As I pointed out in a a previous diary, the social security surplus is effective a loan from working class people to wealthy people. Lets talk about that again in more detail because some interesting observations immediately jump out.

Ok, social security as a loan from the working class to the wealthy - here it goes:

Suppose social security does not exist and the government funds itself solely on income taxes with a balanced budget. One years federal spending of $2T is matched with $2T of income tax. Easy enough.

Now, add in the social security trust fund as a separate entity. It runs a surplus of $100B. It can't put the cash in a vault, so it shoots it over to the federal budget in the form of a bond purchase. So, social security surplus equals extra money in the federal budget (+ debt). Easy enough.

Now here is a problem. The federal budget has an extra $100B. It also cannot put the cash in a vault,... so,... that means: TAX CUT!

So, $100B social security suplus = $100B tax cut. Whoo-hoo!!!!

Ok, but now the federal government has an outstanding debt. Suppose that 3 years later the social security trust is $100B in the hole. It calls in the loan to the federal government, which must scrounge up the cash through income taxes. So..., that means: TAX INCREASE!

So, $100B social security deficit = $100B tax increase. Dohhh!!!!

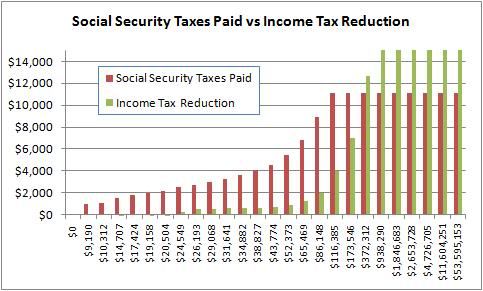

Now here is the tricky part: social security taxes are not collected at the same rates that income taxes are collected. Side by side income tax rate and social security tax rates look like this:

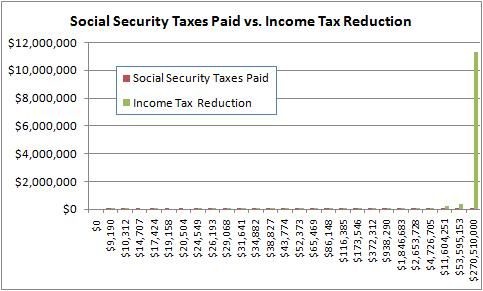

Fully zoomed out, the difference is much more awesome-scary:

Of course, those charts compare individual takes. Since there aren't the same number of people in each income group, the dollar totals look like this:

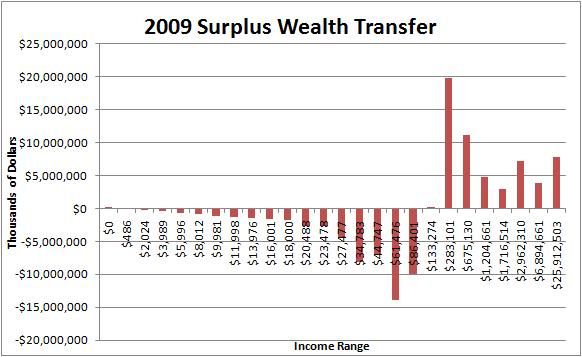

When social security is in surplus, money flow from the left side of the chart to the right side of the chart. When social security is in deficit, money flows from the right side of the chart to the left side of the chart. After all, it is only a loan if it is ever called back. Otherwise it is a give-away.

Now, lets muck it up a bit. First, income taxes are only about 2/3 of federal income, so technically we are playing the same game with corporate taxes and other sources of federal income. Second, the loans do carry interest, so if it is never called back it is still transferring money from the right side of the chart to the left side of the chart via interest payment. Finally, the federal government can run in deficit beyond the trust fund, but for these purposes that is only kicking the can down the road, it doesn't change anything.

Now, lets make some observations:

1) The ONLY way to recall the loan is to raise income taxes and allow social security to run in the red (i.e. burn down the surplus). No new taxes = keep my $2.6T!!!!!

1.5) Even worse, 'fixing' social security by increasing inflows = keep my $2.6T and here is more!!!!!

2) Social security interest rates are currently under 3%. Raising that rate = instant solvency. Raise it too high and wealthy people could rightly claim they are being loan-sharked. But, 3%%%% Come-on!!!!

3) Technically, social security is privatized: the surplus is distributed to wealthy people at a 3% interest rate. They are allowed to keep anything they can generate above 3% with the distributed funds. Sucks to be them, or boy are they stupid for trying to close this spiggot.

4) Social security surplus = federal debt. No deficit spending = no increase in trust fund balance. Go figure how/why old people are supporting that one or how anyone can claim they are improving trust fund solvency while closing the deficit.

5) Beware the bait-and-switch. There is currently $2.6T in the trust fund. Dissolving it and distributing it to its contributors requires $2.6T in income taxes. Beware the "How about $2.6T of these nice cds-backed-butterfly-sweeps!"

I was going to post the spreadsheet. It is online as a google doc, but I'm out of time for tonight.