A lot of people wax poetic on the theoretical aspects of health insurance. Some people have always had an employer plan. That's nice, if you can get it. Some of them have never been off their parent's plan, and that's also great if you can get it. But some of us have been out in the open market and trying to get insurance. We have chased down the information, wrestled with the middlemen, spent untold hours trying to analyze the availability and costs, and choosing from the few options we ended up with.

This is my story of that process, and with the new MA insurance system. Take-home message: Things are a lot better here than they used to be.

Before your heads explode, consider this: I know this MA system is flawed. I would rather there was a public option. I have worked for a federal public option in the streets and on the phones. But our little experiment here is not necessarily the fount of most evil that you may have been led to believe.

I decided to start my own business in 2001. I was going to quit my job in 2002, and become an independent contractor. I had a number of fears around this, but the top one was health insurance. What was I going to do about that?

Working with a career coach, I worked through some of the logistics. He told me that usually people would join a local small biz group (Chamber of Commerce, or something like SBANElocally). I used the COBRA for the first year or so. But then I joined SBANE to get access to the insurance. There was a fee to join--by the way.

But I had access to about 4 health plans. I picked one that I had prior experience with, and that my family has had good experiences with, Tufts. I picked the basic, low-end plan. As I don't have any prescription needs for chronic conditions, I chose not to take prescription coverage.

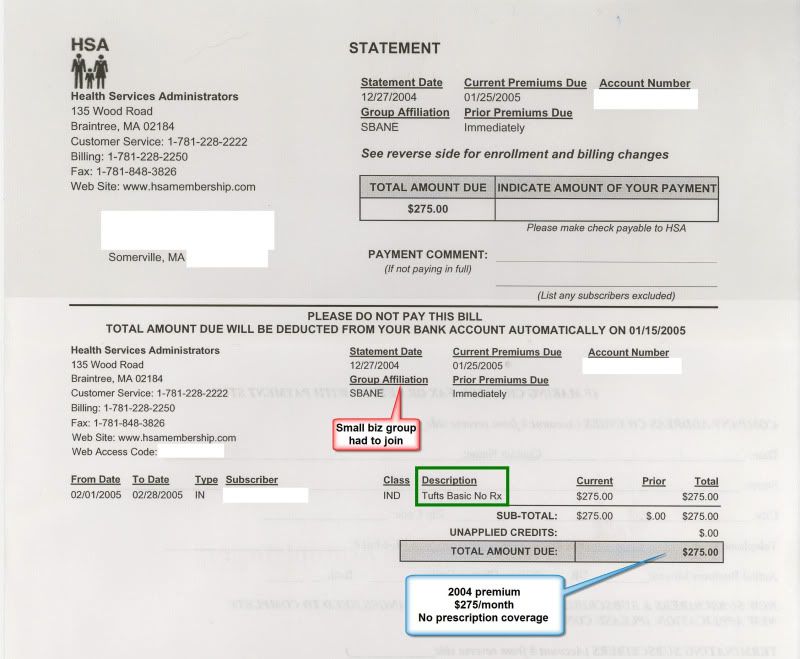

By 2004, this meant a plan that cost $275/month, or $3300/year.

Figure 1. Shown here is one of my bills for this plan as evidence, with my account number and address stuff redacted. 2004 premium for Tufts Basic insurance, no prescription coverage. $275/month. This is for an individual. It required membership in a small business association of some sort to get access to the group rates at all. Click to see it full size.

Figure 1. Shown here is one of my bills for this plan as evidence, with my account number and address stuff redacted. 2004 premium for Tufts Basic insurance, no prescription coverage. $275/month. This is for an individual. It required membership in a small business association of some sort to get access to the group rates at all. Click to see it full size.

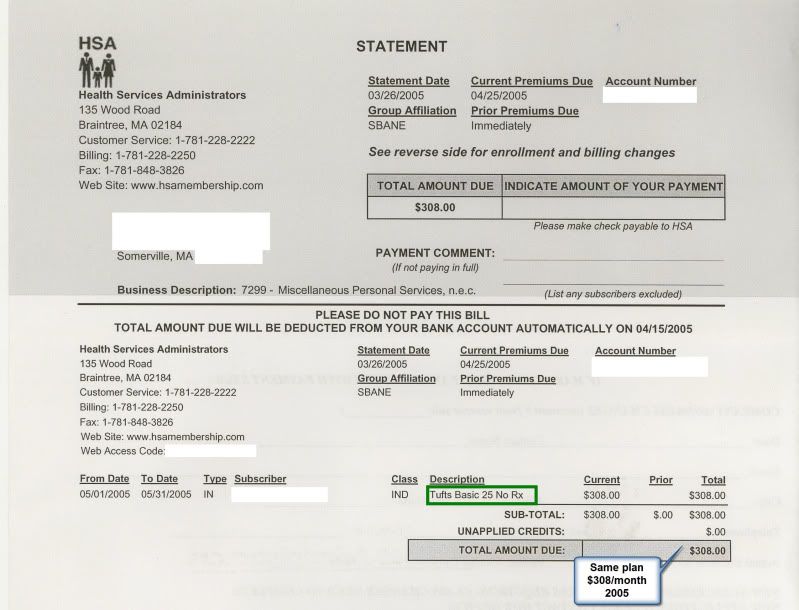

By 2005, this meant a plan that cost $308/month, or $3696/year. That's a 12% increase for the same plan. All of the plans increased about the same, so there was no advantage to switching plans. There also wasn't that much choice. And it was not very easy to compare plans. Further, other business groups seemed to all have the same options pretty much.

Figure 2. Shown here is one of my bills for this plan as evidence, with my account number and address stuff redacted. 2005 premium for Tufts Basic insurance, no prescription coverage. $308/month. This is for an individual. It required membership in a small business association of some sort to get access to the group rates at all. Click to see it full size.

Figure 2. Shown here is one of my bills for this plan as evidence, with my account number and address stuff redacted. 2005 premium for Tufts Basic insurance, no prescription coverage. $308/month. This is for an individual. It required membership in a small business association of some sort to get access to the group rates at all. Click to see it full size.

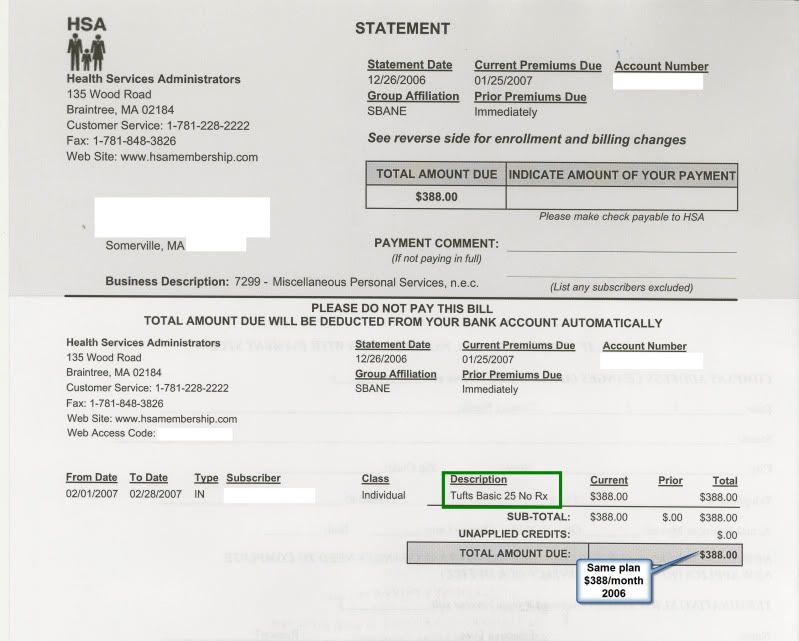

By 2006, this meant a plan that cost $388/month, or $4656/year. That's a 25+% increase for the same plan. That's 1 year before the new system kicked in. There's no justification for that kind of increase annually.

Figure 3. Shown here is one of my bills for this plan as evidence, with my account number and address stuff redacted. 2006 premium for Tufts Basic insurance, no prescription coverage. $388/month. This is for an individual. It required membership in a small business association of some sort to get access to the group rates at all. Click to see it full size.

Figure 3. Shown here is one of my bills for this plan as evidence, with my account number and address stuff redacted. 2006 premium for Tufts Basic insurance, no prescription coverage. $388/month. This is for an individual. It required membership in a small business association of some sort to get access to the group rates at all. Click to see it full size.

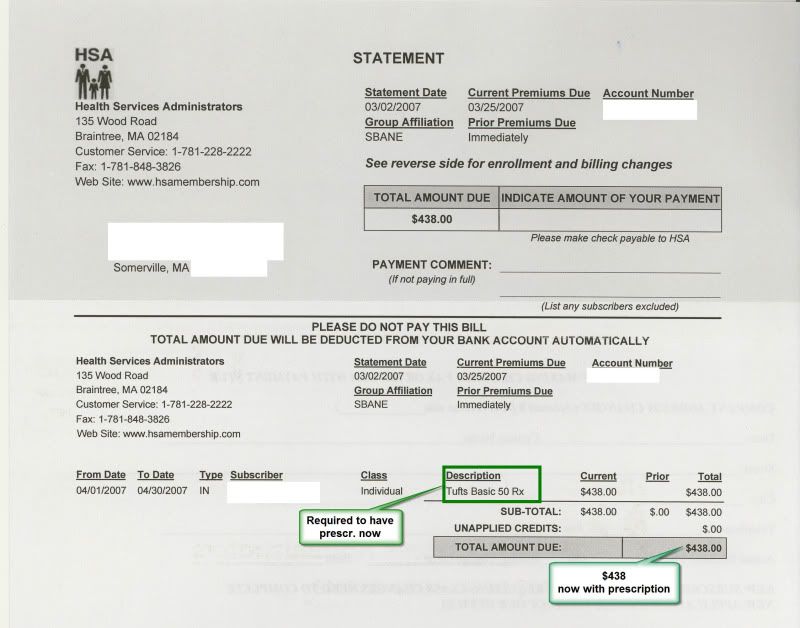

In 2007, everything changed. The new MA laws were going to be implemented, that included the mandate to be insured (and to carry some prescription coverage). So when I had to re-enroll early that year, I had to pick a new plan that carried prescription coverage--despite still not having any need for prescriptions on a regular basis. But I understand the mandate is a way to spread the risk around, and I get that. That increased my premium, though. Now I was paying $438/month, or $5256/year. But I had to pick the new plan in my open enrollment window, the state plans had not been established at this point and I didn't know what was coming. So I had to pick one from the existing list.

Figure 4. Shown here is one of my bills for this plan as evidence, with my account number and address stuff redacted. 2007 premium for Tufts Basic insurance, now with prescription coverage. $438/month. This is for an individual. It required membership in a small business association of some sort to get access to the group rates at all. Click to see it full size.

Figure 4. Shown here is one of my bills for this plan as evidence, with my account number and address stuff redacted. 2007 premium for Tufts Basic insurance, now with prescription coverage. $438/month. This is for an individual. It required membership in a small business association of some sort to get access to the group rates at all. Click to see it full size.

Around May of 2007, though, I got my hands on the new "exchange" tool that the state had developed. It is called the Commonwealth Connector. I looked at the site, and it was a pain to enter some of the data (some kind of code for my business--whatever; they changed some of that now, it's even easier). But I entered my data, and looked at my options.

Quite frankly, I was pretty impressed. And I use a lot of software interfaces (I'm a professional software trainer). It had never been so easy to look at the plans side-by-side and see what they did or did not cover, and what the deductibles were. Here's what I'm entering to create the shot I'll show below.

Make these choices (or set your own if you like):

- Click Individuals and Families image from the homepage

- Family size: 1 (click continue)

- My income exceeds the Commonwealth Care threshold, so click the "Shop for Insurance Now" arrow.

- Zip: 02144

- Self only

- Enter a birthday between 1963 and 1966

- Coverage in January 2010

Then you can check out the bronze, silver, and gold plans. As I mentioned, I have no chronic issues and do not use much health coverage. I'm picking bronze. It is probably also most comparable to the plans I had in the past. But feel free to look at the others.

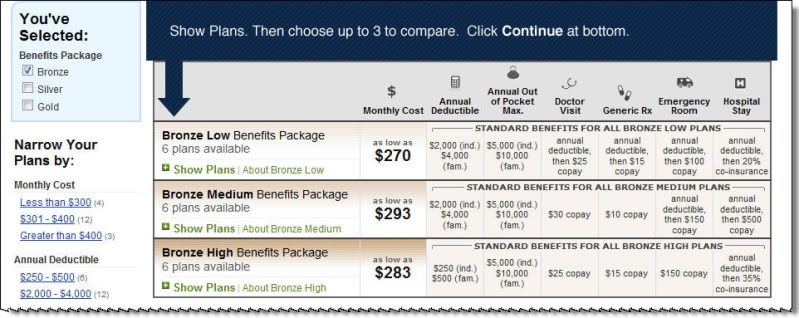

Figure 5. The Massachusetts Bronze options interface. You can see the tiers within the Bronze options, and open up any to see more details about the plans. I never had this much information in such an easy-to-see manner before. This is a little better than it was at first, too, but stuff can get better over time with feedback and usage.

In 2007, I got insurance via the Connector for $269/month, or $3228/year. This is lower than my 2004 premiums, and includes prescription coverage and does not require a joining fee. Remember: before the exchange I was up to $438/month, or $5256/year. That's about 40% less. Also remember that I no longer have to buy into a member group like the Chamber of Commerce with those dues. I did choose a higher deductible, because I could as I now HAD a choice, and because that's appropriate in my situation.

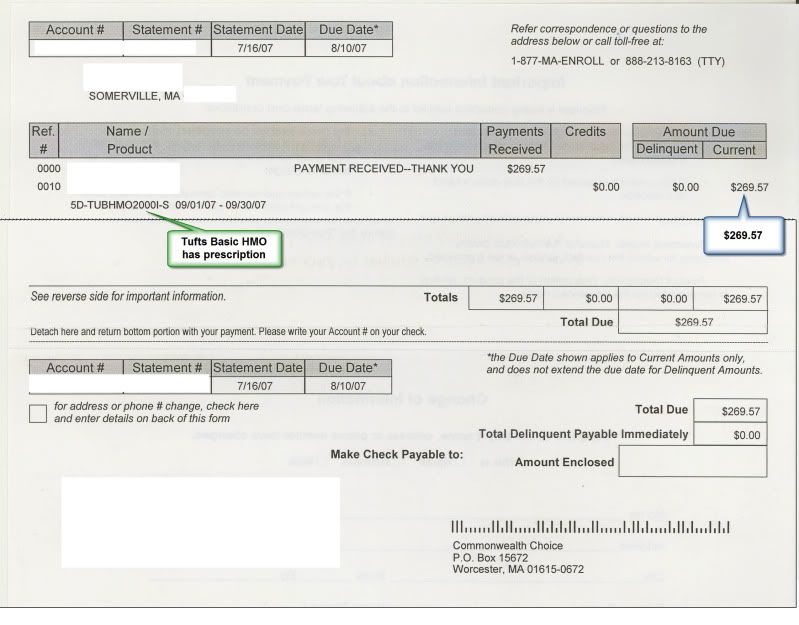

Figure 6. Shown here is one of my bills for this Commonwealth Connector plan as evidence, with my account number and address stuff redacted. 2007 premium for Tufts Bronze insurance, with prescription coverage. $269/month. This is for an individual. It does not require membership in a small business association of some sort to get access to the group rates at all. Everyone in the state has the same access as I do. Click to see it full size.

Figure 6. Shown here is one of my bills for this Commonwealth Connector plan as evidence, with my account number and address stuff redacted. 2007 premium for Tufts Bronze insurance, with prescription coverage. $269/month. This is for an individual. It does not require membership in a small business association of some sort to get access to the group rates at all. Everyone in the state has the same access as I do. Click to see it full size.

My rate stayed the same all through 2007-2008, and recently went up to $291/month for the same plan. That's about an 8% increase--a smaller increase than I ever saw before. (Figure not shown, current premium bill available if you need to see that.)

So this is my experience. My insurance is now cheaper both in premiums and in the fact that I don't have to join a business association to get access. I have more choice. It feels very transparent to me: I don't feel like the next guy is getting some break because he knows someone who knows someone. And I feel like I have more people in my boat now: I could complain to the state regulators if things were going awry for some reason. There's actually some comfort in that for me that we are in this together.

I was concerned at one point. It did need to be monitored to make sure businesses weren't doing squirrelly things to get out of insuring people--and some of them did. But not as bad as I feared. And Mitt did knee-cap the system by setting a low fee for businesses that wouldn't insure their staff. I would prefer, though, that insurance wasn't tied to employment anyway, that doesn't make any sense to me. Employers are not specialists in this in general, and I think keeping your medical records away from your employer is also a good thing. And you shouldn't have to worry about this to change jobs.

As much as I prefer what I have to some of the crappy proposals I've seen coming out of the ethers, I also recognize the need for a 50 state solution. As a virtual company with people in 4 states, I've seen firsthand as my colleagues tried to get insurance. Our experiences vary widely, and we ended up with nothing comparable to each other. We tried to get a solution for all of us, but as many are regional we couldn't. We thought we were close on one solution, but when they wouldn't insure our gay business partner's family we bailed. We won't throw his family under the bus. Think about this: same-sex married families are not insurable everywhere right now. But in Massachusetts they are.

A strong federal public option is my second choice; single payer is my first. But I accept that some things are done as baby steps. I accept that we can't get everything we want on the first pass at this because it is a massive system and a lot of people fear changing it--we also lack some infrastructure that would be needed to re-engineer the whole thing.

Recent data shows we had 96% coverage of taxpayers after the first full year. Again, not perfect, but we keep learning more as well and we can work on filling the gaps. I'm sure you've heard some horror story. You probably haven't heard the quiet stories people tell me when I tell mine. For example, Kitty, revsue, and lesliet have spoken up, among others.

My conclusion: The MA plan is not perfect, but it is better than it used to be for this individual and small business person. I have spoken to other small business people here that say exactly the same thing. I hope we can make it better. But this mandated and unPOed system is not necessarily the spawn of Satan some people would have you believe.

Maybe your plan is better. Great. Show me the data. Real data, not fear, not innuendo, not hyperbole, not rumor or hysterical claims. Show me the data. And think about whether other options might be effective in some ways if your sacred strategy doesn't deliver. Is it worth abandoning all the other pieces?

Disclaimer: I do not work for any insurers, and I have no relationship with them--though I'm sure I'll be accused of that. I have no contact with AHIP or FDL or any of the other groups on this. I am flying solo here. I am a lifelong Kennedy-esque Dem and have never voted for a republican in my life (I think I've met a couple, though. But not many.) This is my first-hand experience and my data in a real-life situation. YMMV.