The Economics:

James K. Galbraith: In Defense of Deficits

... a big deficit-reduction program would destroy the economy, or what remains of it, two years into the Great Crisis.

For this reason, the deficit phobia of Wall Street, the press, some economists and practically all politicians is one of the deepest dangers that we face. It's not just the old and the sick who are threatened; we all are. To cut current deficits without first rebuilding the economic engine of the private credit system is a sure path to stagnation, to a double-dip recession--even to a second Great Depression. To focus obsessively on cutting future deficits is also a path that will obstruct, not assist, what we need to do to re-establish strong growth and high employment.

L. Randall Wray: “Teaching the Fallacy of Composition: The Federal Budget Deficit”

We hear politicians and the media arguing that the current federal budget deficit is unsustainable. I have heard numerous politicians refer to their own household situation: if my household continually spent more than its income year after year, it would go bankrupt. Hence, the federal government is on a path to insolvency, and by implication, the budget deficit is bankrupting the nation.

That is another type of fallacy of composition. It ignores the impact that the budget deficit has on other sectors of the economy. Let me go through this in some detail, as it is more complicated than the other examples.

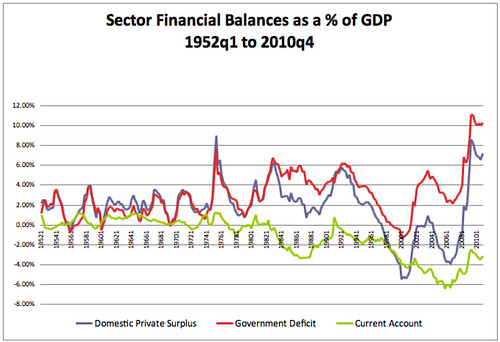

We can divide the economy into 3 sectors. Let’s keep this as simple as possible: there is a private sector that includes both households and firms. There is a government sector that includes both the federal government as well as all levels of state and local governments. And there is a foreign sector that includes imports and exports; (in the simplest model, we can summarize that as net exports—the difference between imports and exports—although to be entirely accurate, we use the current account balance as the measure of the impact of the foreign sector on the balance of income and spending).

At the aggregate level, the dollar spending of all three sectors combined must equal the income received by the three sectors combined. Aggregate spending equals aggregate income. But there is no reason why any one sector must spend an amount exactly equal to its income. One sector can run a surplus (spend less than its income) so long as another runs a deficit (spends more than its income).

Historically the US private sector spends less than its income—that is it runs a surplus. Another way of saying that is that the private sector saves. In the past, on average the private sector spent about 97 cents for every dollar of income.

Historically, the US on average ran a balanced current account—our imports were just about equal to our exports. (As discussed below, that has changed in recent years, so that today the US runs a huge current account deficit.)

Now, if the foreign sector is balanced and the private sector runs a surplus, this means by identity that the government sector runs a deficit. And, in fact, historically the government sector taken as a whole averaged a deficit: it spent about $1.03 for every dollar of national income.

Note that that budget deficit exactly offsets the private sector’s surplus—which was about 3 cents of every dollar of income. In fact, if we have a balanced foreign sector, there is no way for the private sector as a whole to save unless the government runs a deficit. Without a government deficit, there would be no private saving. Sure, one individual can spend less than her income, but another would have to spend more than his income.

While it is commonly believed that continual budget deficits will bankrupt the nation, in reality, those budget deficits are the only way that our private sector can save and accumulate net financial wealth.

Scott Fulwiller (via email):

L. Randall Wray: The Perfect Fiscal Storm: Causes, Consequences, Solutions

During the Clinton years as the government budget moved to surplus, it was the private sector’s deficit that was the mirror image to the budget surplus plus the current account deficit. This mirror image is what the Wall Street Journal had failed to recognize—and what almost no one except MMT-ers and the Levy Economic Institute’s researchers understand. After the financial collapse, the domestic private sector moved sharply to a large surplus (which is what it normally does in recession), the current account deficit fell (as consumers bought fewer imports), and the budget deficit grew mostly because tax revenue collapsed as domestic sales and employment fell.

Unfortunately, just as policymakers learned the wrong lessons from the Clinton administration budget surpluses—thinking that the federal budget surpluses were great while they actually were just the flip side to the private sector’s deficit spending—they are now learning the wrong lessons from this crash. They’ve managed to convince themselves that it is all caused by government sector profligacy.

The Politics:

James K. Galbraith: Why Progressives Shouldn't Fall For the Deficit Reduction Trap

The fetish of long-term deficit reduction is politically poisonous -- and economically pointless. In reality, we need big budget deficits. We need them now -- and down the road.

... once you concede that deficits are actually bad, you're boxed in. If you exclude Social Security and Medicare, there is no way to cut deficits seriously (short- or long-term, on unchanged economic assumptions) except by slashing the Pentagon or by raising taxes. If you had to do something, I agree, those would be better moves. But good luck. It's not a political battle one can win.

In reality, we need big budget deficits. We need them now. We need bigger deficits than we've got, to stabilize state and local governments and to provide jobs and payroll tax relief. And we may need them for a long time, on an increasing scale, and in the service of a sustained investment strategy aimed at solving our jobs, energy, environment and climate change problems. To pretend that expansionary policies are needed only for now, gives all this away.

The public deficit is just the obverse of net private savings. That is, when private credit is booming, investment exceeds saving and deficits tend to disappear. That's what happened in the 1990s. When credit collapses, deficits return. That's what's happening now. Large long-term deficits will occur, or not, depending only on whether we succeed in generating a new growth cycle, financed by the expansion of private credit. Policies to cut spending or raise taxes -- now or for that matter in the future -- contribute nothing to this goal.

Financial reform and debt relief are therefore the only paths to public deficit reduction.; It would be nice to have them, for the economy works better and people are happier when they can borrow and invest privately. But if we don't get them, the alternative isn't a "return to fiscal responsibility." It's a choice between large public budget deficits that fund important and useful activities and tax relief, or large deficits because the recession, housing slump and high unemployment drag on and on, all made worse by cuts in Social Security, Medicare and other public spending.

Yes, we must defend Social Security and Medicare from Wall Street and its political agents -- which now, sadly, include the Obama White House. But we'll lose on that -- and everything else -- if we start by giving up the fight for an aggressive, effective, sustained and long-range economic recovery program, deficits and all.

The Banksters and You:

James K. Galbraith: In Defense of Deficits

To put things crudely, there are two ways to get the increase in total spending that we call "economic growth." One way is for government to spend. The other is for banks to lend. Leaving aside short-term adjustments like increased net exports or financial innovation, that's basically all there is. Governments and banks are the two entities with the power to create something from nothing. If total spending power is to grow, one or the other of these two great financial motors--public deficits or private loans--has to be in action.

For ordinary people, public budget deficits, despite their bad reputation, are much better than private loans. Deficits put money in private pockets. Private households get more cash. They own that cash free and clear, and they can spend it as they like. If they wish, they can also convert it into interest-earning government bonds or they can repay their debts. This is called an increase in "net financial wealth." Ordinary people benefit, but there is nothing in it for banks.

And this, in the simplest terms, explains the deficit phobia of Wall Street, the corporate media and the right-wing economists. Bankers don't like budget deficits because they compete with bank loans as a source of growth. When a bank makes a loan, cash balances in private hands also go up. But now the cash is not owned free and clear. There is a contractual obligation to pay interest and to repay principal. If the enterprise defaults, there may be an asset left over--a house or factory or company--that will then become the property of the bank. It's easy to see why bankers love private credit but hate public deficits.

All of this should be painfully obvious, but it is deeply obscure. It is obscure because legions of Wall Streeters--led notably in our time by Peter Peterson and his front man, former comptroller general David Walker, and including the Robert Rubin wing of the Democratic Party and numerous "bipartisan" enterprises like the Concord Coalition and the Committee for a Responsible Federal Budget--have labored mightily to confuse the issues.

*******

“In all life one should comfort the afflicted, but verily, also, one should afflict the comfortable, and especially when they are comfortably, contentedly, even happily wrong.”

John Kenneth Galbraith

*******

Further Reading:

Bill Mitchell, Stephanie Kelton, Warren Mosler, Marshall Auerback, L. Randall Wray, Pavlina Tcherneva: Fiscal Sustainability Teach-In and Counter-Conference

Lynn Parramore and new deal 2.0: The Deficit: Nine Myths We Can’t Afford

Warren Mosler:

Seven Deadly Frauds of Economic Policy

William Mitchell:

Barnaby, better to walk before we run

Stock-flow consistent macro models

Deficit spending 101 – Part 1

Deficit spending 101 – Part 2

Deficit spending 101 – Part 3

L. Randall Wray:

Understanding Modern Money: The Key to Full Employment and Price Stability

James K. Galbraith:

The Predator State: How Conservatives Abandoned the Free Market and Why Liberals Should Too

********

NOTES:

1. The extended quotes are used with the kind permission of the authors, James K. Galbraith and L. Randall Wray. The graph is used with the kind permission of Scott Fullwiler.

2. x-posted from my blog