The BLS released its Employment Situation report today and the results came in with an adjusted loss of 11,000 and an unadjusted gain of 80,000. The widely reported U-3 unemployment rate came in at 10% (unadjusted was 9.4%) and the much more accurate U-6 rate was 17.2%. What all of this means is that the economy looks like it is getting close to job creation even though we are still in quite a hole and that we have a long slog ahead of us before we can even hope to see full employment again (and the full employment percentage may be moved higher because of a permanent adjustment to the economy anyways).

Update: Here is a link to my analysis on the seasonal adjustments and birth/death adjustments.

A few other important pieces of information from the report showed that the employment-population ratio (probably the most complete summary of employment) came in at 58.5, which is still abysmal and the labor force participation rate was 65. Finally, the seasonal adjustment used was -.928%, which compares to the five year average of -.80 (what this means is that using the average adjustment we would have seen the creation of 158,000 jobs instead of the loss of 11,000), and the birth/death adjustment was 80,000, which compares to the average of 36,000 for the month.

Keep in mind that it takes approximately a job creation rate of +100,000 a month just to absorb new entrants to the market and that this correlates to an approximate growth rate of 2.8% (from Bernanke's testimony yesterday and a number I hadn't heard before). What this all means is that we have a long way to go before the job market can really hope for stability and growth.

The elephant in the room with the job market is government stimulus, as the private sector seems loathe to hire new employees on the fear that once stimulus is removed, the economy will dip again and this is a huge problem since the government simply cannot afford to stimulate forever (although we have been essentially doing this to some extent for the last 40 years).

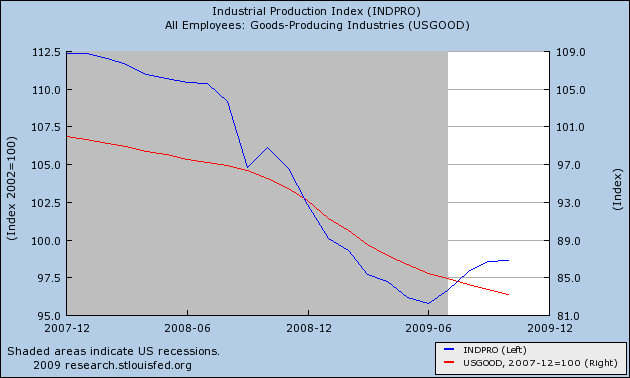

This fear of the future can be best shown in industrial production

which has not only fallen less than goods producing employment, but has also started to recover, while goods producing jobs continue to fall. The fear also can be shown in productivity increases, which come while unit labor costs continue to fall. While the productivity number was revised down from its previous report of 9.5%, an 8.1% gain is simply huge and would normally indicate hiring should be near (but likely isn't do to fear).

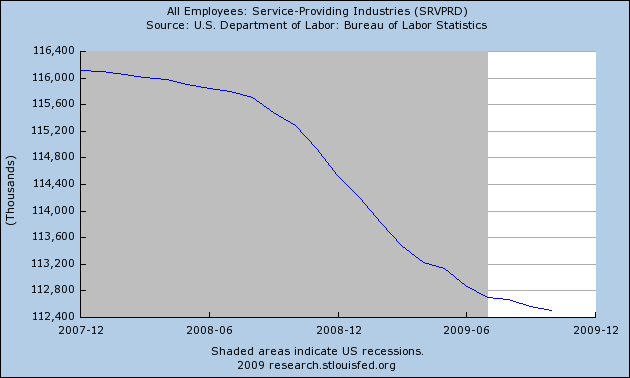

Finally, initial jobless claims continue to fall (and quite dramatically), but have so far have not turned out to be positive for job creation like some have hypothesized, which is most likely from a fear to hire even though layoffs have declined. The other factor at play besides fear (or perhaps linked to the fear) is the continued decline of service jobs,

which we haven't experienced during a recession since the depression. This is evidenced by the ISM non-manufacturing index that came out this week which showed that

Veiling a big improvement in new orders, the ISM's non-manufacturing composite index tumbled backwards, down nearly 2 points to a sub-50 and sub-par 48.7. But new orders, one of four evenly weighted components in the composite, show a significant month-to-month increase, at 55.1 vs. October's even more positive 55.6. There could be little better news for the economy than a bulk of new orders being put in place. Improvement in jobs, however, is still the central focus and today's report is very downbeat with an index of 41.6 to show significant deterioration and combined with a similar reading in October point to a turn lower in trend.

This is not good news for jobs, as that 40 reading on the employment index is still very negative.

In summary, November's jobs report was fantastic and it looks like we may finally see some real job growth next month.

UPDATE: the revisions to prior months were also great, with September being revised from a loss of 219,000 down to a loss of 139,000 and October going from down 190,000 to down 111,000. More great news.

Update 2: For those interested in reading the take of the guy who has been right all along on the economy, please head over to Bonddad's Blog.