This is based on a comment that I made in NCrissyB's diary this morning, "Morning Feature: Where Is the Bottom? My comment talked about the nature of speculation in the housing market, the causes of the housing bubble and a recommendation for resolution. I ascribed the fundamental reason as too much wealth chasing after profits resulting in speculation and large scale debt. This is unsustainable and has had many undesirable secondary effects on our economy, not to mention the current primary effect of creating a crisis. If we can understand this problem then we can devise a solution.

NCrissyB wrote in her diary Morning Feature: Where Is the Bottom?

There is fairly widespread agreement that our economic crisis began with an over-leveraged, hyper-inflated housing market.

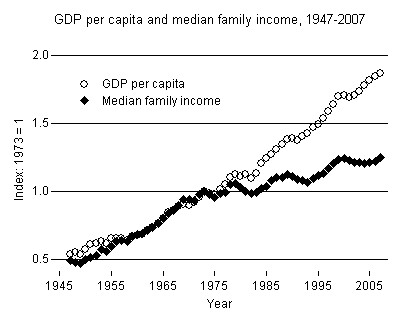

The following graph is from When did the financial crisis really start? by Jerome A Paris

The question here is why did the housing market hyper-inflate? The answer is not a simple as over-eager mortgage initiators. Although Greenspan gets some of the blame by keeping Fed rates as low as possible to prevent a recession during Bush's first term, the real culprit is excess wealth. Private mortgage debt doubled during the last 8 years. Those seven trillions of dollars came from somewhere, and it's not the median worker. We have been in a pattern of increasing income disparity since 1974 (See the above chart from Jerome). Accumulated wealth is always looking for somewhere to go. After the high tech bubble crash, money went into the mortgage market and investments derived from those. The strange anomaly during this period was that no matter how many mortgages were involved, interest rates remained at historically (for modern times) low rates. The only explanation for this was that there was a nearly endless supply of wealth wanting to go into this market.

The really serious bottom line is that there was too much wealth pushing an ever hyper-inflationary housing market. This is the worst type of investment possible, almost totally speculative. A house that sold for $100,000 in the early 90s was now selling for $450,000. Same house, same kitchen, same everything, just a bigger price tag. In a free for all market like this we can't see the forest from the trees. If you invest in technology and infrastructure your investment is building greater value in the future. The unfortunate conclusion of this line of reasoning is that an economy has a finite limit on total accumulated, invested wealth. After that, it can't provide a real return. If you invest in a hyper speculative mortgage market you are investing in nothing but individual debt.

The answer is that the investment in housing was a bad gamble and it will have to crash. The question is how much of this will be absorbed by the owner and how much by the holder of investments derived from mortgages. NCrsisyB makes the point that some of the wealth is held by retirement plans, and therefore the loss would effect all of us. That's true, but if the investment itself was fundamentally unsound then you can't make a moral argument based on some of the ownership to somehow make the investments whole.

How do we unwind from this untenable situation? Nouriel Roubini has made the point that we need to reduce the principle face value of mortgages, not just the payments. That's exactly right. Here's the bargain. You will lose some of the value of your retirement investment, in return your mortgage face value and payments will be reduced. If we don't solve this problem then I believe that the economy will completely crash and it will take a decade to unwind from debt, much of it dissolved by foreclosure. In fact my opinion is that the first great depression was resolved when hyperinflation and debt were worked out of the system. We need to do two things. Take speculation out of the housing market and reduce the face value of all mortgages on primary residences, and correspondingly reduce the value of all investments based on those mortgages.

First let's talk about taking hyper-speculation out of the Housing Market

A traditional view of the mortgage market is that is has been distorted by government interference. By insuring mortgages through Fannie and Freddie the risk of the investment has been artificially reduced encouraging risky mortgages. The second issue here is that statistical methods have been used to bundle risky mortgages into packages to create an investment vehicle of higher rating. This is problematic as all of the mortgages have some common dependencies and can crash together. The third issue is the writing of insurance policies against these risks (credit default swaps). This as the same problem as bundling and in addition it bypasses the usual regulations for writing insurance policies that are designed to eliminate fraud and excess risk.

Here's my suggestion:

Allow Fannie and Freddie to insure only qualified mortgages. Here are the terms for qualification:

- The amount of the mortgage can not exceed 100% of the structural value of the house which is determined by size, age, location, condition, etc.

- The owner must put a minimum of 20% down for a new mortgage.

- The interest rate is fixed at the time of initiation and some percentage over Fed Prime rate. The target for today's market is 5%.

- The owner must have the demonstrated ability to make the mortgage payments and taxes and insurance, by actual income or assets.

- There are some protections for the mortgage against bankrupcy proceedings.

Regulate investment vehicles containing bundled mortgages. The rating of the bundle cannot be greater than the lowest rating of any individual mortgage.

Register and regulate according to good insurance standards, any company issuing an insurance policy on investment vehicles containing mortgages.

Unqualified mortgages may be written, however they would have the following characteristics. They would be uninsured. They would be subject to bankruptcy proceedings, that is an individual may file for bankruptcy and keep his house and lose part or all of the remaining mortgage principle.

Here's the point. You can get a mortgage for any house that you want to buy at any price, however, the payments are going to be very expensive. This stops the broad middle class from getting involved with risky mortgages, and keeps these assets from becoming toxic.

Resolving the current crisis

Nouriel Roubini has suggested lowering the face value of mortgages. I agree. That leaves us with the question of how to do that and how to make it fair. From my analysis the issue is driven by hyper-speculation in the late 1990s and the 2000s. Let's say that this is what screwed the economy and we need to back out from this to reasonable mortgage principles and payments. First, the housing market needs to deflate and we are going to do that by letting it happen and encouraging it with the above qualified mortgage plan. We need to calculate the average overprice by market area. We then discount all mortgages by that amount, based on a schedule of when the original mortgage was issues. You discount all mortgages to eliminate the problem of fairness, but more importantly we are going to give the average middle class worker a lot more income to spend. Let's assume that you live in the San Francisco area and you bought your house in 2002. Your current mortgage payment is $3200 per month. We look up your region and your initiation data and your mortgage is reduced by 30%. You now have a qualified mortgage and your rate is fixed at 5%. Your payment is now $1800 per month, adjusted for reduced face value and reduced interest rate. That amounts to an additional $1400 to spend per month. I call that a stimulus.

The obvious question now is that what happens to any investment vehicles powered by this mortgage? The answer is that they are adjusted down, and the difference is considered a loss. It's just like buying GM stock two years ago. You made a bad investment, but the good news is that the new investment is very secure. As I said at the beginning someone has to lose in this crisis. If you take it out on the consumer then the economy tanks and mortgages foreclose.

I have lots more to talk about, but if you have made it this far I applaud your patience. I'll tickle your interest by making the claim that everything discussed in this diary is key to answering the questions as to why we don't have a healthy manufacturing sector and why we can't manufacture price competitive goods for the global market.

Yours in eternal gratitude to our community, The Wizard.