The LA Times reports a better than expected jobs report showing the unemployment rate fell to a four year low, of 7.6 percent, due to the addition of 146,000 jobs, but also due, in part, to a large number of discouraged workers dropping out of the workforce.

The U.S. added more jobs in November, sending stock index futures up in pre-market trading immediately after the report was released. But underneath the headline numbers, the monthly report gave a mixed read on the economy.

The main numbers from the jobs report were encouraging. The Labor Department said the U.S. added 146,000 jobs last month. The unemployment rate fell to 7.7 percent from 7.9 percent, the lowest since December 2008.

This much is great news signaling that our economy is moving in the right direction, however, as we look at the details we see more of a mixed picture.

The unemployment rate fell largely because discouraged unemployed workers stopped looking for work, and weren't counted among the unemployed. Also, the Labor Department revised previously released jobs numbers downward, saying that employers added 49,000 fewer jobs in October and September than initially estimated.

Lund also wasn't so sure about the government's statement that Hurricane Sandy “did not substantively impact” the unemployment numbers. He expected Sandy's detrimental effects to show up in jobs reports over the next couple of months, as businesses figured out their post-storm plans.

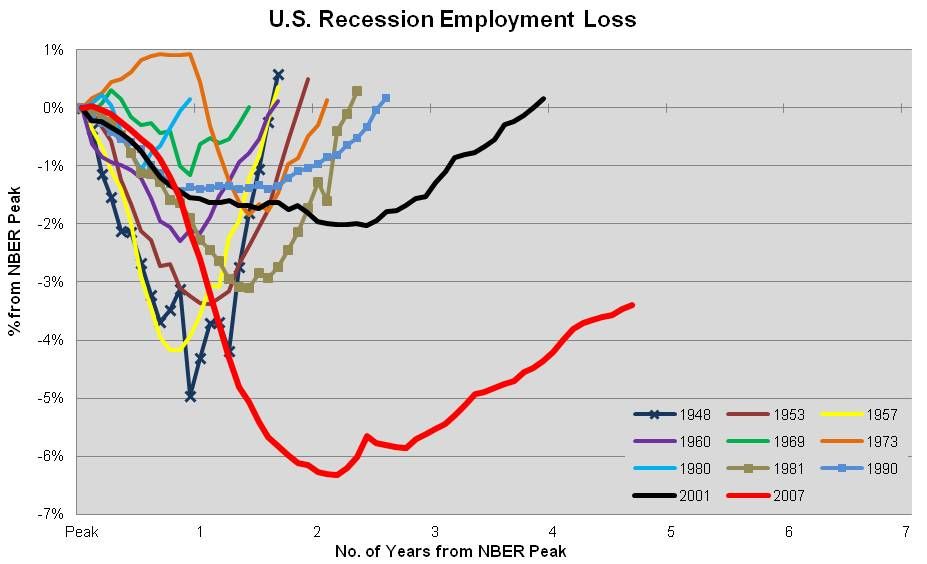

Our unemployment numbers are still well above historical levels for this phase of the 4-7 year business cycle. For example, in the the recession of the early 2000s. the unemployment rate never exceeded 6.3 percent. At the high point of this recession, unemployment hit 10 percent and staid above 9 percent for almost two years.

To me, the data indicates we are suffering from multiple problems and we are seeing what is called the "super-positioning of multiple modes" of economic behavior. The data is not showing a typical business cycle recovery because the underlying economic forces causing us the most trouble are not those of the classic shorter-term "inventory work-force adjustment" that many believe are the driving causal dynamics of the business cycle.

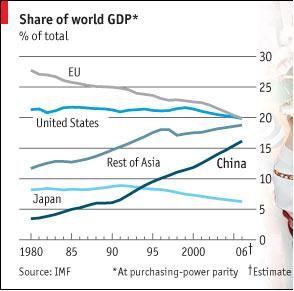

What we are experiencing now, seems to me to be driven by a longer-term decades long trend in the loss of manufacturing jobs due to lower wages, less regulation, and targeted national industrial strategies in emerging nations in South-East Asia, and Latin America - and especially in China, where global multinational corporations can install the latest manufacturing technology and find an eager, relatively well educated workforce, willing to work for $2,000 to $,4,000 a year. And, favored industries in these nation's industrial plan often received huge subsidies, tax and regulatory forgiveness.

A few years ago, I read that highly well educated Indian Ph.D.s in computer programming earn the equivalent of $7,500/year. And, we well know the result of Japan's three decades long industrial strategy, starting in the 1950s, to capture the American automobile, and consumer electronics markets. China has announced the same kind of plan, including a declared intention to dominate the emerging solar, wind, and other renewable energy technologies, most of which were invented and developed originally in the U.S., giving their solar industries $30 billion in start-up subsidies. We can no longer ignore these competitive challenges.

Many of these jobs the U.S. has lost to "off-shoring" are not coming back, especially, where labor costs are a primary component. But, rather than become discouraged, our best strategy is to recognize that for many products the labor share of total product cost is now much smaller than it used to be. As of about a decade ago, I was surprised to learn that the labor share of the automobile cost was less than 7 percent.

And, Apple Computer is considering bring production of the Mac back to the U.S.

The U.S. has significant cost advantages in energy costs and political stability.

But, we also need to amplify the debate over the "fair trade - free trade" issues unions have been trying to bring to our attention for decades. The recent fire at the Walmart in Bangladesh, due to inadequate fire protection, allegedly involving deliberate prioritization of cost-control over worker safety, illustrates that unless we have a more level global playing field, economic policies of totally free trade, and free markets will drive global wages towards those countries with the lowest costs, industrial policy advantages, and lowest environmental and safety regulation.

Also, we need to develop a national industrial policy and strategy for improving our nation's competitiveness in the free market, as virtually all other advanced and emerging economies have done. Our stubborn refusal to do so, based on free market ideological purity, comes from an arrogance, and unfounded assumption, that the US has such vast economic superiority over all the rest of the world that we do not need to be strategic about our competitiveness. The data increasingly demonstrates this assumption is not true.

Improving America's economic vitality and international competitiveness should be an area of common interest with all sides of our divided political spectrum. Our political battles will become more bitter if we are fighting over ever smaller pieces of a shrinking pie. President Obama could exert much needed leadership by expanding our economic discussion to ways we can improve our national industrial health and competitiveness with wiser global strategies.

In this regard President Obama's modest $50 billion for an infrastructure bank should be the first of just many such investments in upgrading our electrical grid, accelerating our conversion to sustainable energy generation, and other enhancements to our industrial vitality that will pay rich dividends in a more prosperous future.

10:12 AM PT: More data that helps us visualize troubling long-tern economic issues beyond that of mere business cycle dynamics and should be upmost in the minds of shorter sighted politicians about to set off an austerity bomb at perhaps one of the worst possible moments.

10:16 AM PT: