In What Might Real Financial Reform Look Like?, The Agonist editor and former Morgan Stanley banker Sean-Paul Kelley has outlined ten critical financial reforms that, amazingly, neither Obama nor McCain -- nor anyone in the mainstream media for that matter -- are even discussing.

I’m tempted to just copy and paste the entire article, but of course I can’t do that. So, I’ll urge you to follow the link. But here’s the ten-point reform plan, in brief:

Please follow below the jump.

- "Mark-to-model should be excised from GAAP and disallowed. End of story. If you can't discover a real price, then there isn't a market for it."

- "disclosure and absolute transparency when it comes to any kind of credit derivatives. . . [and] There must be limits on the amount of contracts one can write on any specific security, just as there are limits for options trades and futures trades."

- "make it mandatory for all bankers, hedge funds, all bank employees and executives and pretty much anyone who works in a 'securitized' or derivative market to get licenses to work in the securities market. . ."

- "executive compensation and clawback provisions. It is simply obscene that Lehman Brother's filed for bankruptcy but in those proceedings their executives were allotted $2.5 billion in bonuses. Are you fucking kidding me? (You didn't know this had happened did you? Well, it is true.)"

- "enforce anti-trust laws. If it is too big to fail, it is too big to exist. . . . Break up Wal-Mart, the media conglomerates, the mega-banks, the mega-retailers, Microsoft and quite possibly Google."

- "regulate hedge funds, although keeping said regulation at a minimum."

Here I disagree. Hedge funds should be outlawed, plain and simple. They serve mostly to hide movement of hot money, At the very least, they should be forced into full disclosure. We’ve already been burned twice by hedge fund opacity – once with Long Term Capital Management, and now the present crises, which began last summer when two Bear Stearns hedge funds exploded.

- "overhaul municipal bond issuance, marketing, selling, and trading regulations." Kelly notes here that municipal bond issuance is actually completely unregulated at this time. Mind-boggling.

- Kelly writes that there is no need for reform of the innsurance industry reform, except for the credit default swaps, which are what brought down AIG. He notes that "It's a good things the states have authority over this [insurance] or AIG really could have been a cataclysm of an altogether horrific order."

- "enact a Tobin tax on all cross-border financial trades."

Here again, I think Kelly does not go far enough. I would make it the highest priority to impose a Tobin / Pigou tax, on ALL financial transactions, not just cross-border. And it must be determined exactly at what percentage the tax works to discourage short-term trading, without damaging long term holding, especially of equities and debt that is going directly into the creation of new, physical capacity.

In fact, I think a transactions tax is probably the one most important step we can take at this time – and the fact that it is not even being discussed is a reflection of the utter bankruptcy of the U.S. political and media elites. So, here are a few links to follow on this crucial issue:

Destabilizing Speculation and the Case for the Tobin tax

http://www.currencytax.org/

http://www.globalpolicy.org/...

http://www.ceedweb.org/...

- "Finally, everyone in the investment business, instead of having to take obligatory exams on new bullshit Patriot Act money laundering laws--which actually made it harder for new business to start up, not to mention the fact that anyone with half-a-brain and a sound understanding of fiduciary responsibility knows who's laundering and who's not--should take mandatory classes on financial prudence, what systemic risk is, what causes it, etc."

Here again, I must interject. Not that Kelly is wrong, but he provides an important clue to how we can proceed to remove many of the people who created this disaster. If $5,000 can be tracked back from a call girl to take down the sitting governor of New York, then it should not be that difficult to track down the hundreds of billions of dollars of hot money sloshing from the Cayman Islands, to Lichtenstein, to Switzerland, the City of London, and so on. That money should be seized, and all participants in the financial laundering imprisoned, with special attention to removing the very top people – the CEOs, CFOs, directors, and other top managers and officers of the banks and hedge funds involved.

Stop and think about it: What other way is there to remove from the scene the people who have created these financial derivative markets and who are pretty much still running the show? This may sound harsh and unreasonable now, largely because it is impolitic, but as the coming depression worsens, the public mood is going to become very ugly indeed, and the demand for villains to blame is going to be overwhelming. If we don’t bring forward the correct villains, chances are we will fumble the policy response to these crises, and squander a historic attempt to transform capitalism into something much better, and far more useful, than it now is.

Those are Kelly’s ten points, but there are a few more measures that I believe are required which he does not mention.

One is ending the regime of free floating exchange rates. This is a particularly important issue for what we call "Third World" countries. In March 2006, Thomas Palley quite accurately forecast the bursting of the U.S. housing bubbl, and located it as just one part of a larger and increasingly dangerous imbalances in the world financial system. In that paper, which is entitled "The Fallacy of the Revised Bretton Woods Hypothesis: Why Today’s System is Unsustainable and Suggestions for a Replacement," Palley proposed a scheme of crawling band target zones to replace the complete, unregulated chaos we have today in foreign exchange markets.

Such a system involves choice of a number of parameters that would need to be negotiated by participants. First, there is choice of the target exchange rate. Second, there is the choice of size of the band in which the exchange rate could fluctuate. Third, there is a choice whether the band would be hard or soft. A hard band is automatically and decisively defended; a soft band is one that allows for marginal temporary deviations outside the band, while retaining a commitment to bring the exchange rate back within the band when market conditions are most conducive. Fourth, there is the choice of the rate of crawl. This involves determining the rules governing the adjustment of the target and band. Issues here concern the periodicity of adjustment, and the rule governing adjustment of the nominal exchange rate. . . .

Finally, rules of intervention to protect the target exchange rate need to be agreed upon. Historically, the onus of defending the exchange rate has fallen on the country whose exchange rate is weakening. This requires the country to sell foreign exchange reserves to protect the exchange rate. Such a system is fundamentally flawed because countries have limited reserves, and the market knows it. This gives speculators an incentive to try and "break the bank" by shorting the weak currency, and they have a good shot at success given the scale of low cost leverage that financial markets can muster. Recognizing this, the onus of exchange rate intervention needs to be reversed so that the strong currency country (the central bank whose exchange rate is appreciating) is responsible for preventing appreciation, rather than the weak currency country being responsible for preventing depreciation. Since the strong currency bank has unlimited amounts of its own currency for sale, it can never be beaten by the market. Consequently, once this rule of intervention is credibly adopted, speculators will back off, making the target exchange rate viable. Such a procedure recognizes and addresses the fundamental asymmetry between defending weak and strong currencies.

I think it is also worth repeating here a somewhat lengthy passage from Robert A. Blecker’s Taming Global Finance: A better architecture for growth and equity, even though some of the points Blecker makes have been made above.

But no amount of transparency and supervision can eliminate the inherent information problems in international capital markets or prevent global financial flows from destabilizing domestic economies. In order to make international capital flows serve the broader public interest in a more stable, equitable, and prosperous global economy, further policy reforms are needed in four interrelated areas:

1. Regulating capital movements. A variety of measures such as capital controls, exchange controls, and transactions taxes (including a "Tobin tax" on foreign exchange transactions) can help to discourage short-term speculative capital flows, restore greater national policy autonomy, and encourage more stable, long-term investment. . . .

2. Reforming international institutions. The international financial system has become integrated to a point where the need for global regulation cannot be avoided. Simply abolishing the IMF and allowing markets to discipline errant countries would be a mistake because it would invite greater instability and harsher adjustments. While in the future it may be desirable to create new global institutions, such as a world central bank or international supervisory agency, most such proposals are politically unrealistic at present-although regional institutions such as an Asian Monetary Fund are more feasible in the short term. Today, the most immediate priority is to fundamentally reorient the governance and policies of the IMF by replacing its top leadership; instituting more democratic control and accountability; broadening its mission to emphasize global prosperity and distributional equity; tailoring its crisis intervention policies to better meet the needs of specific debtor countries; and shifting more of the adjustment burden in crisis situations onto creditors.

3. Managing exchange rates. Neither extreme of perfectly flexible or rigidly fixed exchange rates is generally desirable. The best way to reduce exchange rate volatility is to establish a compromise system of "target zones" among the major currencies (especially the dollar, euro, and yen), with wide enough "crawling bands" around the targets to allow moderate exchange rate fluctuations - and with regular, small adjustments in the targets and bands to keep them credible. . . .

4. Coordinating macroeconomic policy. Supporting the exchange rate targets and promoting more rapid global growth with more balanced trade and full employment will require economic coordination among the G-7 countries. International coordination of monetary policy would permit reductions in interest rates without creating incentives for speculative capital flight. Countries that agree to coordinate their interest rates need to retain other policy levers for domestic adjustment, however, especially by using fiscal policy more flexibly for countercyclical purposes and by using prudential restrictions (e.g., reserve requirements) more actively for monetary control.

More generally, Palley and Blecker are part of what I hope, with the present financial crises, is a newly reinvigorated movement of heterodox economists who have been consistently attacking the "neo-liberal" economic orthodoxy that has reigned supreme for over three decades now. Which brings me to the a consideration of the cultural aspect of the crises we face. Simply put, real economics has not been taught in the U.S. and most of the West for nearly half a century now. Economics is really quite simple – it is how a society organizes itself to procure, produce, and distribute the material, social, and cultural goods and services required for sustaining and reproducing human life. What almost all our MBAs know instead is monetary theory, a very small subset of economics, which unfortunately came to be mistaken as the be-all and end-all of economics, thanks to Milton Friedman and his "Chicago School." Something quite different used to be taught, for example, the following, from the first two paragraphs from a 1921 book entitled, Economics for Executives, Vol. II, The Primary Industries (A Series of Twenty–Four Reading Texts Which Constitute an Interpretation of the Underlying Principles of Economics and Business for Men and Women in Practical Life), edited by George E. Roberts, American Chamber Of Economics Incorporated, New York, NY., The Benjamin Franklin Institute:

It is logical to begin a study of the fundamentals of economics with a consideration of how mankind satisfies its wants. The activities of society in providing for its desires are termed "production." Our discussion of the principles of economics, therefore, begins with a survey of the sources of production.

Fundamentally, all of the products upon which society is dependent come from the earth. Food, fuel, and raw materials spring either directly or indirectly from this source. The industries, therefore, which extract our food, fuel, and raw materials from the soil or the deposits of nature, may appropriately be termed the "primary industries." Agriculture, mining, lumbering, and fishing are the most important of these industries.

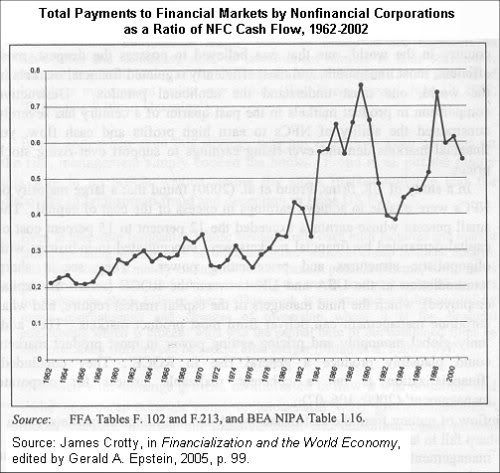

The most pernicious result of this multi-generational mis-education in economics has been the rise of what James Crotty has identified as a "portfolio view" of industrial assets. In The Neoliberal Paradox: The Impact of Destructive Product Market Competition and Impatient Finance on Nonfinancial Corporations in the Neoliberal Era Crotty explains

I stress two aspects of the changing relation between financial markets and large NFCs. The first is a shift in the beliefs of financial agents, from an implicit acceptance of the Chandlerian view of the large NFC as an integrated combination of illiquid real assets – that is, physical and organizational assets that cannot be sold for cash quickly and without a major loss in value – assembled to pursue long-term growth and innovation, to a "financial" conception in which the NFC is seen as a ‘portfolio’ of liquid subunits that home-office management must continually restructure to maximize the stock price at every point in time. The second is a fundamental change in management’s reward structure, from one that linked pay to the long-term success of the firm, to one that links it to short-term stock price movements.

The 1960s conglomerate merger movement initiated a change in the perception of the proper role of top management, from one in which managers were expected to be experts in the main business of the firm, to an evolving view of top executives as generalists who knew how to buy and sell subsidiaries as business conditions changed. This shift remained incomplete, however, until the hostile takeover movement of the 1980s, which forced NFC insiders to either divest units whose stock price fell below the level demanded by Wall Street or yield control of the firm to corporate raiders. Raiders relied primarily on debt to finance takeovers, while managers of targeted firms often defended their turf by loading the firm with debt-financed stock buybacks and special cash dividends to deter potential raiders. These developments pushed NFC debt burdens to historic highs. They also forced a change in managerial goals, from concern with the long-term success of the firm to a short-term obsession with keeping the stock price high enough to deter a hostile takeover.

This is why we have legions of professional MBAs who have run American industry into the ground - they have been indoctrinated to believe that there is no essential managerial difference between running a company that produces semi-conductor lithography equipment, and a chain of brothels in Nevada. I think a quote from John Maynard Keynes is very appropriate here:

"The ideas of economists and political philosophers, both when they are right and when they are wrong, are more powerful than is commonly understood. Indeed the world is ruled by little else. Practical men, who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist." The shift to impatient finance Crotty identifies has fostered malignant cultural and spiritual crises - instant gratification - that is simply beyond the ability of neo-classical economics based on mathematical modeling to either recognize or deal with. This is why U.S. elites, whether they be Democrats or Republicans, seem to act as a monolithic block in supporting and implementing economic, financial, and fiscal policies that are consistently wrong: the ruling economic theory is wrong. The elites are unable to "think outside the box."

Finally, there is one extremely important reform, that, while not directly having to do with financial markets, is perhaps the most important we could undertake to begin to raise working class and middle class incomes again. That is: remove all the Reagan-era obstacles to labor organizing, and let labor unions go on an organizing tear. Any labor lawyers can tell you horror stories of how someone trying to organize their workplace was fired -- a direct violation of federal law -- but the companies and managers involved were never really brought to justice because the penalties are negligible.

In fact, there was a rescued diary on DailyKos a few nights ago, aptly named You Haven't Even Been Paying Attention about the Machinists' strike at Boeing. It included this insightful paragraph from a recent Businessweek article:

Underlying the current standoff are the poor relations Boeing has long had with the IAM. That became clear in last-minute talks between Calhoun and Blondin just before the strike began. The two were deadlocked over yet another relatively minor issue, involving worker training. Blondin recalls asking: "I just don't understand why you always fight us." Blondin says Calhoun replied: "You just don't get it. We represent Corporate America. You represent labor. We are always going to be adversaries." Boeing says Blondin's account was taken out of context.

Calhoun's Corporate America needs to be slapped down, hard, on this issue. It’s time to make the financial system and the economy work for all people, not just the well-connected few.