This past week brought fresh news that American consumers, for so long seemingly invulnerable, are finally caving in. A surge in inflation that is directly correlated with the Federal Reserve's lowering of interest rates by 3/4% since mid August has caused a critical mass of consumers to slow down. This adds to the evidence that beginning last month the US entered a recession.

In recent diaries I have explained how recessions typically start with a housing slowdown, then a slowdown in big consumer goods like cars, and then spread out into general retail weakness and finally increases in layoffs and unemployment. I have also shown how this year, for only the second time in the last 25 years, the American consumer has run out of sources (wage increases, home equity loans, stock market gains) of cash or credit for spending. I said that only a decline in retail sales and an increase in jobless claims remained.

In October, retail sales started to capitulate.

I. Retail Sales and Recessions

This past summer, Prof. Edward Leamer presented a paper to the Fed (warning: pdf) examining all 8 recessions since the end of World War 2, and concluded that almost all of them followed a predictable scenario:

After residential investment as a contributor to prior weakness come consumer durables, consumer services, and then consumer nondurables. Those are all consumer spending items -- it's weakness in consumer spending that is a symptom of an oncoming recession.... The timing is: homes, durables, nondurables, and services. Housing is the biggest problem in the year before a recession

There is no need to discuss further here the collapse of the housing market. Auto sales (the biggest consumer durable) have been in decline for over half a year.

According to Shoppertrak, however, until October of this year, retail sales had been holding up reasonably well. Here's a monthly chart showing gross sales increases from the same period in 2006, minus the inflation rate, for the net inflation-adjusted actual growth in retail sales:

January: +4.9% gross sales minus (2.1%) annual inflation = +2.8% net

February: +4.3% (-2.4%) = +1.9%

March: +2.7% (-2.8%) = -0.1%

April +2.3% (-2.6%) = -0.3%

May +4.0% (-2.7%) = +1.3%

June, +4.7% (-2.7%) = + 2.0%

July + 4.0% (-2.4%) = +1.6%

August +4.1% (-2.0%) = +2.1%

September +3.4% (-2.8%) = +0.6%

October + 2.8% (-3.5%)(est.) = -0.7%

The sudden downdraft was also reported on Thursday by the International Council of Shopping Centers, which reported:

U.S. chain store sales grew 1.6 percent in October compared to the same month last year, according to ICSC’s index. This performance held steady with September’s results, which showed a 1.7 percent increase. .... “"Over the last two months, retailers have struggled with the warm weather's negative impact on retail spending," said Michael P. Niemira, ICSC's chief economist and director of research. “However, for the November-December period, we are expecting a marked improvement from the very sluggish September-October performance.” Niemira said he expects November comp-store sales to increase by about 2.5 percent.

Even though October sales nominally "grew" by 1.6%, once the likely annual inflation rate is subtracted, this becomes a real contraction of -1.9%, and the expected November reading is also a real, inflation adjusted contracton also.

In fact, Shoppertrak reported early November sales have also declined in real terms:

ShopperTrak RCT Corporation's National Retail Sales Estimate™ (NRSE) today reported that retail sales for the week ending November 3 increased 1.7 percent as compared to the same period in 2006

II. Why are retail sales slowing now?

We've known for some time that the working class consumer has been suffering (recall how Wal-mart reported that sales were dropping off in the few days before mid and end of the month paychecks are issued). What is different now is that it is the "affordable luxury" part of the retail spectrum that is capitulating:

Wall Street analysts say that could hurt specialty retailers like Coach Inc. (COH) , which touts affordable luxury, as well as upscale emporiums like Nordstrom Inc. (JWN) and Saks Inc. (SKS) , which have increasingly tapped into the "aspirational" market of consumers who a cut below the superwealthy.

Citing slowing customer traffic, Coach expects holiday sales at North American stores open at least a year to rise at their slowest pace in at least six years. Nordstrom, which had been one of the sector's leading performers, recently lowered its third-quarter profit forecast.... Rival Saks also reported lower-than-expected September same-store sales.

Earlier this week, Liz Dunn, analyst at Thomas Weisel Partners, ... [said] that consumers may be "cracking under pressure" as home values decline.

"We are beginning to witness an unwinding of the wealth effect," Dunn wrote in a report for clients. "Consumer spending has been boosted by consumers' impression about their 'paper wealth' tied to the value of their homes. Now that home values are falling, spending is slowing."

...."weakness is spreading pretty far up the food chain."

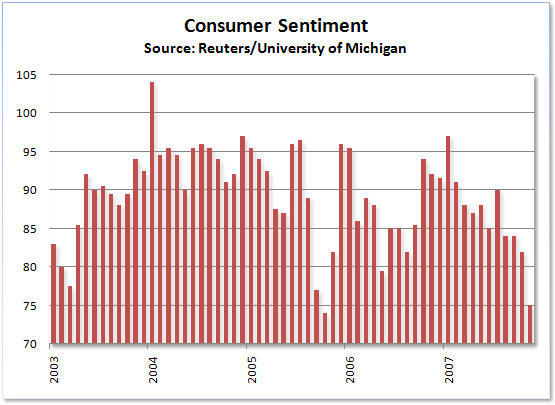

This loss of confidence by US consumers is pretty obvious in this chart of "consumer confidence" which fell to a low only seen one time since the last recession:

III. It's the inflation, stupid.

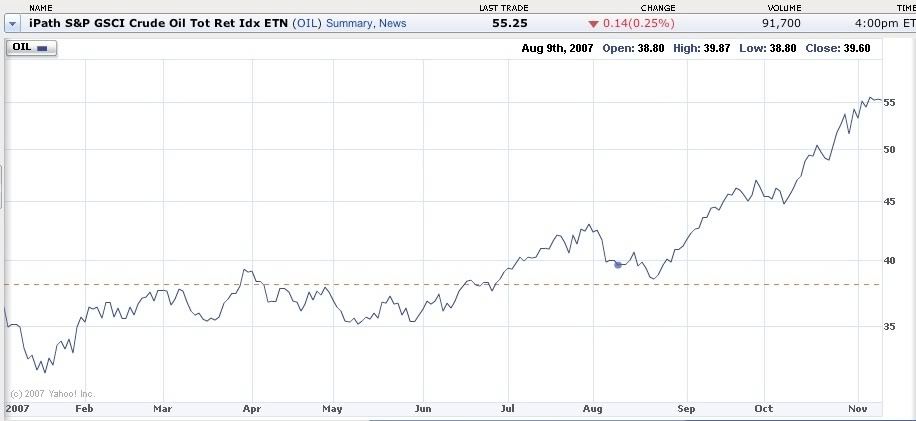

The reason for the sudden loss of confidence by even affluent and upper middle class consumers is also pretty obvious: sharp increases in energy and food prices, especially (and not just coincidentally) in the last 3 months since the Federal Reserve caved in to Wall Street and decided to bail out investment bankers and financiers with two rate cuts so far. Here's a graph of oil prices. They've gone up almost 50% since mid-August!

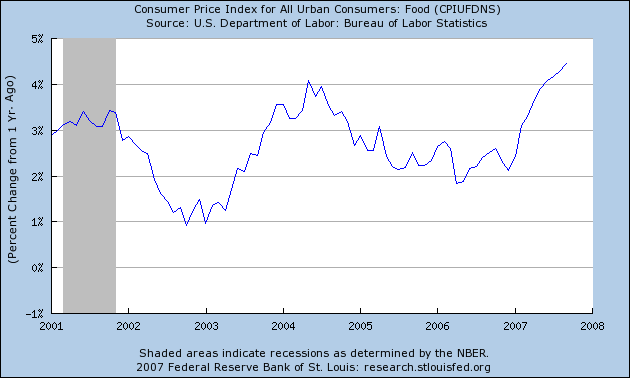

And here's a chart of food prices, which are also surging up to 6% on average:

And, there's no sign of a let-up on the inflation front. Here's a graph of import price inflation for the last 10 years. Look at that spike just reported for October 2007. It certainly foretells a rude shock in the producer and consumer price inflation readings that will be reported this coming week:

So, where do consumers turn to fuel their spending? Their houses continue to decline in value. Their stock portfolios aren't doing so well at the moment either: as of Friday, the S & P 500 stock index is only up about 2.5% this year. They're not getting big wage increases.

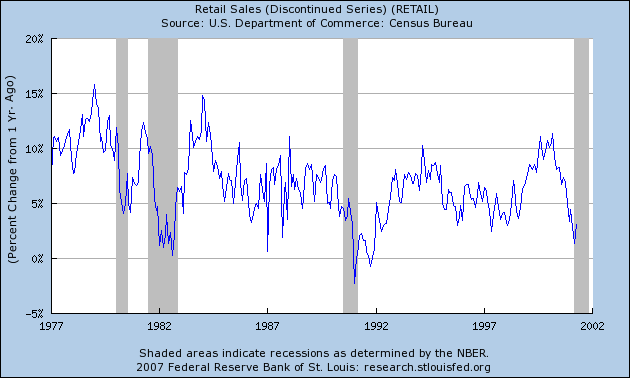

Signs are, consumers are finally pulling in their horns. What happens then? Here's a picture:

P.S. I'm going to post The Definitive Daily Kos guide to Inflation in the next day or two, and I'll have more to say about inflation later this week when the PPI and CPI are reported.