As far as I know, I'm still allowed to demand honest journalism these next six months so here we go. Apparently it's not enough that Andrew Ross Sorkin is obviously not in it for anyone else besides himself and his access to Wall St. There's not a pro banker bias he won't proudly wear on his sleeve. You really get the feeling he secretly wishes he was an investment banker instead of a terrible writer and fake journalist.

His latest POS takes some half truths to extremes regarding the Glass Steagall Act and how "useless" it would have been in this crisis. It is true that the Glass Steagall Act is not a panacea for everything and it's repeal wasn't the only thing that caused the financial crisis. Notably the Commodity Futures Modernization Act deregulating derivatives is also quite noteworthy among a multitude of other things.

It's true that there would have still been a housing bubble, though the repeal of Glass Steagall added to the housing bubble making the fallout a lot more unmanageable. However, this effort to downplay its importance is quite disingenious. It's ultimately not surprising coming from a banking shill like Andrew Ross Sorkin though; one who pictures himself as part of the big boy club now.

So Let's take on his piece, piece by piece.

But here’s the key: Glass-Steagall wouldn’t have prevented the last financial crisis. And it probably wouldn’t have prevented JPMorgan’s $2 billion-plus trading loss. The loss occurred on the commercial side of the bank, not at the investment bank. But parts of the bet were made with synthetic credit derivatives — something that George Bailey in “It’s a Wonderful Life” would never have touched.

For someone who based his article on Glass Steagall, Andrew Ross Sorkin has a grade school level of knowledge about it. He seems blissfully unaware about what happened recently with JP Morgan. Perhaps he doesn't care?

Alexis Goldstein does. It looks like she and

Occupy the SEC have to school him on Jamie Dimon using the portfolio hedging loophole in the Volcker rule within Dodd Frank. This, of course, was what brought on JP Morgan's recent losses unbeknownst to Andrew's pseudo "expertise."

Occupy the SEC to Jamie Dimon: We Told You So

Several visits over months by the bank’s well-connected chief executive, Jamie Dimon, and his top aides were aimed at persuading regulators to create a loophole in the law, known as the Volcker Rule. The rule was designed by Congress to limit the very kind of proprietary trading that JPMorgan was seeking.

“JPMorgan was the one that made the strongest arguments to allow hedging, and specifically to allow this type of portfolio hedging,” said a former Treasury official who was present during the Dodd-Frank debates.

Portfolio hedging is at the heart of the London Whale debacle.

The loophole is known as portfolio hedging, a strategy that essentially allows banks to view an investment portfolio as a whole and take actions to offset the risks of the entire portfolio. That contrasts with the traditional definition of hedging, which matches an individual security or trading position with an inversely related investment — so when one goes up, the other goes down.

Portfolio hedging “is a license to do pretty much anything,” Mr. Levin said. He and Senator Jeff Merkley, an Oregon Democrat who worked on the law with Mr.Levin, sent a letter to regulators in February, making clear that hedging on that scale was not their intention.

“There is no statutory basis to support the proposed portfolio hedging language,” they wrote, “nor is there anything in the legislative history to suggest that it should be allowed.”

Oops, it looks like Glass Steagall could have helped stop this after all. It would put a wall between

proprietary trading and FDIC backed deposits used as collateral since the Volcker rule is just Glass Steagall lite(limitations on proprietary trading). I guess Andrew Ross Sorkin might need to study harder.

I'll skip the part where Sorkin pesters Elizabeth Warren and on to another canard I've even heard sadly even repeated by some here(hoping to wash away the stench of the Rubin philosophy and its practitioners still prevalent in a Democratic administration today) about certain firms not having commercial banking arms. This is supposed to be some sort of a genuine insight as to how Glass Steagall repeal can't be significant from Sorkin's peice.

The first domino to nearly topple over in the financial crisis was Bear Stearns, an investment bank that had nothing to do with commercial banking. Glass-Steagall would have been irrelevant. Then came Lehman Brothers; it too was an investment bank with no commercial banking business and therefore wouldn’t have been covered by Glass-Steagall either. After them, Merrill Lynch was next — and yep, it too was an investment bank that had nothing to do with Glass-Steagall.

Whether Bear Stearns, Lehman Brothers, or Merril Lynch had commercial banking arms or not is absolutely irrelevant to Glass Steagall. All it takes is a few originators with bad underwriting standards brought on by the slow repeal of Glass Steagall in the 80s and the final blow with Gramm Leach Bliley in 1999 to spread this junk everywhere. ALL of these investment banks were brought down by subprime mortgage backed securities losses. Guess what?

Municipalities and public and private pension funds who investing in MBS didn't have commercial banking either and also went bust so they busted the unions like in WI. You see, only people completely ignorant or dishonest like in Andrew Ross Sorkin's case don't know how these investment banks with no commercial arms had investments in bad mortgages(MBS). It doesn't matter at all which banks had commercial banking arms because some of them did.

They were able to distribute these bad mortgages across the financial system to be securitized and package up into (CDOs), sell them off, and didn't have to hold them(“originate and hold”) or be responsible for them like banks used to. They were sold to other institutions(and different kinds of institutions) that didn't have commercial banking arms which is also how they wound up poisoning public pensions in states across the U.S. causing them to go broke. What a piss poor uninformed, excuse. It's time to go back to school. Originate to distribute 101.

Research and consulting firm Celent released a study yesterday titled, “Pathology of the US Mortgage Crisis,” which examines the evolution of the credit crunch from its humble beginnings as a U.S. subprime mortgage problem to the subsequent global liquidity crisis that ensued.

The Boston-based firm noted that the global credit market saw a “flight of uncertainty” over the past nine months that led to billions in associated write-downs, the fall of investment banking giant Bear Stearns, and multiple emergency rate cuts by the Fed.

[...........]

Essentially, most originating banks and mortgage lenders only held onto mortgages long enough to sell them off to investors, promoting a higher-risk environment for loan origination.

Under this system, mortgage brokers and originating banks had volume-based incentives that weakened underwriting standards, while investment banks and Wall Street firms worked on loan performance incentives.

This disparity caused scores of low quality loans to funnel through the system and find their way into structured investments that eventually spoiled as home prices began to stagnate and fall, and mortgage defaults began to surge.

I'll save you the trouble of reading the rest of Andrew Ross Sorkin's excuses for Bank of America and other big commercial banks. It's basically, "They only acquired banks with massive subprime losses, they didn't do it themselves!" You know it's really ironic that he wrote the book

Too Big to Fail while failing to get why it is a problem.

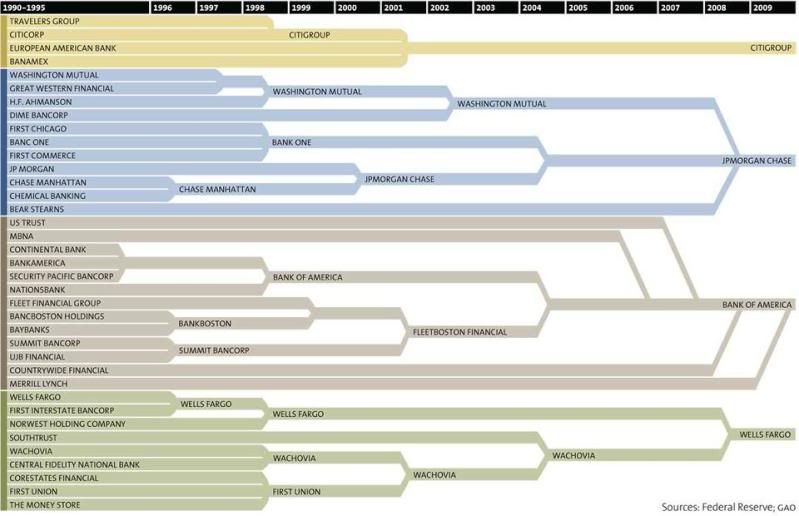

He admits Glass Steagall had something to do with Citigroup, which is good because Citicorp, Citibank, and Travelers Insurance Company couldn't merge together to form Citigroup without the repeal. I'd hope he would at least know that much if nothing else. He talks about AIG being separate from Glass Steagall which is true, but AIG is where the Commodity Futures Modernization Act comes to play.

Fannie and Freddie only got involved in junk after the game started which I already explained(many many times to the RW) as those junk bonds were originated and distributed though the entire system; the fatal flaw in Andrew Ross Sorkin's pseudo analysis. The bottom line is that we need an updated Glass Steagall Act and we need to break up the TBTF banks. Their political power is what's most dangerous though they are dangerous on multiple levels. Robert Reich gets this.

Break Up the Banks. They’re Too Big to Regulate

That’s why, as a practical matter, the Volcker Rule is hopeless. It was intended to be Glass-Steagall lite -- a more nuanced version of the original Depression-era law that separated commercial from investment banking. But JPMorgan has proven that any nuance -- any exception -- will be stretched beyond recognition by the big banks. So much money can be made when these bets turn out well that the big banks will stop at nothing to keep the spigot open.

There’s no alternative but to resurrect Glass-Steagall as a whole. Even then, the biggest banks are still too big to fail or to regulate. We also need to heed the recent advice of the Dallas branch of the Federal Reserve, and break them up.

And to keep them from reforming we need stronger antitrust laws and enforcement as well as adding to the basic firewall represented by Glass-Steagall as BruceMcF outlines well in this piece:

In a traditional partnership, the partners are not protected by corporate limited liability. A partnership goes bankrupt because the senior partners are completely tapped out ~ not just savings, but house, car, working lawn mower ... the works.

In the post-WWII era, investment banks switched from traditional partnerships to corporations ~ but they were closely held corporations, rather than publicly traded, and so they were still not consumers of their own underwriting services. And even if the senior partners were no longer subject to losing their car if the firm went bankrupt ~ they were still subject to losing a massive chunk of their personal wealth and, perhaps just as importantly, could not inflate their wealth merely by impressing traders in the public stock markets.

[............]

However, reconstituting Glass-Steagall would still leave us with the incestuous mess of investment banking service being provided by publicly trade corporations.

So what I argue is that we should add to the basic firewall represented by Glass-Steagall, and also forbid publicly traded corporations from engaging in investment banking activity or owning corporations that engage in investment banking activity.

That's an updated Glass Steagall we can believe in. That way assuming we are able to pass something like Brown Kaufman anytime soon it's less likely the big banks will re-consolidate like the vampire squids they are. And there within lies the problem that I'm not allowed to talk about on this site very much, anymore.

No one is talking about any regulatory system they are for in this campaign. It's all about Romney and Bain, which is fair game, but more of a bipartisan problem than we can comfortably admit. There are some Democrats trying on the right side of ending TBTF, even though they are a minority it seems. Many Democrats pretend like they are against TBTF until it is time for a vote.

Senator Sherrod Brown is reintroducing the Safe Banking Act of 2012 again(after many sellout Democrats voted it down in 2010) to try to break up the TBTF banks, but I don't hear the White House campaigning on it. At least they're not actively campaigning against it this time, I guess, as they did in 2010 upholding TBTF.

I assume since Sherrod Brown is a Democrat, I'm allowed to point this out, but who knows? I do know you know now, if you didn't already, that if you want sound economic or financial analysis, Andrew Ross Sorkin is not where it's at.