Much hay has been made over President Obama's "if you like your insurance, you can keep it" campaign-style pledge. Lately, there has been some blowback over this pledge: some Americans are getting letters in the mail saying their coverage has been canceled, and they are being "forced" into more expensive insurance plans. But just how prevalent is this issue?

An MIT economist and health insurance expert says it's not as common as it has been portrayed in the media and elsewhere.

Hit me up below the fold for more.

Jonathan Gruber is an economist at the Massachusetts Institute of Technology, and one of the architects of the individual mandate under Massachusetts' "RomneyCare" and the Affordable Care Act (ACA) as well. In The New Yorker, Gruber discusses the health care law's winners and losers.

Here are the highlights:

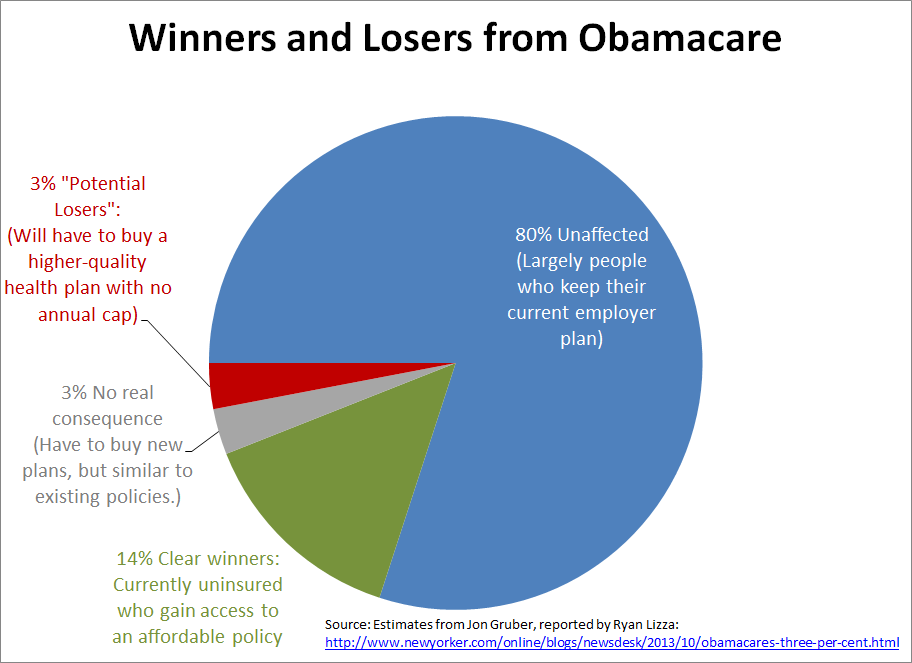

- 80% of Americans get insurance through their employers and are relatively unaffected.

- 14% of Americans were previously uninsured and will finally gain access to affordable health care through the exchange.

- 3% of Americans buy insurance on the individual market, and they will not see a significant change in their policy. Some of them will save money over their previous insurance.

- 3% of Americans who are in the individual insurance market will have to pay more for an ACA-compliant plans.

Or, in convenient chart form, courtesy of Gruber's Twitter account:

According to Gruber, 3% of Americans, or about half of those currently participating in the individual insurance market, will pay more for an ACA-compliant plan. But what composes this 3%? Here's The New Yorker's Ryan Lizza and Gruber:

The primary reason for the increased cost is that the A.C.A. bans any plan that would require a people who get sick to pay medical fees greater than six thousand dollars per year. In other words, this was a deliberate policy decision that the White House and Congress made to raise the quality—and thus the premiums—of insurance policies at the bottom end of the individual market.

“We’ve decided as a society that we don’t want people to have insurance plans that expose them to more than six thousand dollars in out-of-pocket expenses,” Gruber said. Obama obviously should have known that his blanket statement about “keeping what you have” could not apply to this class of policyholders.

[Ed. Note: The

actual out-of-pocket maximum is $6,350 for an individual plan and $12,700 for a family plan.]

Most of these plans are "insurance in name only"--plans that don't actually protect the policy holder from financial ruin in case of a health emergency. Even still, there are some individual insurance plans that are sufficient, but are required to be upgraded to fit the ACA minimum standards. One group likely to see this change is single, healthy men who have to purchase extra benefits like maternity care.

However, most media reports overlook the fact that this is part of the ACA's sweeping reform of the individual insurance market. In the old system, young women considering having kids would have to pay considerably more when selecting maternity coverage. In a sense, they were subsidizing the ability of men to get a very inexpensive plan. Now, with the ACA, the playing field has been leveled and everybody in the individual insurance pool gets the same benefits.

The bottom line is that the number of people who have to pay more for additional benefits perhaps considered unnecessary is very small--less than 3% of the population. But this does not take into account the extra ACA benefits that may not be printed in the insurance policy: insurance carriers can no longer drop you if you get sick, you can elect to change insurance policies without worrying about preexisting conditions, free preventive care, and the medical loss ratio which prevents insurance companies from padding their profits too much.

It's easy to forget that those same benefits mentioned in the above paragraph are available even to the vast majority of Americans who will see little to no change. Their insurance coverage is improved thanks to the ACA. Some of them will even save a lot of money compared to before the enactment of ACA.

So the next time you see a hysterical media report about how the president didn't keep his promise, or a report scant on details saying that someone is going to pay more, keep it in context of the goals of the ACA, the additional benefits included in the new policies, and the 14% of Americans who weren't able to buy insurance before.

Oh, on a side note, what does Gruber have to say about those pesky website problems?

Gruber’s view is that, at the moment, the technical problems associated with healthcare.gov are only a “DefCon 4 problem”—mostly just a political headache for the White House.

Yeah, that's what I thought. Not exactly the "Katrina moment" the media is making it out to be.