200m) and, of course, Citigroup ($3.3 bn), more is expected in the very near future.

As I wrote on Friday morning, banks are trying their damnedest to hide what's going on, but the few available market-based indicators are all pointing to a bloodbath. and it keeps on getting worse.

Shares of Merrill Lynch were hammered on Friday on concerns that more writedowns are yet to come (up to $10 bn). Same with Citi (just another $4 bn).

This Financial Times article (accessible with a free reg.) does a good job of pointing a few worrying things:

Perhaps the most shocking thing about recent announcements is that while big banks might have now written down their mortgage holdings by more than $20bn, this does not appear to capture all the potential losses.

Last week, for example, a US congressional committee warned that over the next year mortgage lenders could foreclose on 2m American homes, destroying $100bn of housing value. And some private sector economists think the total loss from mortgage problems could reach $200bn or more. “What everyone keeps asking is where are those losses sitting – where is the rest of that $100bn?”

And, on top of that, the problem is that a whole pyramid of financial instruments has been built on top of these mortgages:

For in recent years, banks have not simply been acquiring subprime loans, they have been repackaging them into complex “asset-backed securities” (ABS) that can be difficult to value. The Bank of England, for example, suggests that on the basis of industry data some $700bn-worth of bonds backed by subprime loans are now in circulation in the world’s financial system, with another $600bn of bonds backed by so-called “Alt A” loans, or those with slightly better credit quality.

Moreover, these bonds have then been used to create even more complex securities backed by diversified pools of debt, known as collateralised debt obligations (CDOs). According to the Bank’s calculations, for example, some $390bn of CDOs containing a proportion of mortgage debt were issued last year – though the precise level of the subprime component varies.

There's more in the article, but one thing strikes me today: the "structured finance" world is reeling today despite the fact that the economy is supposedly going well - ie it is not able to cope with what are meant to be mild economic conditions. what will happen when the coming recession strikes? Of course, to some extent, today's market crunch reflects the fears associated with that recession, but as most pundits and market players still tend to dismiss the possibility of anything worse than a mild recession (don't ask me why), it is unlikely that the full impact of any serious downturn is priced in already.

In fact, I invite you to take a look at this article from Fortune two weeks ago which explains in detail how some of thes structured products worked, and how they are faring today...

In the spring of 2006, Goldman assembled 8,274 second-mortgage loans originated by Fremont Investment & Loan, Long Beach Mortgage Co., and assorted other players. More than a third of the loans were in California, then a hot market. It was a run-of-the-mill deal, one of the 916 residential mortgage-backed issues totaling $592 billion that were sold last year.

The average equity that the second-mortgage borrowers had in their homes was 0.71%. (No, that's not a misprint - the average loan-to-value of the issue's borrowers was 99.29%.)

It gets even hinkier. Some 58% of the loans were no-documentation or low-documentation. This means that although 98% of the borrowers said they were occupying the homes they were borrowing on - "owner-occupied" loans are considered less risky than loans to speculators - no one knows if that was true. And no one knows whether borrowers' incomes or assets bore any serious relationship to what they told the mortgage lenders.

Those that do not want to admit that the real estate world had gone completely insane need to read these two paragraphs again: not only people were able to borrow (huge) amounts of money that they would be able to pay back only if housing prices went up, but this was considered normal and a sound basis to create mortgage-backed paper. The lenders were confident that the loans could be passed on to the investment banks, which were confident that they could use them as core ingredients for new paper that would get a decent ratings and be sold to investors, rating agencies were willing to give their stamp of approval, and investors were indeed willing to buy.

A "run-of-the-mill" deal. One of a thousand. Sold to pension funds or mutual funds or other investors looking for good, safe, returns.

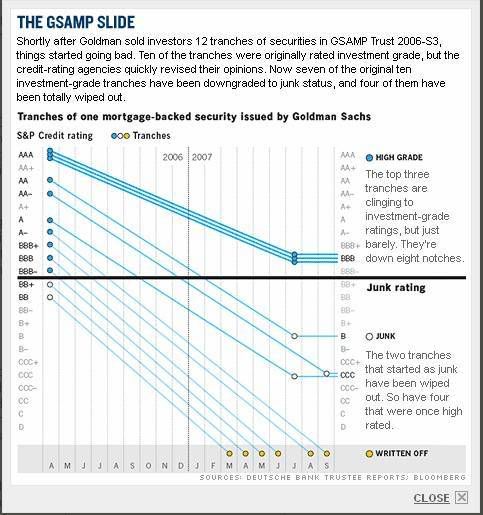

In this case, Goldman sliced the $494 million of second mortgages into 13 separate tranches. The $336 million of top tranches - named cleverly A-1, A-2, and A-3 - carried the lowest interest rates and the least risk. The $123 million of intermediate tranches - M (for mezzanine) 1 through 7 - are next in line to get paid and carry progressively higher interest rates.

Finally, Goldman sold two non-investment-grade tranches [and kept one more, the riskiest, as its fee for the deal}

(...)

Even though the individual loans in GSAMP looked like financial toxic waste, 68% of the issue, or $336 million, was rated AAA by both agencies - as secure as U.S. Treasury bonds. Another $123 million, 25% of the issue, was rated investment grade, at levels from AA to BBB--.

Thus, a total of 93% was rated investment grade. That's despite the fact that this issue is backed by second mortgages of dubious quality on homes in which the borrowers (most of whose income and financial assertions weren't vetted by anyone) had less than 1% equity and on which GSAMP couldn't effectively foreclose.

This is a very, very important point. Having your paper rated "investment grade" is extremely valuable for investment banks because it can then be sold to regulated entities that are allowed to buy only such paper. That rule is in place to ensure that such funds invest only in safe securities. That rule, which is imposed by the US government (and enforced by the SEC), applies to funds like pension funds and the like, and makes a lot of sense. It gives rating agencies an amazing power - that to decide what investments are legally safe.

And they get paid by the investment banks cooking up the paper to do that job (and they get paid by them to advise them on how to obtain the ratings, too).

How is a buyer of securities like these supposed to know how safe they are? There are two options. The first is to do what we did: Read the 315-page prospectus, related documents, and other public records with a jaundiced eye and try to see how things can go wrong.

The second is to rely on the underwriter and the credit-rating agencies - Moody's and Standard & Poor's. That, of course, is what nearly everyone does.

It is also hard to underestimate how much people rely on such ratings. The paper has a good rating, you don't need to do any analysis yourself, you can buy it safely.

Moody's projected in a public analysis of the issue that less than 10% of the loans would ultimately default. S&P, which gave the securities the same ratings that Moody's did, almost certainly reached a similar conclusion but hasn't filed a public analysis and wouldn't share its numbers with us. As long as housing prices kept rising, it all looked copacetic.

Goldman peddled the securities in late April 2006. In a matter of months the mathematical models used to assemble and market this issue - and the models that Moody's and S&P used to rate it - proved to be horribly flawed. That's because the models were based on recent performances of junk-mortgage borrowers, who hadn't defaulted much until last year thanks to the housing bubble.

The fallout

Through the end of 2005, if you couldn't make your mortgage payments, you could generally get out from under by selling the house at a profit or refinancing it. But in 2006 we hit an inflection point. House prices began stagnating or falling in many markets. Instead of HPA - industry shorthand for house-price appreciation - we had HPD: house-price depreciation.

Interest rates on mortgages stopped falling. Way too late, as usual, regulators and lenders began imposing higher credit standards. If you had borrowed 99%-plus of the purchase price (as the average GSAMP borrower did) and couldn't make your payments, couldn't refinance, and couldn't sell at a profit, it was over. Lights out.

And this is how it looks:

Written off means that all the money is lost and unlikely to be ever recovered. From the numbers above, it looks like 25% of the securities have lost all their value, and another 7% are hanging in by a thread.

and that's before the housing markets have even tanked. They've just, so far, tightened, but that's enough to destroy the economics of the underlying deals (those that required increasing prices to make any sense). Now, as prices start actually going down, and more of the funny mortgages kick in (those that had sweetened interest rates for the first 2-3 years, and which now see their monthly payments skyrocket), more defaults are likely.

Potential losses will turn to real ones. Securities will be written off. Banks will take more hits. They will tighten their credit . As Migeru noted in the previous thread, banks are now saying "my balance sheets were full of worthless assets; if my balance sheet is this ugly, imagine the neighbour's" and have stopped lending to one another - thus the credit crunch, which means that they are also restricting loans to corporations (as they can no longer easily refinance themselves behind) and hoarding cash.

Which means that the whole financial model of companies, funds and financial institutions financing their activities on the markets is compromised. When your business model was based on paying 0.20% as financing costs (and lending, for instance, at 0.50-1.00%) and you have to pay 2.50% now to borrow, you're in big , big trouble.

And, again, this is happening with the econmy still officially doing fine. We on the blogs know that the economy has not been doing fine for quite a while, with a lot of wealth capture rather than wealth creation happening, and a lot of concentration of wealth in a few hands. Well, the wealth was imaginary, but the capture has been all too real.

The question, again, is - who will pay when "imaginary" turns into "non-existing"? If the Democratic candidates don't talk about this, whoever is elected WILL be blamed for it come 2009. This is a slow motion crash; it is by no means clear that the crash will be obvious by November 2008, and it is certain that the only goal of Bush, Bernanke et al is to delay the reckoning until after the election. If the problem is not identified and flagged right now, it will be blamed on the new occupant of the White House.

Time to speak up.