Back in May, I wrote a primer about the insidious McCarran-Ferguson Act, the law that excludes the insurance industry from federal antitrust regulation. One of the points made in that piece was:

If you want to take some action on healthcare, call your congressperson and tell them to support or cosponsor Pete DeFazio's bill H.R. 1583. This legislation has the insurance lobby tossing and turning at night and waking up in cold sweats. Only when the good citizens of this country are heard will the money of the insurance lobby seem less persuasive to our leaders.

After an analysis of the House healthcare bill, I'm convinced that the industry has successfully evaded federal regulation yet again.

First, you need to understand why the McCarran act is so absolutely awful. The Insurance industry, especially health insurance, is probably the worst anti-competitive industries in America next to Major League Baseball. In a report issued by Healthcare for America Now, (A MUST READ!!!)consolidations, mergers, and clear evidence of price-fixing have caused near monopolies on healthcare in many regions of the counrty. Just a few brief examples from around the country:

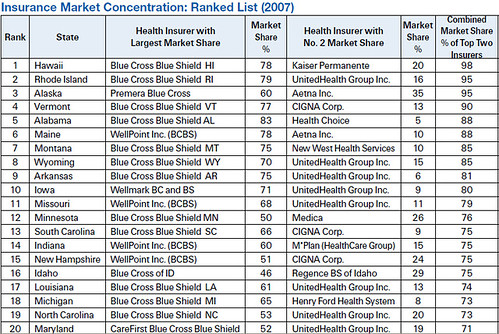

Vermont - Blue Cross/Blue Shield, 77% market share, 75% premium increase

Indiana- Wellpoint, 60% market share, 83% premium increase

North Dakota - Noridian Mutual, 89% market share, 74% premium increase

S. Carolina- Blue Cross/Blue Shield, 66% market share, 76% premium increase

Oregon- Blue Clross/Blue Shield, 67% market share, 85% premium increase

all increases are from 2000-2007

No matter region of the country you live in, you probably live in an area where there is a high degree of market concentration, unless you live in a large metropolitan area. And even then...

Take a look at this chart of the top 20 most concentrated markets:

When a firm has more than a 42 percent share of a single market, the U.S. Justice Department considers that market to be "highly concentrated" and subject to antitrust supervision at minimum. But not the healthcare insurance industry. They don't need to worry, because of the Major League Baseball-like protection the industry is given under the McCarran-Ferguson Act.

After a careful review of the H.R. 3200, and the bill reported out of the Senate HELP committee, the current on the table healthcare bills, I am now ready to report the revisions that have been to this horrible law:

Nada. Insurance competition will still remain a patchwork matter for state insurance commissioners and state attorneys-general. As the chart above indicates, these are clearly insufficient to bust up what is clearly an out-of-control oligarchy. I'm a big free market guy and even I think this is absolutely insane.

Democrats and Republicans have two different ways of dealing this problem:

Democrats propose creating a "healthcare exchange" where you would be able to compare rates and plans offered from a variety of providers, including (hopefully!) a public option, much like the Federal employee health plan. Of course, under the current bills, the only way you get into the exchange is if your employer does not provide you with a plan, you lose your job, or you're a small businessperson or freelancer. (Aside...I'm a legal industry management consultant and I get my health insurance from The Freelancers Union. It's not cheap, but its pretty good.). This is good, but it still does nothing to prevent a wave of mergers and acquisitions that would probably follow healthcare reform.

In the past 13 years, more than 400 corporate mergers have involved health insurers, and a small number of companies now dominate local markets but haven’t delivered on promises of increased efficiency. According to the American Medical Association, 94 percent of insurance markets in the United States are now highly concentrated, and insurers are thriving in the anti-competitive marketplace, raking in enormous profits and paying out huge CEO salaries.

Republicans propose allowing you to "buy insurance across borders." That way, the health insurer across the border can bring some competition to your state. Sounds good right? Wrong. This is really an attempt to subvert what little regulation exists today. What will happen is that all the insurers will go set up headquarters in the LEAST REGULATED STATE. Your state insurance commissioner in California could not stop your employer from buying a plan sold in ass-backwards Oklahoma. It is exactly what happened in Delaware and South Dakota when both states allowed no limit to interest rates on credit cards. All the credit card companies moved there, so now you're screwed everywhere.

What neither party proposes to do is remove the damn exemption to competition enforcement! Guess why.

Antitrust law was my favorite subject in law school, and I've been keeping tabs on the Antitrust Division at the Department of Justice. I have no doubt that they would go after this industry if they had the legal authority to do so.

As of today, Pete DeFazio's bill, H.R. 1583, is still stuck in a byzantine worm hole of committee review. Waxman, Frank, and Conyers all have jurisdiction but aren't moving it. Conyers did at least refer it to a Subcommittee run by Hank Johnson of Georgia. On the Senate side, Leahy has not re-introduced the bill he introduced in the 110th Congress which had some surprising co-sponsors: Lott, Reid, Landrieu, and Specter.

I had hoped something like DeFazio's bill would have been snuck into one of the healthcare bills, but no. Apparently the Democrats have concluded there will be separate legislation or none at all.

The President's position during the campaign has always been for much more stepped up antitrust enforcement and he has delivered on this. But if he really wanted to start taking the meat axe to the health insurance indusrty, he should support DeFazio's bill and sic the Justice Department on them. That is the simplest and most effective means to get them to cry uncle.

P.S. - I was supposed to publish this yesterday but I got really busy. Much apologies to those of you who were looking for it.