Ben Bernanke’s term as chairman of the Federal Reserve ends on January 31, and the vote to confirm his reappointment will probably take place on Thursday or Friday. But the really important vote – on cloture of the hold placed by Sen. Bernie Sanders – will likely be tomorrow or Thursday. The vote on cloture requires 60 votes, and is the best opportunity to stop the reappointment. And stopping the reappointment of Bernanke is the best opportunity to let our leaders in Congress and the White House know just how unhappy you are with their economic and financial reform policies thus far.

Yves Smith on Naked Capitalism yesterday had a great summary of the pertinent facts, including tables of which Senators are undecided or uncommitted: Tell Senate "No" on Bernanke Cloture

Smith points out that a Senator can easily pose as being against Bernanke while still doing Wall Street’s bidding by voting for cloture, but then voting against Bernanke.

And if you don’t believe that keeping Bush-appointed Republican Bernanke as Fed head is doing Wall Street’s bidding, here’s Kos himself: Vote down Bernanke, the world ends

WHAT TO SAY

On Naked Capitalism, Yves advises:

What To Say: Make it simple so as to not tie up the lines ... "Vote No on Cloture to end debate on Bernanke. I am opposed to the reappointment of Bernanke [give your personal reason] and I think we should start all over on health care [or whatever you think about that issue].

JUDGING BERNANKE ON HIS RECORD

There are a surprising number of people here on DailyKos who apparently believe Bernanke has done a good job and saved us from sliding into a Second Great Depression. I’ll discuss the 2GD issue at the end; for now, I just want to repeat what Yves Smith pointed out: Bernanke failed to examine the health of the major investment banks and plan for a failure even after the collapse of Bear Stearns. What was Bernanke and the Fed doing in the almost six months between the collapse of Bear Stearns and the collapse of Lehman Brothers? Assuring the nation and the world that the "problem has been contained." And now, after Lehman’s collapse, there are still no plans to handle the collapse of Citigroup or JP Morgan Chase or Goldman Sachs, or to make them smaller. Yves Smith believes that

Unreconstituted, unreformed, and more concentrated, the financial system will break down again, likely in a more spectacular way.

Yves links to a post on Pragmatic Capitalism which notes that Wall Street may be looking forward to another Bernanke term of almost free money for the banksters, but Main Street has an entirely different story:

This so-called expert on the Great Depression completely missed the Great Recession coming and then took credit for saving the world from a second Great Depression despite few signs that his actions have actually done anything to help the recession on Main Street. What we have learned over the course of the last year is that Bernanke actually worsened the problem of too big to fail, has failed as a regulator and has only increased the financial strains on a government that is already in over its head. . . .

Unfortunately, as we’ve learned over the course of the last year, what’s good for Wall Street is not always good for Main Street. The boom/bust policies of the Federal Reserve have not worked over the course of the last 15 years and the public wants real change.

Bernanke’s economic philosophy remains unrepentant "neo-liberalism" (efficient financial markets, free markets are better at allocating resources than governments, and free trade benefits all). Australian economist Steve Keen explains why Bernanke’s economic beliefs are simply wrong, wrong, wrong: Steve Keen: The Economic Case Against Bernanke

Bernanke is popularly portrayed as an expert on the Great Depression—the person whose intimate knowledge of what went wrong in the 1930s saved us from a similar fate in 2009.

In fact, his ignorance of the factors that really caused the Great Depression is a major reason why the Global Financial Crisis occurred in the first place. . . .

Bernanke is a leading member of the "neoclassical" school of economic thought that dominates the academic economics profession, and that school continued Fisher’s pre-Great Depression tradition of analysing the economy as if it is always in equilibrium.

With his neoclassical orientation, Bernanke completely ignored Fisher’s insistence that an equilibrium-oriented analysis was completely useless for analysing the economy.

WILL THE FINANCIAL MARKETS CRASH IF BERNANKE IS TOSSED?

So now I have to address those of you who agree with Versailles and The Village that it would be irresponsible to discard Bernanke, because that would cause crisis in the financial markets since he is doing a great job keeping us out of a Depression, and is basically only the only person in the world who knows how to do the job.

First, do you really care what these guys think? They’re laughing at you, man. Laughing at you!

This is the license plate of Robert Kindler, a vice chairman at Morgan Stanley who is one of the firm’s top mergers and acquisitions advisors, according to New York Times financial columnist Andrew Ross Sorkin, author of the recent book, Too Big to Fail: How Wall Street and Washington Fought to Save the Financial System — and Themselves. Kindler sent Sorkin a note claiming "he had ordered the plate as a satirical reminder that ‘no one is too big to fail.’ "

Here is the plain fact: You can either save the financial markets. Or you can save the country.

Why? Because the financial system does not serve its purpose of allocating society's resources to solve society's problems. Case in point: we are more dependent than we were three decades ago, not just on fossil fuels, but on IMPORTS of fossil fuels.

The financial system is worse than worthless: it has become an obstacle to society's ability to solve problems.

Wall Street has manipulated the credit mechanism of the economy in such a way that credit no longer flows to real industry, but to speculation, usury, and "economic rent." (See, for example, Complexity as rent.)

In Debunking the Myth of the Financial Markets, I explain that

The fundamental problem is the big players on Wall Street have misused the credit mechanism of the economy for their own private gains through the bloating of debt and speculation, at the expense of actually allocating and supplying capital to the real economy. The dollar volume of financial trading has increased nearly forty-fold since the 1960s, but almost none of that trading is of any use to the real economy. Even now, after the collapse of September 2008, big Wall Street firms like are still making most of their money by trading for their own account.

There are some stunning graphs which show that the financial system is actually subtracting capital from the real economy, rather than adding capital.

And here's William Black on How the Servant Became a Predator: Finance’s Five Fatal Flaws:

- The financial sector harms the real economy.

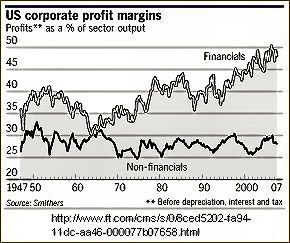

Even when not in crisis, the financial sector harms the real economy. First, it is vastly too large. The finance sector is an intermediary — essentially a "middleman". Like all middlemen, it should be as small as possible, while still being capable of accomplishing its mission. Otherwise it is inherently parasitical. Unfortunately, it is now vastly larger than necessary, dwarfing the real economy it is supposed to serve. Forty years ago, our real economy grew better with a financial sector that received one-twentieth as large a percentage of total profits (2%) than does the current financial sector (40%). The minimum measure of how much damage the bloated, grossly over-compensated finance sector causes to the real economy is this massive increase in the share of total national income wasted through the finance sector’s parasitism.

Second, the finance sector is worse than parasitic. In the title of his recent book, The Predator State, James Galbraith aptly names the problem. The financial sector functions as the sharp canines that the predator state uses to rend the nation. In addition to siphoning off capital for its own benefit, the finance sector misallocates the remaining capital in ways that harm the real economy in order to reward already-rich financial elites harming the nation. The facts are alarming:

• Corporate stock repurchases and grants of stock to officers have exceeded new capital raised by the U.S. capital markets this decade. That means that the capital markets decapitalize the real economy. Too often, they do so in order to enrich corrupt corporate insiders through accounting fraud or backdated stock options.

• The U.S. real economy suffers from critical shortages of employees with strong mathematical, engineering, and scientific backgrounds. Graduates in these three fields all too frequently choose careers in finance rather than the real economy because the financial sector provides far greater executive compensation. Individuals with these quantitative backgrounds work overwhelmingly in devising the kinds of financial models that were important contributors to the financial crisis. We take people that could be conducting the research & development work essential to the success of our real economy (including its success in becoming sustainable) and put them instead in financial sector activities where, because of that sector’s perverse incentives, they further damage both the financial sector and the real economy. . . .

• The financial sector’s fixation on accounting earnings leads it to pressure U.S manufacturing and service firms to export jobs abroad, to deny capital to firms that are unionized, and to encourage firms to use foreign tax havens to evade paying U.S. taxes.

• It misallocates capital by creating recurrent financial bubbles. Instead of flowing to the places where it will be most useful to the real economy, capital gets directed to the investments that create the greatest fraudulent accounting gains. . . The FBI began warning of an "epidemic" of mortgage fraud in its congressional testimony in September 2004. It also reports that 80% of mortgage fraud losses come when lender personnel are involved in the fraud. (The other 20% of the fraud would have been impossible had these fraudulent lenders not suborned their underwriting systems and their internal and external controls in order to maximize their growth of bad loans.)

• Because the financial sector cares almost exclusively about high accounting yields and "profits", it misallocates capital away from firms and entrepreneurs that could best improve the real economy . . . and could best reduce poverty and inequality . . .

• It misallocates capital by securing enormous governmental subsidies for financial firms, particularly those that have the greatest political power and would otherwise fail due to incompetence and fraud.

- The financial sector produces recurrent, intensifying economic crises here and abroad.

. . . . The financial sector has become far more unstable since this crisis began and its members used their lobbying power to convince Congress to gimmick the accounting rules to hide their massive losses. Secretary Geithner has exacerbated the problem by declaring that the largest financial institutions are exempt from receivership regardless of their insolvency. These factors greatly increase the likelihood that these systemically dangerous institutions (SDIs) will cause a global financial crisis.

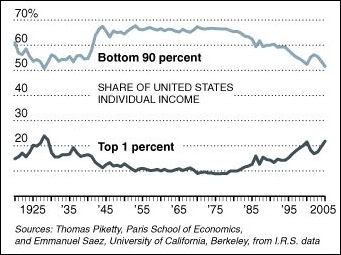

- The financial sector’s predation is so extraordinary that it now drives the upper one percent of our nation’s income distribution and has driven much of the increase in our grotesque income inequality.

- The financial sector’s predation and its leading role in committing and aiding and abetting accounting control fraud combine to:

• Corrupt financial elites and professionals, and

• Spur a rise in Social Darwinism in an attempt to justify the elites’ power and wealth. Accounting control frauds suborn accountants, attorneys, and appraisers and create what is known as a "Gresham’s dynamic" — a system in which bad money drives out good. When this dynamic occurs, honest professionals are pushed out and cheaters are allowed to prosper. Executive compensation has become so massive, so divorced from performance, and so perverse that it, too, creates a Gresham’s dynamic that encourages widespread accounting fraud by both financial firms and firms in the real economy.

As financial sector elites became obscenely wealthy through predation and fraud, their psychological incentives to embrace unhealthy, anti-democratic Social Darwinism surged. While they were, by any objective measure, the worst elements of the public, their sycophants in the media and the recipients of their political and charitable contributions worshiped them as heroic. Finance CEOs adopted and spread the myth that they were smarter, harder working, and more innovative than the rest of us. They repeated the story of how they rose to the top entirely through their own brilliance and willingness to embrace risk. All of their employees weren’t simply above average, they told us, but exceptional. They hated collectivism and adored Ayn Rand.

- The CEO’s of the largest financial firms are so powerful that they pose a critical risk to the financial sector, the real economy, and our democracy.

The CEOs can directly, through the firm, and by "bundling" contributions of its officers and employees, easily make enormous political contributions and use their PR firms and lobbyists to manipulate the media and public officials. The ability of the financial sector to block meaningful reform after bringing the world to the brink of a second great depression proves how exceptional its powers are to corrupt nearly every critical sector of American public and economic life. The five largest U.S. banks control roughly half of all bank assets. They use their political and financial power to provide themselves with competitive advantages that allow them to dominate smaller banks.

This excessive power was a major contributor to the ongoing crisis. Effective financial and securities regulation was anathema to the CEOs’ ideology (and the greatest danger to their frauds, wealth, and power) and they successfully set out to destroy it. That produced what criminologists refer to as a "criminogenic environment" (an atmosphere that breeds criminal activity) that prompted the epidemic of accounting control fraud that hyper-inflated the housing bubble.

The financial industry’s power and progressive corruption combined to produce the perfect white-collar crimes. They successfully lobbied politicians, for example, to legalize the obscenity of "dead peasants’ insurance"(in which an employer secretly takes out insurance on an employee and receives a windfall in the event of that person’s untimely death) that Michael Moore exposes in chilling detail. State legislatures changed the law to allow a pure tax scam to subsidize large corporations at the expense of their taxpayers.

THE CRIMINALITY OF WALL STREET

Now, either you believe that Wall Street is engaged in criminal behavior, or you don't. Two weeks ago, the U.S. District Attorney for the Southern District of new York (which has Wall Street in its venue), complained

We had a lot of trouble with the Treasury Department" in his recent case against Credit Suisse, in which the bank coughed up $536 million and admitted to aiding Iran and other rogue nations in violating economic sanctions. The feds, as they did in a similar settlement with the British bank Lloyds, wanted only civil penalties.

In fact, the evidence of Wall Street's criminality is so overwhelming that in September of last year, a federal judge rejected the SEC's proposed settlement with Bank of America:

[T]he parties were proposing that the management of bank of America – having allegedly hidden from the Bank’s shareholders that as much as $5.8 billion of their money would be given in bonuses to the executives of Merrill who had run that company nearly into bankruptcy – would now settle the legal consequences of this lying by paying to the S.E.C. $33 million more of the their shareholder’s money.

This proposal to have the victims of the violation pay an additional penalty for their own victimization was enough to give the court pause.

Then Judge Rakoff starts talking like a regular person. . . about fairness:

It is not fair, first and foremost, because it does not comport with the most elementary notion of justice and morality, in that it proposes that the shareholders who were the victims of the Bank’s alleged misconduct now pay the penalty for that misconduct.

Then, he calls a spade a spade:

Overall, indeed, the parties submissions, when carefully read, leave the distinct impression that the proposed Consent Judgment was a contrivance designed to provide the S.E.C. with the façade of enforcement and the management of the Bank with a quick resolution to an embarrassing inquiry..."

The beast of Wall Street should have been - and could have been - beheaded. We should have been, right now, in the middle of the process of breaking up Goldman Sachs, JP Morgan Chase, Citigroup, Bank of America, Morgan Stanley, Wells Fargo, and a few other giant financial firms. Instead, we get the Treasury Secretary undercutting the President's rhetoric (never mind actions) about "too big to fail," and Banks already finding ways around Obama financial reforms.

Until the American people see a ruthless prosecution of the banksters, that actually removes hundreds, even thousands, of top Wall Streeters from their positions, all the talk will be seen as just that, mere talk.

And I'll go even further: until thousands, of top Wall Streeters are removed from their positions, there can be no remedy for the country's economic woes. Because the simple fact – the simple fact that President Obama, Summers, Pflouffe, and almost all Democrats in power seem unwilling to even contemplate - is that the financial system does not help the real economy, but is actually looting it.

Matt Taibbi wrote back in October:

I heard a story recently from a Democratic Party operative who tells me that certain members of one of the president’s cabinet departments only got wind of how hard it is out there for ordinary people to pay their bills when they invited in a major corporation to give them a presentation about their financial outlook for the holiday season — and through that report found out that this company’s prospective customers were spending less because large numbers of them had been laid off, or had huge medical bills, or had maxed out their credit, and so on.

Letters from customers, survey answers and such, were read to the cabinet group. And they were shocked. This is how they find out about the economic reality of this country — accidentally, from a major campaign contributor! That’s how out of touch these people are.

WHAT HAPPENS IF BERNANKE IS REAPPOINTED

First of all, it will be another signal that the Obama administration has no intention of implementing fundamental change. But even more worrisome is the message sent by capitulating once again to the demands of the financial markets. Can you see the trend here? In September 2008 we were told the world economy would crash and we would even be under martial law if the Wall Street bailout were not passed. Now we're being told that teh financial markets will crash of Bernanke is not confirmed for a second term. How much longer until we start hearing that "The markets will crash if social security isn’t cut"? Or, "It’s irresponsible to oppose the slashing of Medicaid when we’re half-way through entitlement reform"?

Keeping Bernanke is a sure fire way to make sure nothing fundamental will change and we’ll remain on the course we are on now, and have been for the past three decades, since the Reagan Revolution:

A few days ago, I heard from an attorney in a large Great Lakes city whose business of traffic court cases, probate filings, and small business licenses, and home sales closings used to keep him so busy he hardly ever ate lunch and he used a small armada of cell phones and beepers to direct and deploy his small staff of three or four as they ran around the city gathering documents and signatures and making filings. Since the "recession" began his business serving the legal needs of the working class struggling its way into the middle class has simply fallen dead on the floor. Working people just don’t have the money for legal muscle anymore (adding yet another disadvantage to their existence). But he's scraping by, doing LOTS of short sales, where the homeowner has to get permission from the mortgage holder to sell for less than the mortgage amount.

"You mean the banks are starting to loan money for home sales again?" I asked.

"No," he replied. "But there are some incredible deals. Houses are going for $15,000 or $20,000."

Wow, that’s pretty remarkable: just two years ago you couldn’t touch a three-flat in that town for less than a half million dollars, and single family homes were well over a quarter million. So I asked, "Where are these houses located?"

"Well, they're not in good areas."

That made sense; I just couldn’t believe $500k three-flats were going for less than $50k now. But there was still one thing that puzzlied me.

"And if the banks still aren't lending, then who’s buying these deals?"

A brief pause, before the reply: "The only people that have cash now. Drug dealers."

Last night, when I related this recent phone call, a few expletives streamed out at the people who thought there were "green shoots" just a half year ago. I mean, don’t people think about things such as: what are the social implications of having the housing stock of entire urban neighborhoods owned by drug dealers in the next few years?

I'll leave you with this:

Will Extreme Economic Inequality Lead to Terrorism? A Chilling Moment on NPR’s OnPoint

by Bruce Judson on October 20th, 2009

Last week, It Could Happen Here was the subject of a 45-minute segment of Tom Asbrook’s OnPoint, which airs nationally on NPR. To demonstrate, how inequality can divide a nation, It Could Happen Here, which is a nonfiction book, opens with a fictional scenario involving American terrorists who threaten the nation with dirty bombs demanding an end to foreclosures by "vulture banks," and free access to healthcare and higher education for all. Tom Ashbrook asked hard questions about this scenario. I said to him think of a laid off engineer who works with radioactivity to create medical devices...

Here’s the transcript of the discussion:

BRUCE JUDSON: First off, here’s a flash point for you. In the scenario, in the fictional scenario, I talk about...It is very easy to imagine that an engineer, or someone else with the necessary knowledge who works on, let’s say, medical devices and has used radioactivity to create a better world.... to save lives, is laid off. You can imagine that he suddenly is facing foreclosure. He’s an educated person unable to put his kids through college.

A few minutes later the show took calls. The show received a chilling call from an out of work nuclear engineer–who had helped to build 13 nuclear power plants but had not worked in two years. You can read the transcript of his call below, or click to listen to his call here.

TOM ASHBROOK: Certainly inequality’s a big issue. Let me get a call right here from New London, Connecticut. And

Don. Hi, Don. You’re on the air.

CALLER: Hi.

TOM ASHBROOK: Hi.

CALLER: I think you should be listening to this guy, Judson. I’m an unemployed nuclear engineer. I’ve worked on 13 nuclear power plants. Making a dirty bomb is not a big deal. I’m not going to go out and tell everybody now to do it, but I’m just saying things like that can happen. And it sounds like you’re just being dismissive of all his ideas and what he’s saying. Because there’s a lot of anger out here, and there are a lot of people who feel that the American Dream is slipping away from them, they don’t have a chance. And the only entrepreneurial opportunity for them is to sell drugs and to be an outlaw. It’s happening.

TOM ASHBROOK: [OVERLAPPING] I hear you, [PH] Don. We’ve got Bruce on for an hour. So, I can’t say we’re not listening to him. But let me ask you, you’ve got a lot of expertise in your field, nuclear engineering. But does that mean you’re unhappy if you’re unemployed? Do you really feel like the country’s ready to revolt?

CALLER: I’m not an expert in revolution, and I don’t really know how they happen. All I know is I’m 60 years old. There’s not a lot of people who want to hire a nuclear engineer who’s 60 years old. And there are a lot of people out there like me who are out there who, you know, once you have so much gray hair, you’re out of here. And there’s just a lot of people that are just not happy with the way that the country’s going right now.

And I don’t know...where it’s going to take it, or what’s going to be its spark, or what’s going to be the event. But people feel like there’s just no way to climb out of the hole. Like there’s just nothing that’s going to get them out. This attitude, that I’ve seen, over 60 years, I’ve never seen anything like it. It scares me.

TOM ASHBROOK: Up against it. And with an education, a particular education. Don, thank you for your call.

The financiers and speculators need to be stopped at some point. Either we start now, or we will be forced to do so when the damage already done is much greater and the stakes are even higher.