The London Interbank Offered Rate (LIBOR) is arguably the single most important short-term interest rate in the world. Loans for mortgages, credit cards, small businesses and automobiles are just a few of the credit products that reflect a relationship with LIBOR. Using some basic math and a step-by-step calculations, we can demonstrate how Barclays and other banks extracted wealth from trading partners and customers.

Just bear in mind that LIBOR is the benchmark for short-term loans of varying duration not exceeding one year. Loans are structured on a 31-day month, 360-day year.

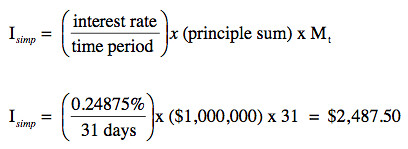

To demonstrate how basic interest formula works, simple interest is calculated using real numbers and a LIBOR interest rate quote from last week for a $1 million loan for one month. The interest rate of 0.24875% is the average for this duration.

M(t) denotes the measure of time - the duration of the loan in the number of days. You can notate this formula a different way. The answer will be the same as above.

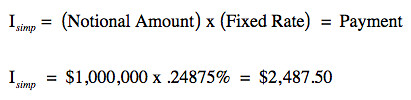

Interest rate swap formula is where this calculation gets a bit more complicated. Banks will often enter swap agreements with their customers. A 'swap' is an arrangement in which banks will occasionally exchange interest rate payments. Swap agreements provide banks a primary target for market manipulation. In essence, banks have the power of little gods to control the flow of global capital.

Next: How they did it.

The next calculation comes from Dr. Galen Burkhardt's book, The Eurodollar Futures and Options Handbook. Bank A borrows money at a fixed rate from Bank B. Bank A will then receive a quarterly payment calculated as the difference between the fixed rate and the floating LIBOR rate.

This equation uses simple interest operations above as its basis.

Since the rate went down over this period, the Bank B made money on a manipulated 3-month LIBOR. Conversely, the counterparty to the trade lost money. This quarterly interest rate reset involves a monetary transfer at that time. It means that over the course of the loan, the cost of money can rise artificially.

Mind you, a one million dollar notional value used in these examples is an unrealistically puny loan amount. Loans are routinely structured in billions (frequently tens of billions) of dollars. These rates set every day. So the sums of money and the velocity of capital moving through the world's financial system amplifies the effect of tweaking the rate as little as one basis point, or 1/100th of one percent. As such, great sums accumulate in the hands of banking giants almost daily.

Conspiracy or not, manipulation is manipulation.

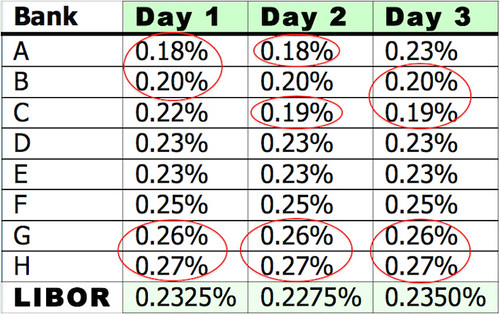

Below is a table that demonstrates Verstein's Analysis -created by Yale University Law School lecturer Andrew Verstein. The message to take away here rests with how banks can manipulate rates in either direction even without a conspiracy. Verstein demonstrates how the system is flawed on a number of levels -primarily the localized level where any bank with enough pull to influence LIBOR can use rate submissions to hedge its trading position without any regard either for other banks, customers or trading partners.

LIBOR's daily calculation uses the basic statistical method that eliminates the outliers (lower and upper quartiles) to determine the daily lending rate.

The table I have constructed here shows the daily interest rate submissions of eight fictitious banks. The standard method for calculating LIBOR removes the highest and lowest interest rate submissions, circled here in red. With the top and bottom quartiles excluded, the middle quartile is averaged. For instance: On Day 1 the formula for LIBOR is (0.22 + 0.23 + 0.23 + 0.25)/4 = 0.2325%.

Why is this important?

Barclays is known to have submitted unusually high rates to Thomson Reuters which compiles LIBOR data on behalf of the British Bankers Association. If Barclays submission was so high as to be thrown out of the middle quartile, they could nudge the interest rate in a direction that benefitted their trading position in swaps, increase the value of their books and diminish their trading losses.

Interest rate manipulation also impacts the fluctuating value of the hundreds of trillions of dollars in the derivatives market. A falsely reported interest rate can hide the poor fiscal health of a too-big-to-fail bank.

If you spot any error in my calculations, please let me know. This is cross-posted at Macroindex.

Sources:

The U.K. Financial Services Report on Barclays

The Commodity Futures Trading Commission Report on Barclays

Libor Flaws Allowed Banks To Rig Rates Without Conspiracy

How Barclays Made Money On LIBOR Manipulation

What is LIBOR Market Model (LMM)

Introduction to Interest Rate Swaps

Wall Street Journal Market Data Center

Bloomberg BBA LIBOR USD 3 Month

Libor Flaws Allowed Banks To Rig Rates Without Conspiracy