Ok. So I'm signing my 28 year old son up for health insurance under Healthcare.gov. After the initial craziness the first ten days of October, I was able to finally get him an account so that I could shop the plans.

It's the plans that are the issue.

Please read over the fold and help me find a basis for appeal, ok? I'm stuck.

So the son, let's call him Jake, is a 28 year old who does not use tobacco products. he works as a waiter, and his income in 2012, before taxes, was between $22K and $23K. We live in Virginia, so we have to use the Health Insurance Marketplace (asshat McDonnell declined to have VA set up its own exchange).

After subtracting income, SS, and Medicare/Medicaid taxes, his AFTER TAX income is between $19K and $20K.

His average monthly BEFORE tax take home pay is $1,866. His average monthly AFTER tax take home pay is $1,654.

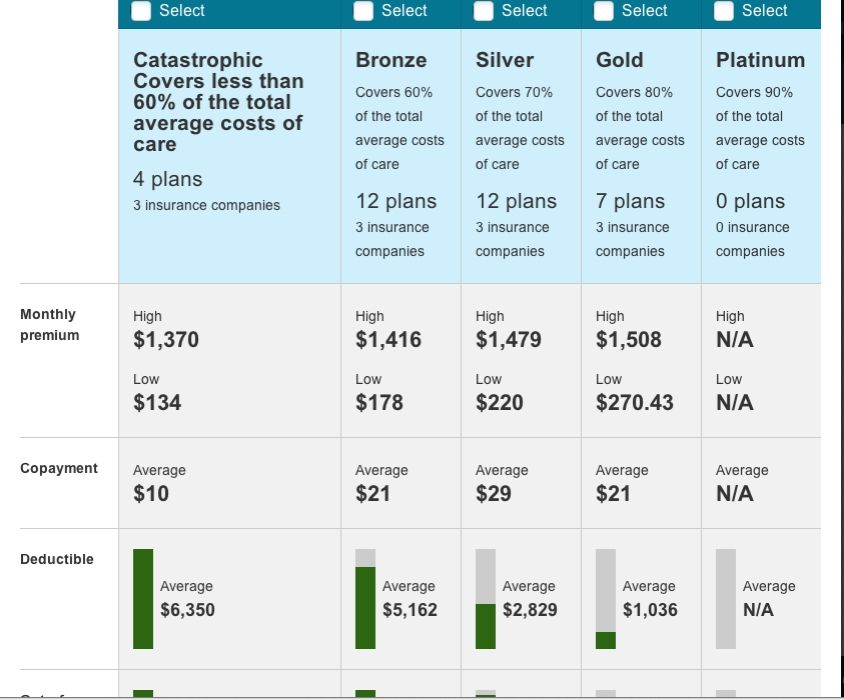

The lowest quoted BRONZE plan is $178/month. That's either 9.5% of his before tax take home pay or 10.8% of his after tax take home pay.

Either way - the monthly premium seems to be far out of range of what the guidelines for his income level is. I can't find those guidelines. I have to file an appeal for him and I can't find the substantiating information. We have his W2 handy.

When I worked his income through the Kaiser Family Foundation subsidy calculator, I was supposed to be able to find him a qualified SILVER plan for about $110/month. No dice on the Exchange.

I know this is wrong - meaning, the subsidy isn't being applied correctly. But I don't know what to do about it. He currently has NO health insurance.

Aren't they supposed to be attracting people like him? Young, health males, with the subsidized premium?

Trying not to panic here. But $178/month for him is NOT affordable. At all.

Thanks in advance.

UPDATE - I took the advice of several folks and created and entirely new account and went through the signup process to "select plans". The result is the same - premiums that are WAY out of line with my Son's income. Here's a screen shot of the results:

His employer DOES provide group health insurance, if you could call it that. They can't verify that it is ACA compliant yet, and the premium for a Silver equivalent is $376/month with high deductibles etc. I provided the insurance plan provider's contact information, phone number, email etc. as requested.

This is depressing.

UPDATE - 4:03pm Eastern. Ok. So I have a BIG update here. Let me re-lay out the facts:

1. Son is a waiter. Income between $22K and $23K before tax, and between $19K and $20K after tax. That works out to pre tax monthly income of $1866 and after tax monthly income of $1656.

2. Son's restaurant DOES provide health insurance. Lowest premium for catastrophic coverage is $279. That is 15% of his pre tax income - well exceeding the threshold.

3. Son does NOT take the insurance coverage. He can't afford it. He is uninsured.

Ok. So those are the details.

The first time through the ACA website, when asked if he had insurance I selected "no". When asked if he could obtain employer provided health insurance in 2014 I selected "yes". It IS available, although he would never take it because it costs too much.

THAT is why he wasn't getting a subsidy.

After creating another new account, and doing everything all over again, I selected "no" when asked if he had insurance. I also selected "no" when asked if he could obtain employer provided health insurance in 2014. Bingo - subsidy appeared, and a good silver PPO plan was available for $101/month.

I did NOT, however, go through with the enrollment process. I don't like the shady nature of the answer I gave to the second question. Strictly speaking, YES - he CAN get insurance through his employer. But he also CAN'T get it, because he can't afford it. I'm not comfortable answering that question as "no", and it requires a "no" answer to get the subsidy. So we'll have to go to a Navigator I guess. Ugh.

I don't mind going to a Navigator. But as I mentioned in another comment in the diary - what are the odds that another 20-something even figures out that answering "yes" to the availability of their unaffordable employer provided insurance is the issue? Do they just stop and pay the penalty when they get a premium of $178 returned? Or if they DO figure that out, do the go to the trouble of going to a Navigator to get it sorted out, or do they pay the penalty and just opt out?

I fear the latter - and I don't think that's an unfounded fear.

If you specify that you qualify for employer provided insurance, they should ask one more question: How much per month is the lowest cost plan available to you? Had that been in there, they would have known to apply the subsidy regardless and I could have been both honest and gotten a fair deal.