Prof. James Hamilton of Econbrowser notes that:

The curious thing is that [stock and commodity] graphs [for the last month] all look the same. Which suggests ... that recent market moves have a common driving factor.

The natural explanation would seem to be that markets have interpreted developments over the last month as bad news in terms of the quantities of basic raw materials that global customers will want to buy and in terms of the profits that companies around the world can expect to earn.

Such concerns would have to come not just from the fact that the European countries forced into budget austerity measures are going to be buying less... [but] a potential replay of the credit crunch that brought the world economy crashing down in the fall of 2008.

In short, markets are anticipating another deflationary bust. Will this push the US back into recession? That is what I discuss below.

Introduction. This diary is designed to give you a working understanding of the following two subjects:

(1) What is at issue in Europe?

(2) What are the effects of Europe's problem (including effects specific to the US)?

What is at issue in Europe is really the problem of Greece, Spain, Portugal, and Italy. All of these countries are part of the single european currency, the Euro, but never really met the official fiscal rules for entry -- their deficits were persistently too high. This problem was exacerbated as, during the good times, European governing authorities looked the other way while even big countries like France ran deficits that supposedly called for sanctions. Now, in bad times, the bill is coming due, and the typical way of dealing with the debt problems -- devaluing your currency in order to pay back your debt with cheaper paper, and to increase your exports -- is not available to them, because they are tied in a fiscal union to countries like Germany.

But keep in mind that the 4 Mediterranean countries at the epicenter of the problems are not aomng the biggest economies in Europe. They could leave the Euro and life would go on. Europe could bail them out, issuing more debt, but countries like Germany are able to handle that. Or they could insist on austerity, which only exacerbates the problems in times of deflation (a la the Great Depression). Signs are the Europe is insisting on a combination of the last two items, and has resolutely taken "leaving the Euro" off the table.

The effects of Europe's problems are primarily concerns about loss of demand. If I make money from selling you products, and you buy less of my products, I suffer too. The concern is that Europe's problems, and their demand for austerity as part of the solution, will cause demand for goods and services in southern Europe to collapse. This will hit the economies of the rest of Europe the most, causing a loss of demand there as well. And from there the downturn in demand continues to ripple outward.

Secondarily, if I make my profits partly in your currency, and your currency is devalued relative to mine, then when I "repatriate" my profits to my own country, in my currency I have made less profit. The further away from the epicenter I am, however, the less the effects on me are.

The United States is, among the industrialized countries, the furthest from the epicenter, in part because there are collateral but contrary benefits to us from Eurozone distress. If my currency is the "safe haven" then my interest rates go down, allowing me to borrow (for things like mortgages and cars) at a lower rate. Also, if the prices I have to pay go down (deflation), but my economy is otherwise growing, I am able to buy more stuff than I otherwise could. So, the issue for the US is whether the benefits outweigh the risks.

Now let's take a look at the above issues in more detail.

I. Loss of demand

Here is a graph of various commodity indexes for the last year:

Notice how all the squiggles are generally going up - until a month ago. That is because the global economy was expanding, and at a rapid pace too. More natural resources were needed for production, so their prices went up. In the last month, they've all gone back down sharply. That's because the markets believe that demand will go down. Prof. Hamilton's article above includes graphs of copper and aluminum as well as oil, and they all look the same.

Notice secondly what a decline in the prices of raw materials means -- deflation. More on that below.

II. Loss of profits

Large US companies make a significant share of their profits in Europe. In addition to European demand for those products going down, the 10%+ decline in the value of the Euro vs. the Dollar in just the last month means that profits made in Euros become 10% lower profits when recorded on balance sheets in the US. Thus corporate profits are expected to go down, and that is what the following graph of the S&P 500 for the last 6 months tells us:

III. The Issue of Deflation

Back in January, in 2010: Gilded Recovery, or Double Dip? (and Oil) I sketched out 2 scenarios, one for each for the two halves of this year. Based on the Leading Economic Indicators which were still strongly positive, I said

The simple fact is, the first 3-6 months of 2010 are probably going to show growth, and indeed more strong growth than few dared to hope for in 2009.

So it seems, as in the first quarter we saw ~3% growth, and the second quarter looks to be positive as well.

As to the second half, I said:

There is ... one economic indicator with an excellent track record at forecasting the economy - with one important qualifier - a year out. That is the yield curve of the bond market.

So long as there is inflation, not deflation, a positive sloping yield curve, where long term interest rates are higher than short term rates, has correctly predicted economic expansion 1 year later, without exception, since 1920, including the Great Depression.

Since long term interest rates, at ~3.5% to 4%, are higher than short term rates, which are close to zero, we still have a positively sloping yield curve as we had at the beginning of this year.

But ... the combined stock and bond markets smell deflation. To show you what I mean, in the following three graphs, the price of the S&P 500 stock index is plotted in red and the 10 year US Treasury bond yield in blue.

The first graph covers the period 1982-1997. Notice that bond yields and stock prices form mirror images of one another. As stock prices go up, bond yields go down, and visa versa:

A decline in bond yields was, on balance, good, as it meant cheaper credit, whereas higher bond yields meant more inflation and the possibility of the central bank tightening credit.

The next graph covers the period from 1998 when the Asian currency crisis hit, to 2003 when the post dot-com recovery finally got going:

Notice that during this time, bond yields and stock prices moved in the same direction. This signaled that bonds were primarily being used as a "flight to safety" and moreso that lwer, but necessarily positive bond yields weren't enough to prevent economic meltdown. In other words, the bond market was primarily concerned about DEflation rather than inflation.

Now here is the same series from 2003 to the present:

Notice that there are 4 distinct periods:

- First, from 2003 to mid 2007, during the Bushco expansion, bond yields and stock prices once again generally moved as mirror images of one another. The bond market did not fear deflaton.

- The second period is mid 2007 to mid 2009. This is the period of the Great Recession, which was the first full fledged deflationary bust since the 1930s.

- The third period is the second half of 2009, during which bonds and stocks briefly resumed their mirror image period.

- Finally, since December of last year, roughly equivalent with the Dubai solvency crisis, bonds have once again resumed primary status as a safe haven, and are moving in tandem with stocks.

In short, for the last 6 months, the bond market has again primarily feared a resumption of deflation.

Noting the (-0.1%) CPI report Wednesday, Prof. Krugman is also concerned the deflation is being signaled.

Another negative is that the Leading Indicators were reported surprisingly if slightly down yesterday, by (-0.1). Given the stock market meltdown this month, a negative LEI for May looks quite likely as well, which certainly signals weakness, if not full reversal, around about Labor Day.

IV. The Counterbalancing benefits: lower prices and interest rates

Deflation isn't always bad. If deflation occurs during an economic upturn, and wages grow rather than join prices in a vicious spiral downward, deflation can be good. Indeed, during the last decade, there have been 5 incidents of deflation longer than one month: late 2001, early 2003, late 2005, late 2006, and a very serious bout of deflation in the second half of 2008. The first four were not long or deep enough to show up as a serious impact on the economy. Only the fifth was a full-fledged deflationary bust.

In my above forecast for 2010, I called Oil the "Joker in the Deck" as to whether there would be deflation, saying:

if consumers once again have to pay over $3 a gallon for gas (which ~$90 Oil would give us), it will have a psychological as well as economic impact on consumers, and I would expect them to cut back in other areas. ... It seems [ ] likely that Oil prices will continue to increase, but slowly this time as opposed to the skyrocketing speculative blowoff that led to $147 Oil in July 2008.

Whether $90+ Oil will lead to a full-blown double-dip economic contraction, or just a slowdown later in the year, is almost impossible to gauge. It depends upon how far over $90 Oil shoots, and how long it stays there. If there is a dramatic overshooting a la 2007, there will be a double-dip. If there is a gradual increase over $90 that does not last that long before consumers cut back and the feedback loop causes price declines, then there may just be a slowdown, or if there is a contraction, it may be shallow and only last a quarter or two -- which is my best guess, and only a guess, at this point.

Here's the graph showing Oil prices from their December 2008 bottom to the present:

What has happened is exactly that "gradual increase" which wound up stopping about $2 short of the $90 breaking point described above. Note that even the past month's $20+ decline in the price of Oil does not look so drastic in this larger time frame. In other words, more consistent with slowdown or shallow decline than full-fledged "double-dip."

So the price of an essential US consumer commodity is going down, retreating strongly from the level (equivalent to 6% of disposable consumer income) which in the past 40 years was the triggering point for a recession.

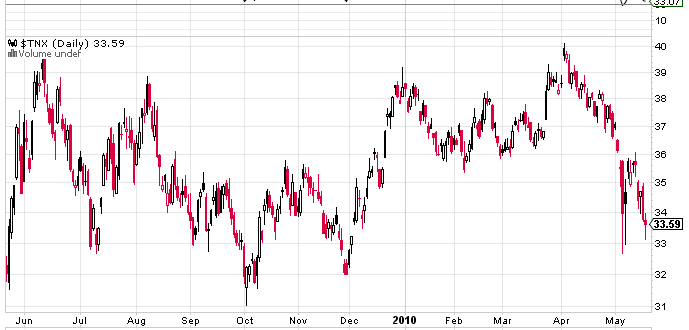

Additionally, here's a close up graph of yields on the 10 year treasury bond for the last year:

The crisis in Europe which has caused investors to flee to US bonds, has caused interest rates of the benchmark 10 year US Treasury bond -- the one used generally to calculate mortgage rates -- to decrase all the way from 4% to 3.13%(!) yesterday. In other words, the cost of refinancing consumer debt just went back down.

Just a few days ago, calling Income Stagnation the greatest threat to the recovery, I said that for sustainability, we needed to see lower interest rates (to aid and abet debt refinancing) and/or inflation under 1.5%. The Euro meltdown may give us both of those things.

V. Most analysts believe the benefits of lower prices and interest rates will prevent the US from sliding back into a "double-dip"recession

So far, none of the econometric forecasting services that foresaw the recovery late last year believe that the European problem is sufficient to drive the US back into a double-dip recession, although they believe a slowdown in growth is likely.

For example the Federal Reserve Bank of San Francisco accurately forecast the shape and strength of the recovery to date back in August. Here's the projection of their "Laubach and Williams" (LW) model for the rest of the year:

The model calls for nearly 4% YoY GDP growth, which is quite strong.

Similarly, the Economic Cycle Research Institute (ECRI) which distinguished itself during mid freefall in March of last year by accurately calling for the recession to bottom in summertime, says that "there is little risk of renewed recession this year," although the pace of improvement in the overall economy is set to slacken in the months ahead," according to its managing director, Lakshman Achuthan.

One persuasive analyist has gone even further. University of Oregon economics professor Tim Duy has described, in this post at Economist's View, which I encourage you to click through to and spend a few minutes reading in full, that the European problems may wind up being a net positive for the US economy:

I think it unlikely that an export demand shock alone is sufficient to push the US economy back into recession. Menzie Chinn tackled this issue back in 2007, arguing at the time it was unlikely a rise in exports would stave off a recession. The reverse logic holds as well; US recessions look to be driven by sharp declines in domestic absorption, not exports....

one would have to consider the positive impact of the Greek crisis against any trade drag. And yes, there are positive implications. First, the weaker Euro has taken a bite out of oil prices, which fell back below $70 today. Make no mistake - keeping a lid on oil prices offers continued support for US consumers. And while we can all dream of a more balanced economy less dependent on household spending, for now it remains the best game in town. ...the overall trend in retail sales continue to look solid:

Consumers have a wind at their backs, unbelievably, and further job growth will only speed them further. Likewise, the rush to Treasuries is keeping a lid on US interest rates....

Bottom Line: The European crisis, by keeping US interest rates in check and oil prices low, may do more to help the US recovery than hurt it

Paul Krugman agrees:

Many of us have noticed that the US exports only a bit more than 1 percent of GDP to the euro zone, limiting the direct negative impact. Meanwhile, as Duy points out, the immediate impact of the euro crisis has been (a) a fall in oil prices (b) a fall in long-term interest rates. Both of these are actually positive for the US.

Against that you might set fear of financial disruption, which may drive up borrowing costs for some private sector players. But Duy is right: it’s not at all clear that this hurts prospects for growth over the next few quarters.

And just this morning, Menzie Chinn, Professor of Public Affairs and Economics at the University of Wisconsin, Madison, notes that:

The OECD has recently released documentation on their new macroeconometric model. One of the experiments implemented involves a 10% euro depreciation against a basket of currencies

....

the [study] indicates the effect of a 10% euro depreciation would only have a modest impact on US GDP -- a 0.2 percentage point deviation relative to baseline two years out, if sustained.

Prof. Chinn suggests that it would take a September 2008 syle total credit freeze for this model to be seriously off the mark.

Conclusion

It is worthwhile to note that in the 2008 recession, the US was the epicenter of the crash. No other region took so big a hit to GDP or employment. In fact, most of Asia kept right on growing. If Europe gets hit now, Asia will be one step removed, and as Krugman points out, the US will be even more on the periphery than that.

The question is, which will be affected more by a Euro meltdown: the manufacturing and exports that have helped drive the US recovery so far (bad), or interest rates and the price of Oil and other commodities (good)? Nobody knows for sure, in part because nobody can gauge the trade-offs I've described above with any real precision; and also because some of the decisive factors are going to be how adept - or maladept - the political response is in Europe. In my opinion, the panic-mongering of Bush, Bernanke, and Barney Frank among others, needlessly and stupidly caused consumers to "freeze" at the time of the September 2008 Wall Street bailout. Similarly, German Chancellor Angela Merkel's blunt declaration that the Euro was in danger the other day may well have had a similar effect on the markets.

Still, for now my best guess is that Profs. Duy and Krugman are right, and we sustain only a slowdown in the rate of recovery, but not a double-dip. Time will tell, and anybody who tells you they know for sure is lying to you.