I don't like "The Sky is Falling" diaries. People tend to muddle through. Put enough people together and you get an economy, and the economy tends to muddle through, too.

But every now and then it is prudent to be fearful. Not panic-stricken, but instilled with enough caution to focus on a serious problem, to check and double-check if one's house is truly in order.

Now appears to be such a time. In the last 24 hours, a state pension fund closed its doors to new withdrawals after a "run" on the fund by municipal participants. I believe this is only a foretaste of what is to come over the next 12-48 months.

There is an excellent chance that the dominant issue of the 2008 election campaigns will not be Iraq nor iran nor executive power nor immigation, It will be the economy, in the form of this "Panic."

The story, and the ramifications, below.

Yesterday bloomberg reported:

Florida officials voted to suspend withdrawals from an investment fund for schools and local governments after redemptions sparked by downgrades of debt held in the portfolio reduced assets by 44 percent.

Today's Orlando Sentinal fleshes out the detail:

The unanimous vote by the State Board of Administration -- Gov. Charlie Crist, Attorney General Bill McCollum and Chief Financial Officer Alex Sink -- halted at least temporarily a run on the fund that has seen withdrawals totaling $16.5 billion in the past several weeks. That's nearly two-thirds of the assets the fund reported Nov. 1.

The freeze will last at least until Tuesday, prompting concern from some local governments that they might have trouble making payroll without access to their money. That's because they invest their operating money in the state fund as a short-term investment.

"They've got bills. There's payroll in the next couple of days. You've got bond proceeds that have to pay debt service," SBA executive director Coleman Stipanovich warned the board. "If you just arbitrarily cut off liquidity, I have no idea what the ramifications will be."

The surprise vote came at the close of a tense emergency meeting ....

"If we don't do something quickly, we're not going to have an investment pool," Stipanovich said.

....

"We have a higher duty not to just help local governments make a mound of dough," Crist said, "but to make sure those who invested in the pension -- the people -- are protected."

And the Florida pension fund isn't the only pension fund with potential exposure:

Thousands of school, fire, water and other local districts across the U.S. keep their cash in state- and county-run pools. These public accounts, modeled after private money market funds, are supposed to invest in safe, liquid, short-term debt such as U.S. Treasuries and certificates of deposit.

All told, there were about 100 such pools...

Public fund managers say they've bought SIV debt because it had the safest credit ratings and offered higher yields than other short-term fixed-income investments.

....

Among the places caught up in the SIV and subprime snarls are Connecticut, Florida, Maine, Montana and King County, Washington. Public funds hold $1 billion of defaulted asset- backed commercial paper, including $273.5 million from SIVs.

Montana entrusted $465 million, or 19 percent of its $2.5 billion investment pool, to SIVs.

But here, from the same article, is the kicker:

Nobody knows how much more pain is coming. State funds could lose hundreds of millions of dollars, says Lynn Turner, chief accountant of the U.S. Securities and Exchange Commission from 1998 to 2001.

In august of this year, there was a similar "run" on 2 Bear Stearns hedge funds, but there was no direct municipal or employee retirement exposure. This was a bad, leveraged bet by some of Wall Street's Big Boyz and Gurlz.

At the same time, there was an isolated "run" on a single L.A. branch of a bank subsidiary of Countrywide Financial, the biggest subprime lender.

This time is different. This is a direct run on a pension fund pool by participants who have a finduciary duty to their individual clients, who are ordinary school district and other municipal workers.

Is this going to be an isolated incident, with no significant consequences? That's certainly possible. But the likelihood that there will be a steady trickle or stream of such runs, or even the possibility that this could presage a cascade of such runs, climaxing in a general "run" on uninsured or not-sufficiently insured (think the municipal bond insurers MBIA and Ambac) financial institutions can no longer be dismissed out of hand.

UPDATE: Panicking as we speak!

Only 4 hours after I posted this diary, it is reported that Montana's municipal depositors are pulling thir money out of that state's fund, totalling about 10% so far:

The Montana Board of Investments, which manages the state's money, has seen $247 million withdrawn by local governments in the past three days from a $2.5 billion money-market-like fund called the Short Term Investment Pool.

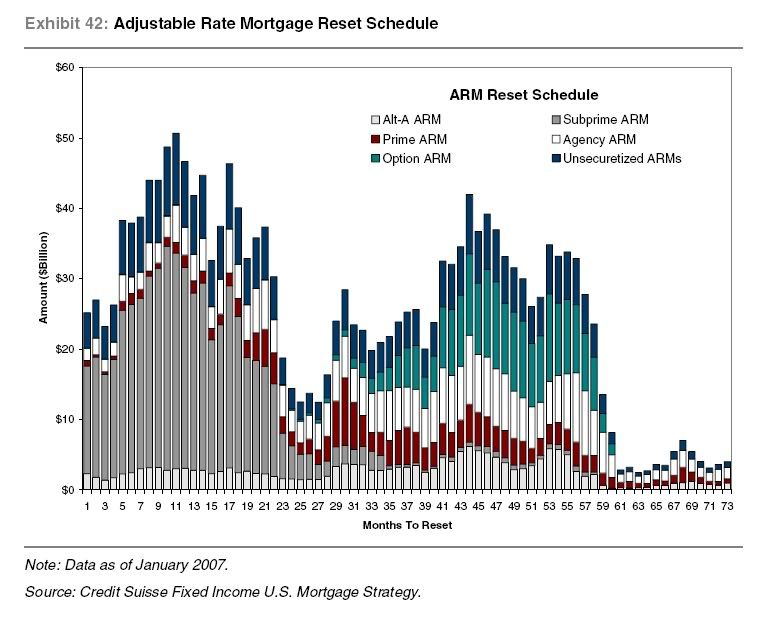

Keep in mind that we are only 1/4 of the way through the toxic mortgage resets that are the root problem whose consequences have spread throughout the entire economy -- in large part because so many entities were invested indirectly in them. Here's that familiar graph again:

And now, as opposed to 1998 or 2001, it seems that every financial company is an Enron, every player has been using leverage like Long Term Capital Management.

The last time our country went through a multi-year combined housing/credit bust, built on financial speculation and leverage, was the decade that began in 1926. Here's the second crucial graph, beginning in 1920, that shows the housing bust that presaged all the other pain to come:

Let me close with some anti-sky-is-falling disclaimers: This is NOT the Great Depression II. Nor is this the stagflationary 1970s. It is going to unfold as some other Beast. Only the broad outlines of this Beast appear discernable now: it will likely feature (1) increasing import prices; (2) wage stagnation (that does not keep up with price inflation; (3) real asset deflation; and (4) possibly a Japan-style "liquidity trap." In fact, while I believe we are already in a recession, I suspect there will be a business upturn late next year.

Furthermore, I believe there will be NOT any "runs" on FDIC-insured bank deposits. Period. In fact, I suspect they will turn out to be the best havens in the storm. But this slow motion bust, this Panic of 2008 (and thereafter), will be painful, and it will unfold. I do not think it can be avoided any more.

In closing, as the "containment" spreads from one supposedly "watertight" financial compartment to another, let me give you one easy pictorial representation: YOU ARE HERE: