In recent weeks, Mitt Romney's presidential campaign has tried to redefine the calendar by inserting the new milestone "AB"—or "After Bain"—into the timeline of human history. Defending its man from damaging reports that he profited when Bain Capital invested in companies that shipped jobs overseas, extracted massive dividends and fees from firms that later failed and even harvested cash from medical waste, the Romney camp routinely protested that most of these episodes occurred "after Mitt left Bain."

Unfortunately for the Republican, Americans are catching on to Mitt Romney's "after Bain" immaculate deception. A growing mountain of evidence suggests that Romney continued to play an active role at Bain even after his supposed February 1999 departure for the Salt Lake Olympics. And as the New York Times documented back in December, Romney's sweetheart deal with the Bain Capital private equity firm he founded ensures that Mitt continues to make millions every year from his old employer.

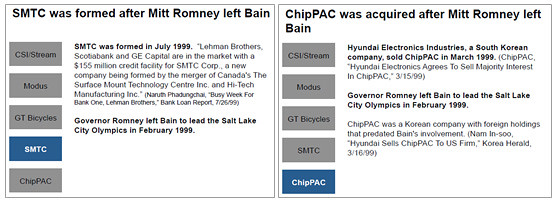

As David Corn and Nick Baumann detailed in Mother Jones, "Romney left Bain later than he says." Confronting the revelation that he was involved in a lucrative Bain investment in a firm that disposed of aborted fetuses among other medical waste, the "After Bain" card was turned over again:

In response to questions from Mother Jones, a spokeswoman for Bain maintained that Romney was not involved in the Stericycle deal in 1999, and insisted he had "resigned" from the company months before the stock purchase was negotiated. The spokeswoman noted that following his resignation Romney remained only "a signatory on certain documents," until his separation agreement with Bain was finalized in 2002. And Bain issued this statement: "Mitt Romney retired from Bain Capital in February 1999. He has had no involvement in the management or investment activities of Bain Capital, or with any of its portfolio companies since that time." (The Romney presidential campaign did not respond to requests for comment.)

But the document Romney signed related to the Stericycle deal did identify him as an participant in that particular deal and the person in charge of several Bain entities. (Did Bain and Romney file a document with the SEC that was not accurate?) Moreover, in 1999, Bain and Romney both described his departure from Bain not as a resignation and far from absolute. The Boston Herald on February 12, 1999 reported, "Romney said he will stay on as a part-timer with Bain, providing input on investment and key personnel decisions." And a Bain press release issued on July 19, 1999, noted that Romney was "currently on a part-time leave of absence"--and quoted Romney speaking for Bain Capital.

But in the big picture, the timing of Bain Capital's

investments in and profits from companies like Stericycle, Dade-Behring or Modus Media ultimately doesn't matter very much. Because as the

New York Times explained late last year, Romney's financial future remains with Bain even after Mitt left the building:

Though Mr. Romney left Bain in early 1999, he received a share of the corporate buyout and investment profits enjoyed by partners from all Bain deals through February 2009: four global buyout funds and 18 other funds, more than twice as many overall as Mr. Romney had a share of the year he left. He was also given the right to invest his own money alongside his former partners. Because some of the funds and deals covered by Mr. Romney's agreement will not fully wind down for several years, Mr. Romney is still entitled to a share of some of Bain's profits.

One of the reasons why the

Washington Post refused the Romney campaign request to retract its story about Bain outsourcing is precisely because,

as the paper put it, "Romney and Bain shared in their profits while he was chief executive and after he left."

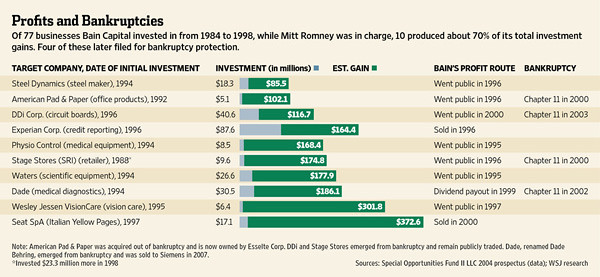

Those shared profits were quite large. And as the New York Times and the Wall Street Journal showed, Romney and his partners at Bain pocketed them even when the companies they invested in failed. During tenure as CEO from 1984 to 1999, Bain invested in 40 companies in the U.S. While seven later went bankrupt, the Times found that "In some instances, hundreds of employees lost their jobs. In most of those cases, however, records and interviews suggest that Bain and its executives still found a way to make money." That mirrors a January 2012 analysis by the Wall Street Journal, which revealed:

Bain produced stellar returns for its investors--yet the bulk of these came from just a small number of its investments. Ten deals produced more than 70% of the dollar gains.

Some of those companies, too, later ran into trouble. Of the 10 businesses on which Bain investors scored their biggest gains, four later landed in bankruptcy court.

Reflecting on his private equity career, Romney in 2007 sounded almost remorseful that the pain from Bain fell mainly on the plain:

"It is one thing that if I had a chance to go back I would be more sensitive to," Mr. Romney said. "It is always a balance. Great care has got to be taken not to take a dividend or a distribution from a company that puts that company at risk." He added that taking a big payment from a company that later failed "would make me sick, sick at heart."

Not so sick at heart, though, to make President Romney change the

two key elements of the federal tax code that keep the American private equity gravy train running at full speed. For starters, Romney opposes ending the notorious "

carried interest exemption" that allows him and fellow fund managers to pay only 15 percent—and not 35 percent—to Uncle Sam from capital gains and dividend income. It is that rule that allowed Mitt to pay a lower effective tax rate on his $45 million, two-year income

than many middle class families. Just as important, central to the business model of Bain and other private equity firms is the tax deductibility of corporate debt. In January,

The Economist explained how the perverse incentives work:

From 2004 to 2011 private-equity firms piled more debt onto their companies so they could take out $188 billion in dividends to pay themselves. The deals got bigger and bigger. The largest ever, in 2007, was the $44 billion purchase of TXU, an electricity company. The market worries the company will go under.

But though the private-equity people may have walked off with the loot, America's tax code was partly to blame, because it encourages this behaviour. The tax deductibility of interest payments on debt gives private-equity executives an incentive to pile extra debt onto the companies they buy, thereby risking the health of these firms for the sake of a tax benefit and the prospect of higher returns.

"Traditionally," Josh Kosman wrote in his 2009 book

The Buyout of America, "cash-rich public companies have paid dividends to lure and reward investors." But private equity firms, he explained, stand this process on its head. "Fourteen of the largest American private equity firms had more than 40 percent of the North American companies they bought from 2002 until September 2006 pay them dividends, "Kosman pointed out, adding, "In thirty-two of the eighty-three case, 38 percent, they took money out in the first year." And the innovator behind the business model?

Mitt Romney was a pioneer of this strategy. His private equity firm, Bain Capital, was the first large PE firm to make a serious portion of its money not from selling its companies or listing them on the stock exchange, but rather by collecting distributions and dividends, which in this context is the exact opposite of reinvesting in a company. Bain Capital is notorious for failing to plow profits back into its businesses.

That is Mitt Romney's legacy. Even now.

After Bain.