The Libor scandal continues to grow. Now that we have a clear idea of how the deception was perpetrated, one can develop an appreciable sense of how this scandal will develop in Europe and, eventually, in the United States. The crisis has not received as much attention in North America as it has across the Atlantic. That will change as litigation moves through the system.

Lawsuits that began nearly a year ago bring sunshine into the idea that banks rigged the credit markets to their own advantage. The go-go real estate days of the past decade inflated credit market bubbles just as they artificially inflated real estate prices. That perspective will bring clarity and relevance of Libor manipulation to the American public.

Former Labor Secretary Robert Reich argues that U.S.-based banks must be complicit in this international fraud ring.

The biggest Wall Street banks – including the giants JP Morgan Chase, Citigroup and Bank of America – are likely to have been involved in similar manoeuvres. Barclay's couldn't have rigged the Libor without their witting involvement. The reason they'd participate in the scheme is the same reason Barclay's did – to make more money.In fact, Barclays' defence has been that every major bank was fixing Libor in the same way, and for the same reason. And Barclays is "co-operating" (giving damning evidence about other big banks) with the justice department and other regulators in order to avoid steeper penalties or criminal prosecutions, so fireworks in the US can be expected.

In other words, it's only a matter of time before the legal firestorm envelops U.S. banks that deal in derivatives markets worth

hundreds of trillions of dollars.

The Scotsman reports that in Canada, the Royal Bank of Scotland is fighting a court order that it cooperate with an international criminal investigation in rate rigging:

The Canadian case, which has not yet filed charges against any of the banks or individuals, has named six banks as being involved in fixing the Yen Libor rate. As well as RBS, the papers feature claims against London-based bankers from Citigroup, Deutsche Bank, HSBC, JP Morgan and UBS.

Clearly, there is something the banks wish to hide from daylight. While Canada wrestles with an investigation, American entities associated with banks have decided to press harder with their own discovery process.

Here come the lawsuits.

The paper trail on Libor rate manipulation has been growing for a long time. Papers were filed almost one year ago when Charles Schwab Corp accused several banks of manipulating rates that stole billions of dollars. States and municipalities have been hit hard with Wall Street's creative public financing contracts over the past decade.

More than a dozen banks, including Citigroup, HSBC and UBS, have been caught up in the probe and have been sued in proposed class-actions by plaintiffs including the city of Baltimore and Frankfurt-based Metzler Investment GmbH, which manages 47 billion euros ($59 billion) in assets. The plaintiffs brought antitrust claims against the banks, saying they were bilked of potentially billions of dollars.

Billions of dollars, indeed. The market for interest rate derivatives is nothing short of mind-blowing. The

Sherman Antitrust Act allows for plaintiffs to receive triple damages if collusion and intent can be proven. This (PDF)

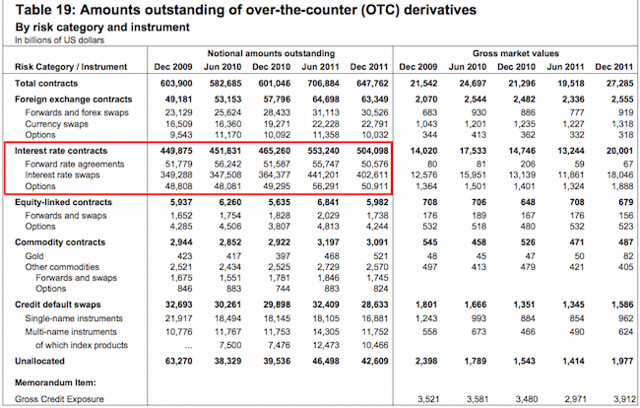

report from the Bank of International Settlements (BIS is the central bank to the world) assesses the number of derivative contracts that exist between banks, other financial services firms and clients. The interest rate derivatives, relating directly to Libor, are outlined in red.

Remember - the numbers are scaled in billions of dollars. That monetary scale would overwhelm banks if they are proven in court to have manipulated contracts of this size to their advantage.

As Yves Smith of Naked Capitalism reveals: number crunchers are working furiously at this moment to find out who was harmed and by how much with manipulation in derivative markets. Smith, as I, quotes The Economist to get some sense of the frequency and duration of this type of market manipulation:

Barclays was a leading trader of these sorts of derivatives, and even relatively small moves in the final value of LIBOR could have resulted in daily profits or losses worth millions of dollars. In 2007, for instance, the loss (or gain) that Barclays stood to make from normal moves in interest rates over any given day was £20m ($40m at the time). In settlements with the Financial Services Authority (FSA) in Britain and America’s Department of Justice, Barclays accepted that its traders had manipulated rates on hundreds of occasions.

'Hundreds of occasions' could extend for years - and only for Barclays.

Other Sources:

Banks’ Defenses to Potential Trillions in Libor Claims Fail

Analysis: Investors may shun big Libor lawsuit and go it alone

Banks face crippling Libor litigation costs