Here’s something interesting.

Steve Keen is an economist at the University of Western Sydney in Australia, and is an expert in Hyman Minsky’s “Financial Instability Hypothesis.” The Financial Instability Hypothesis “emphasizes the importance of private debt in the economy – something that is ignored by the dominant ‘neoclassical’ school of economics” and posits that the accumulation of large amounts of private debt can push economies into financial crises and recessions just like the one we are so enjoying today. Keen’s knowledge of Minksy’s work helped him to predict as early as 2005 that a devastating financial crisis was set to wreak havoc with the world.

If Keen’s analysis of how this crisis came to be is correct, then it also points to perhaps the only truly practical solution for ending the crisis and getting our economy back on a solid footing: a massive amount of debt forgiveness for the private sector and the forced bankruptcy of most of the financial industry.

The Minsky-Keen Trap

Essentially, Keen argues that (i) once private debt represents a "significant fraction" of a nation’s GDP and (ii) the private debt’s growth rate substantially exceeds that of GDP, then private debt must continue growing faster than GDP just to avoid a recession. It is a type of Red Queen’s Race in which “it takes all the running you can do, to keep in the same place.”

To illustrate his argument, Keen provides the following extremely simplified example:

Year One

(For purposes of this example, all dollar amounts are denominated in billions).

Suppose you’ve got an economy that – for Year 1 – will have total output (GDP) of $1,000 and a nominal GDP growth rate of 10%. (Half of the GDP growth rate is attributable to growth in real output, and half is attributable to a 5% rate of inflation.) The economy also begins Year 1 with an aggregate private debt level of $1,250, and that debt level grows at 20%, i.e., twice as fast as the nominal GDP growth rate.

Now what all this means is that during our initial year, the economy’s aggregate demand – the total amount spent - will be $1,250. $1,000 of that demand will have been financed by income (GDP) and $250 will have been financed by an increase in private debt.

So far, so good.

Year Two

In Year 2, we have the following: an economy that will have a GDP of $1,100 ($1,000 x 1.10), and begins the year with an aggregate private debt level of $1,500 ($1,250 x 1.20). Now then . . .

Scenario A - Suppose the amount of private debt levels off in Year Two and,

for whatever reason, no one in the private sector borrows any

more money.

This means that in Year 2, you will have aggregate demand –

the total amount spent -- of only $1,100, which consists

entirely and only of Year 2’s GDP (because no new debt has

been incurred). But this is $150 less than what was spent in

the previous year. Stated another way, if the growth rate of

private sector debt is suddenly cut to zero then the economy

experiences a 12% fall off in aggregate demand, with all the

recessionary consequences one might expect.

Scenario B - Suppose, instead of zeroing out, private debt grows only as

much as does GDP. Now total demand for Year 2 will be $1,250

– the same as in Year 1. This total demand consists of $1,100

GDP, and $150 of increased debt. So there is no growth in the

economy, but it doesn’t shrink either; it just remains flat.

Ordinarily, we don’t think of a flat-lining economy as particularly

good. But it gets worse. As Keen points out, we need to

remember that some portion of nominal GDP growth consists of

nothing more than inflation; in this example, inflation accounts

for ½ of all GDP growth. Taking inflation into account, we find

that even if private debt growth slows only until it matches that

of GDP, real aggregate demand still actually contracts.

Simply stated, even slowing down the private debt growth rate can plunge an economy into recession.

It’s important to note that, for an economy caught in what I am now going to call the Minsky-Keen trap, the proximate cause of an economic contraction is not the mere existence of a large amount of private debt. Instead, it is the failure of that large amount of debt to continue growing at least as fast as it had previously.

The problem, of course, is that aggregate private sector debt cannot grow faster than GDP indefinitely. Which means that it is simply inevitable that at some point the private sector will no longer be able to take on debt as quickly as before; when that happens, the private sector begins to deleverage, i.e. to reduce its debt load. This lack of debt-financed spending reduces aggregate demand and, in turn, plunges us straight into an economic recession -- a recession in which we will remain mired until our private debt overhang has been reduced to the point that private sector resources can once again be put to productive use.

How’s America Doing With All This?

If Keen’s analysis is correct, we’re caught in the trap.

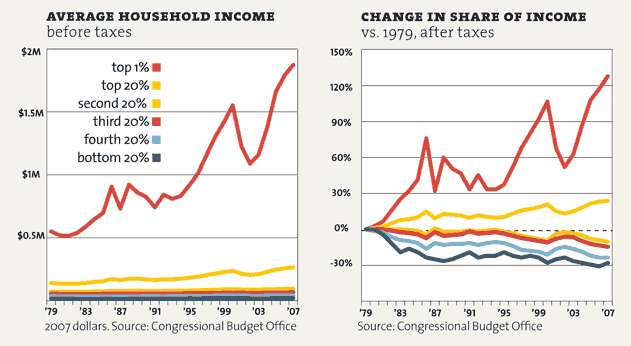

As I’ve mentioned before, the source of the gaping chasm that now exists between most Americans and the uber-wealthy traces back to only 30-odd years ago. Beginning in the mid- to late-70s, all but the top 20% of Americans saw their wages stagnate or decline relative to GDP, while all of America’s increasing productivity was funneled instead to the top 20% and – especially – to the top 1% of the country.

(h/t Mother Jones)

But “some substitute for actual income had to be provided to working- and middle-class Americans . . . . [a]nd that substitute, essentially, was cheap credit.” As the wealth that could have been used to grow average Americans’ real wages and income was instead redirected to the top 1%, the rest of us were encouraged to take on greater and greater private debt in order to continue expanding the economy so that even more economic growth could be funneled to those few people sitting at the top of the economic pyramid.

(h/t Seeking Alpha)

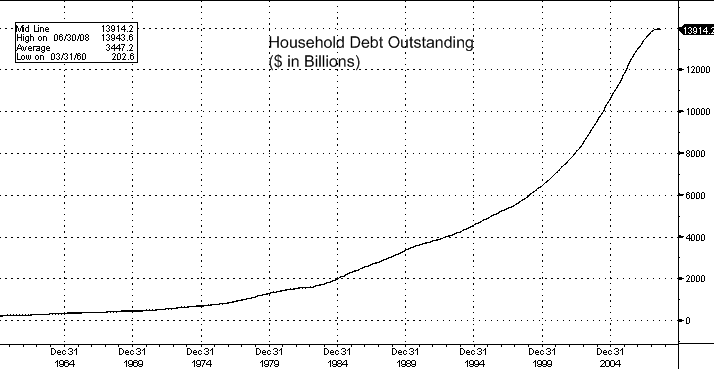

In 2009, after 30 years of this unsustainable plundering and just when the depth of the global financial crisis was beginning to be really felt but was not yet fully understood, John Kemp looked back over that 30 year period and summarized what had happened to America’s private debt-to-GDP ratio position as follows:

From the 1970s onward . . . the economy has undergone two profound structural shifts. First, the economy as a whole has become much more indebted. Output rose eight times between 1975 and 2007. But . . . . almost all this extra debt has come from the private sector . . . . Private debt outstanding has risen an enormous 22 times, three times faster than the economy as a whole, and fast enough to take the ratio of private debt to GDP from 117 percent to 303 percent in a little over thirty years. (emphasis added).

So . . . at the beginning of the financial crisis did private sector debt represent a "significant fraction" of GDP? Oh, yes -- it was

303% of GDP. And had private sector debt been growing at a faster rate than GDP? Oh yes -- for the past 30 years private sector debt had been growing

three times faster than the economy as a whole.

If Keen's analysis is correct, then the United States most definitely is caught in the Minsky-Keen trap.

So . . . What’s to be Done?

In practice, the most popular way of dealing with the recessionary effect of the private sector’s sudden unwillingness to take on more debt is to find a way to goose ‘em into doing it anyway – essentially, to get the private sector to refinance existing debt by collectively taking on even greater liability, like postponing one’s eventual default on a credit card by paying it off with an even bigger and more expensive line of credit. This, Keen argues, what his native Australia recently did.

Specifically, when Australia’s private debt growth rate suddenly fell from 11.5% in early 2008 to minus 5% in mid-2009, the abrupt drop in demand resulted in a severe economic contraction and a spike in unemployment. The government responded with a grant policy that succeeded in enticing 250,000 Australians to take out their first mortgages. The Australians receiving this grant money leveraged it to take out larger loans than they could otherwise afford, which drove up housing prices; their vendors then used this windfall in their own leveraged purchases. The dramatic upswing in mortgage debt more than offset the deleveraging being done by the business sector, and refinanced an apparent boom.

Or, as Keen describes it, “Australia has avoided the Global Financial Crisis by recreating the conditions that led to it. Needless to say, this is not entirely a good thing. We are potentially avoiding pain now by setting ourselves up for greater pain in the near future.”

But while it may not be wise in the long run, it was painless in the short term. And that, of course, is the charm of ever-expanding private debt. It gooses the economy nicely, so long as you don’t actually have to pay the bill.

Unfortunately (?), doing something similar is no longer an option for the United States. We’ve been kicking the can on our increasing levels of private debt for 30 years now, blowing up one asset bubble after the other. This is why, as the nifty chart below illustrates, when the Global Financial Crisis came a-calling America’s private debt was about 300% of its GPD, whereas Australia’s was about half that. This difference is why Australia could postpone its ultimate reckoning for a while longer, when the United States was unable to do the same – we just don’t have the flexibility.

The bottom-line is that – for America – there is no more debt to extend and not another asset bubble to inflate. There is no more road down which we can kick that can, and so the time has come when we are finally going to have to get out from under all that debt we’ve been encouraged to rack up over the past 30-odd years.

And this is where the practical power of the 1% and politics come into play.

* * *

As Ezra Klein explained in his article last weekend “Could This Time Have Been Different?” there are only two possible ways to get rid of debt:

[S]omebody has to pay it, or somebody has to take the loss on it.

The most politically appealing plans are the ones that force the banks to eat the debt, or at least appear to do so. “Cramdown,” in which judges simply reduce the principal owed by underwater homeowners, works this way. But any plan that leads to massive debt forgiveness would blow a massive hole in the banks. The worry would move from “What do we do about all this housing debt?” to “What do we do about all these failing banks?” And we know what we do about failing banks amid a recession: We bail them out to keep the credit markets from freezing up. . . . (emphasis added)

The very moment I first read that passage I loved it for the oh so precise, lawyer-like language that Ezra chose to use: “we know what we do about failing banks.” Note that he didn’t say “we know what

to do,” or “we know what we

should do” . . . . No, Klein knew exactly what he was saying here. We know what

we do about failing banks, whether it makes sense or not:

We bail them out. We don’t let them take a loss on their loans, no matter how stupidly and improvidently extended. We make sure the banksters get paid, no matter how bad they have proved to be at their jobs.

Why?

Well, I’m gonna go out on a limb here and say it’s because of all the reasons so many people have taken to the streets over the past few weeks as part of the Occupy Movement. Because the people that own the banks are the people who own the government, and they will get their money. Their agents in Washington – at least the ones who’ve decided they’d quite like to get re-elected to their agency positions – will make sure of that. No matter what else happens in America . . . The Banks Get Paid.

As Klein says, making the banks eat at least some of their debt has broad political appeal . . . but it just isn’t practical. And that’s the practical power of the 1%.

* * *

To explain the power of politics, here’s Ezra once more:

On first blush, there are few groups more sympathetic than underwater homeowners or foreclosed families. They remain so until about two seconds after their neighbors are asked to pay their mortgages. Recall that Rick Santelli’s famous CNBC rant wasn’t about big government or high taxes or creeping socialism. It was about a modest program the White House was proposing to help certain homeowners restructure their mortgages. It had Santelli screaming bloody murder.

“This is America!” he shouted from the trading floor at the Chicago Board of Trade. “How many of you people want to pay your neighbor’s mortgage that has an extra bathroom and can’t pay their bills? Raise their hand.” The traders around him began booing loudly. “President Obama, are you listening?”

If you believe Santelli’s rant kicked off the tea party, then that’s what the tea party was originally about: forgiving housing debt.

And that’s the power of politics: too many people get apoplectic when the government decides to help out their neighbors who may have gotten in over their heads (and, of course,

the Teabaggers know who those people are), when everyone who was cautious and played by the rules still has to fend for himself.

So the 1% demand that America’s debt be paid in full, and the Teabaggers demand that the debt be paid without help from the government, without even help form the government to refinance the existing debt. In this way the power of politics and the practical power of the 1% conspire to ensure that getting out from under America’s massive private debt is going to be as long and arduous a process as possible.

Forget about Japan’s “lost decade.” The length of time it may take to get out from under all the debt we were encouraged to rack up so as to distract us from the fact we were getting ripped off could result in a “lost generation” – and not the groovy kind, marked by witty banter, knowing ennui and great literature, but the kind marked instead by high unemployment, low wages, a worsening standard of living, and a growing expectation that things will never, ever get better.

Swell.

Fortunately, There is Another Way

And all it requires is defying either the power of politics, the power of the 1%, or both.

Defying the power of politics would require the government to step in and pay off a substantial amount of the private debt now owed to the banks. This would be Ezra Klein’s first stated option: “someone has to pay the debt.”

The 1% wouldn’t have to suffer a loss, but Americans would get out from under a substantial portion of their debt overhang almost immediately, freeing up economic gains to be invested in future growth instead of paying off existing debt. Of course, the Teabaggers would scream bloody murder about “moral hazard,” but they can be ignored.

They can be ignored because, well, they’re Teabaggers and we shouldn’t be paying attention to them anyway, but also because we are dealing with a fairly extraordinary situation right now. Resolving it may mean that some people – Hell! even a lot of people – get a lucky break and don’t get punished for doing stupid things like taking out loans they should have known they could never repay, but if letting somebody I don’t know catch a lucky break is the price I have to pay to get back a robust economy then I say Go with God, my friend!

(Just don’t think that the same weird rules apply if you screw up and the situation isn’t extraordinary. Just ‘cause you got lucky once doesn’t mean you won’t have to pay the price if you do something stupid after things have settled back down to normal. But for right now . . . if helping you helps me, then I’m all about helping you.)

But defying the practical power of the 1% would be even more satisfying. This would be Ezra’s second stated option: somebody has to take a loss.

There is absolutely no reason – well, no good reason – why the United States should continue to keep pumping its money, its heart’s blood, into the lifeless corpse that the financial industry has become. These zombie banks have already acknowledged that they need the government to keep bailing them out in order to continue doing business. When someone has so screwed up their company that it can no longer exist without continuous, massive government subsidies, then – I’m sorry – there’s no longer a place for that company in America.

(It’s not me, Mr. Bankster . . . it’s the free market. I’m just enforcing the rules.)

We could almost immediately get out from under our debt overhang by placing these insolvent banks into a nationally administered receivership during which the flow of working capital could be maintained while they were forced into legal bankruptcy proceedings. A legal bankruptcy would destroy the equity holders in these zombie banks and would require the banks themselves to recognize losses and write off huge amounts of the debt overhang that is now crippling the American economy.

Best of all, it could be done quickly.

By exercising either option, or some combination of the two, the American government could immediately effect the deleveraging that - if dragged out - threatens to cripple us for a generation. Best of all, the only ones who would get hurt would be the people responsible for dragging us to this precipice in the first place: the 1% who fostered our enormous private debt so they could cram their own maws with as much of the American economic pie as they could shovel in.

The Teabaggers wanna talk “moral hazard”? Not making the 1% take responsibility for what they have done to this country for thirty years, for the rapacious, self-aggrandizing, self-centered blindness of what they were doing . . . that would foster moral hazard.

The country needs to get out from under its debt. After 30 years of taking, I say it's time the 1% gave us something back.

Cross-posted at Casa Cognito.