Wherein I make a simple comparison of the average Medicare financial benefits received in 2010 by Medicare recipients vs. what they would have received if Paul Ryan's "Dont Say I'm Killing Medicare Even though I am Killing Medicare" plan had been in effect last year, all using 2010 US dollars.

It's not the end-all, be-all of comparisons between "Medicare as We Know It" and "Ryan's Not-Medicare Voucher Plan" but it has the benefit of giving you a single figure, call it a rough estimate, if you will, of what the average person would get in dollars and cents under Medicare as We Know It and what that average person would receive in dollars and cents under Ryan's Not-Medicare Voucher Plan.

(Spoiler: You would get $5000-7000 less in average financial payments for your healthcare costs from the government under Ryan's plan, at a minimum).

(cont.)

But before the Math let's look at what Medicare provides to recipients and what The Ryan Plan would provide.

We all know that Rep. Pail Ryan's proposal for Medicare would end the current program for everyone 55 and younger. Instead of being enrolled in Medicare at age 65 (or 67 if the Ryan plan is ever accepted), each individual would be provided a "single premium support payment" or as they are more commonly referred to by most people as vouchers. In effect, future beneficiaries under the "Ryan Plan" would not receive the current basket of Medicare benefits that my parents, for example, receive.

Current Medicare Benefits:

You can find a summary of Medicare's hospitalization and insurance benefits (Medicare Part A and Part B) at this webpage (LINK) if you are interested. Benefits under Medicare Part D for prescription drug coverage are summarized at this webpage (LINK). These are the basic benefits provided. Obviously costs may vary depending on whether you opt for basic Medicare or a Medicare HMO or PPO care plan.

The best benefit Medicare provides however is not strictly financial. Medicare provides coverage to everyone enrolled in the program for any medical issue, including any pre-existing conditions. As many of us who are slouching toward age 65 know, the older you get, the more likely you are to have various chronic and other health conditions that pop up. For example, just looking at the "A's" on our list of pre-existing conditions you could have arthritis, Alzheimer's disease, AIDS, and so forth. And let's not even talk about those illnesses/conditions in the "C" category (though I think you know the one I'm talking about).

The Ryan Plan:

The Ryan Plan gets rid of all those confusing alphabet soup parts of Medicare. Instead, it gives you a check every year from the Federal Government with which you, the people formerly eligible for Medicare, will be able to use to pay for your health care costs, including the purchase of any health insurance policies that the private market might be willing to sell to people over the age of 65 (and ultimately over the age of 67). You get the check, you decide how to pay for it, you make the decisions on what coverage you can afford or for which you are willing to pay.

Sounds great, right. Freedom! Liberty! Pay for the health care you need, not for what other people might need.

One big caveat though. The Ryan Plan of Not-Medicare doesn't require that private insurers cover the cost of any re-existing conditions you might have. Hey, if you have no pre-existing conditions what's your worry? On the other hand ...

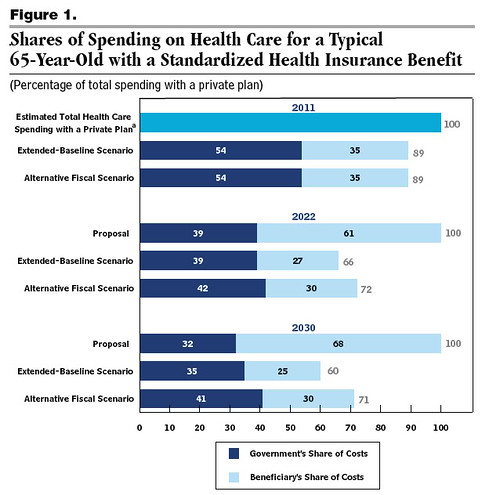

Unlike the Affordable Care Act, which mandated that millions of young and healthy Americans purchase insurance with government subsidies, the Paul Ryan plan would instead bring the oldest, sickest, and least profitable demographic to the table. And with the CBO projecting that the average senior would be on the hook for over two-thirds of their health care costs within just 10 years of the plan's adoption -- a proportion that is projected to worsen in the long run --- the government subsidies backing them up may not bring in enough profitable customers to make things worthwhile.

"If reimbursement rates are too low to provide basic benefits, they'll tell the government, 'You do it,'" one insurance lobbyist told TPM. "I don't think they can require they lose money, they'd just pull out."

Dan Boston, a veteran lobbyist for health care providers and co-owner of Health Policy Source, said in an interview with TPM that he was taking a "wait and see" approach on the GOP budget before judging its value. (The American Hospital Association opposes the plan). But he cautioned that a major concern would be whether hospitals and private insurers would be left on the hook for low-income seniors eligible for both Medicare and Medicaid, who could run up significant costs with little hope of ever paying them off.

So, Ryan's Not Medicare Plan might make it very difficult for seniors to even qualify for health insurance, period. Why? Because the insurance companies may simply not deem it worth their while to participate. Just as an example did you know that in 2006 health insurance companies denied coverage to 29% of all uninsured individuals seeking health insurance? It's true.

Because medical problems tend to increase with age, older adults are

more likely than their younger counterparts to be denied coverage after applying for health insurance in the non-group market. Denial rates were three-times greater for

those ages 60 to 64 than for those ages 35-39 (29 percent vs 10 percent, respectively) (Figure 13). Those who were offered coverage may have had to pay for certain services and treatments out-of-pocket because non-group plans often exclude

treatment for pre-existing conditions through an elimination rider. In 2006, about 10 percent of policies offered to adults ages 55 to 64 included such a rider.

So, let that linger in the back of your mind if you are someone who thinks the free market can solve all our health care cost issues.

The MATH:

But now for the big finale I promised all along (sorry to make you wait). How much in terms of financial assistance (i.e., money) does Medicare as We Know It provide people versus what Ryan's Not-Medicare Plan will pay you.

First we need to control for inflation, so we must adjust the cost by using figures that are adjusted to represent the present value of actual dollars received I chose the year 2010.

Under Medicare as we Know It:

Under Medicare last year, around $528 Billion dollars was spent on the program:

According to the CBO, gross spending on the Medicare program is expected to total $528 billion in 2010 ...

Now in 2010, there were 46,589,141 people who received benefits under Medicare.

So you take $528,000,000,000 (gross spending) and divide that by 46,589,141 (no. of beneficiaries) and you get the an average number of dollars spent per beneficiary. And that number is (damn where's calculator -- oh here it is):

$11,333.11 per Medicare Beneficiary

Just to make things simple lets round that number down to $11,000. That's how much each beneficiary, on average, cost Medicare, or in other words, how much financial benefit Medicare beneficiaries received.

Under the Ryan Not-Medicare Plan:

Oddly enough, Rep. Ryan's Not-Medicare Plan offers a voucher of about that size when the Ryan Not-Medicare Plan goes into effect in 2021. So, sounds like a wash right? Well, not exactly.

You see we still have to adjust for inflation if we are going to accurately compare what Medicare provides to what Ryan's Not-Medicare Plan proposes to provide ten years from now. Fortunately, the Congressional Budget Office has already made that adjustment for us. Here's what they had to say about Ryan's Not-Medicare Voucher Plan and what it would provide beneficiaries in terms of dollars:

In 2021, when enrollees would first receive the voucher, the average voucher for 65-year-olds would be worth $5,900 (in 2010 dollars), as specified by your staff.

The CBO (via Vyan) actually comes up with a a number higher than mine: $7,000:

Now remember, everyone who turns 65 before 2021 gets Medicare as We Know it. But those poor bastards like me (I turn 65 in 2021) would get a voucher for $5,900. I wouldn't get automatic health care coverage, I'd have to find someone willing to sell me a health insurance policy for that amount of money. Since I have a number of pre-existing conditions, I suspect that might be a bit difficult. Indeed, I suspect that I'd either get a policy with a huge deductible and riders excluding coverage for my pre-existing conditions or nothing at all.

In addition, any Medicare benefits beneficiaries currently receive are not taxable. But under the Ryan Not-Medicare Plan, it's not clear how my "voucher" payment for health care would be viewed since the Ryan Plan eliminates the exclusion for medical insurance benefits paid by third parties. Instead ...

In 2011, the current tax exclusion for employment-based health insurance would be replaced by a refundable tax credit for the purchase of health insurance, either through an employer or on an individual basis. The tax credit initially would be set at $2,300 per adult ...

That's a tax credit of $2,300 in 2021 dollars, by the way. In 2010 dollars that tax credit would be worth a lot less, roughly between 1,200-$1,400 at best. So instead of tax free benefits, under Medicare, I would have be pay taxes on the difference between the Ryan voucher of $5,900 and whatever the tax credit is worth.

Conclusion:

In any event, the simple fact is that at age 65 under the Ryan Not-Medicare Plan I would receive, at a minimum, a voucher that on average is worth $5,100 less than the average benefits I would receive under Medicare as We Know It (in my case with all my medical issues, the dollar amount of benefits I would lose under the Ryan Plan likely would be diminished by a far greater amount).

I would also receive much less healthcare coverage under any insurance policy I could buy, assuming any insurance company would be willing to sell me a policy that was worth more than the paper it was printed on.

The CBO predicts that under the Ryan Not-Medicare Plan I would likely have to pay for 2/3 the cost of my medical care. Ask yourself this question: Do you think you will be able to afford to pay 2/3 the cost of your health care when you turn 65? I know I won't.

Medicare as We Know It currently pays approximately 70% of all beneficiaries' health care costs.

Sebelius said the federal government currently covers 70 percent of the cost of Medicare. CBO estimates the government's share of Medicare costs, under the Republican plan, would be reduced to 39 percent in 2022 and 32 percent by 2030, with seniors footing the remainder of the bill.

The Ryan Not-Medicare plan would essentially flip that percentage, forcing the the elderly and their families to pay roughly 70% of their health care costs. I know that if I have to pay 70% of my health care costs after the age of 65 I will run out of my savings very quickly. And then, when I am bankrupt and can no longer afford medical care I (and you, too) would die much sooner than I would if Ryan's "brave" Not-Medicare Plan ever passes into law.

And that's the real math of the Ryan Not-Medicare Plan.