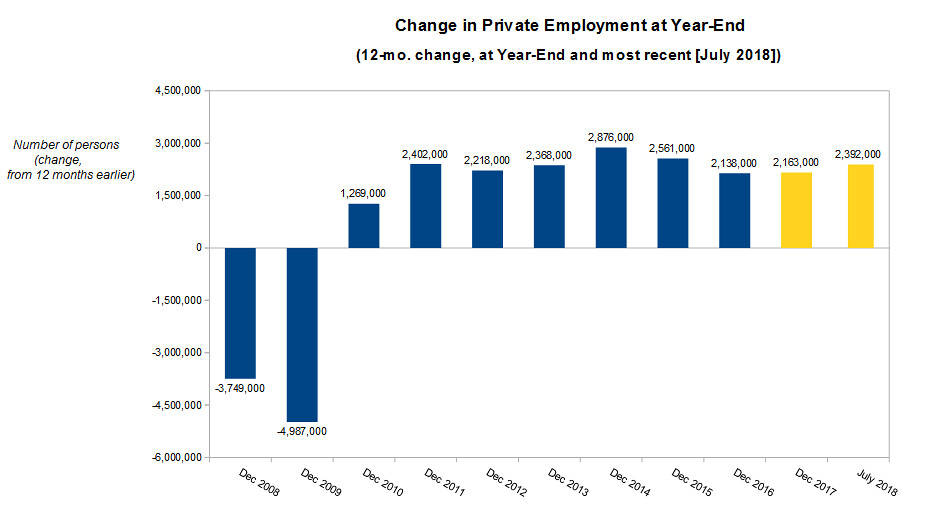

Here are the numbers of new jobs created.

The chart shows change from year ago.

12-month Change in Private Sector employment. Source data: Bureau of Labor Statistics

12-month Change in Private Sector employment. Source data: Bureau of Labor Statistics

During the Obama recovery, the average year-to-year gain in private sector jobs from December to December was 2,262,000 employees per year, or 2,427,000 per year after 2010 on average, from 2011 to 2016 (because 2010 had half as much gain as all the years that followed). At the end of Trump’s first year: the bump was 2,163,000 (12-month change Dec 2016 - Dec 2017).

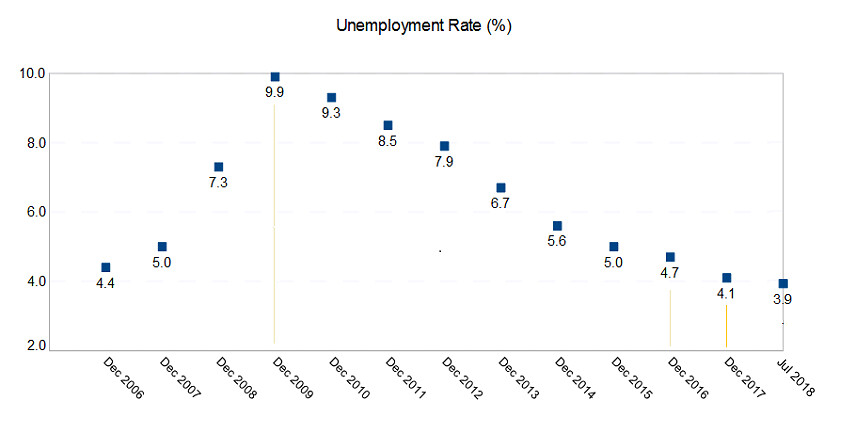

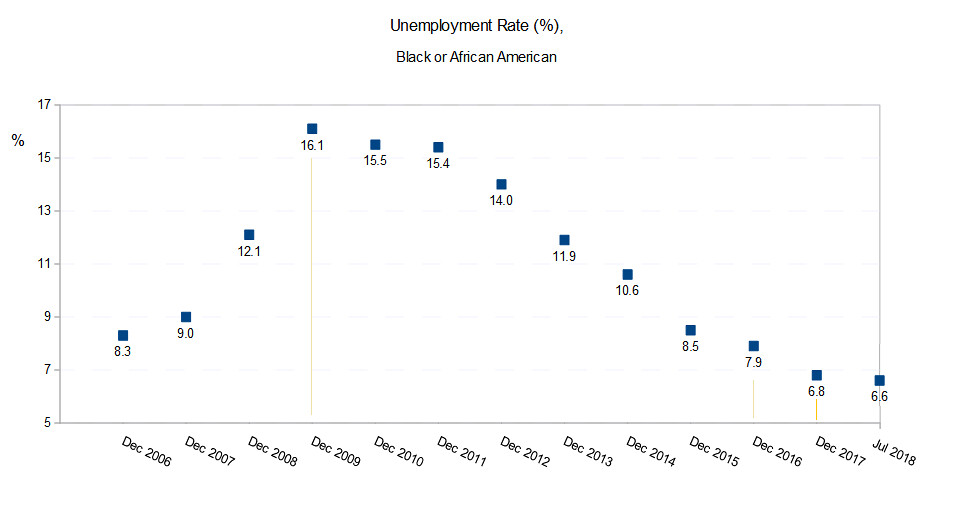

The employment/ unemployment charts above are ones I constructed, from year-end data, along with most recent month reported.

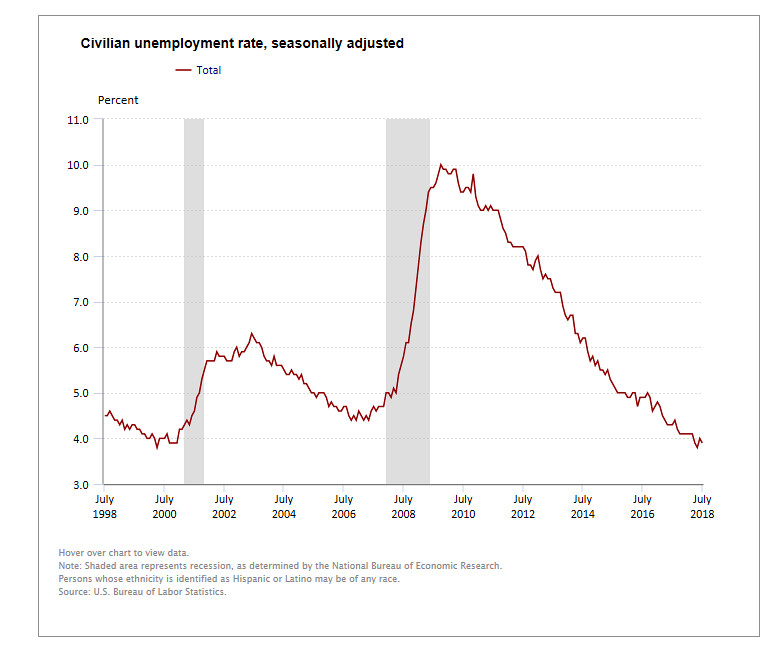

For simplicity, and going straight to the source, here are charts (of all months) from the web pages of the Bureau of Labor Statistics for monthly unemployment — seen at this page link (for total; and latino/Hispanic; black/African-American; Asian-American). The figures are accessed from the single link, then can just click on the each heading, e.g., for “Hispanic or Latino”, or for “Total”.

The 3.9% unemployment rate overall, which has been near an 18-year low, has followed the steep decline seen since 2010.

Total Civilian unemployment rate (%). BLS link: https://www.bls.gov/charts/employment-situation/civilian-unemployment-rate.htm#

Total Civilian unemployment rate (%). BLS link: https://www.bls.gov/charts/employment-situation/civilian-unemployment-rate.htm#

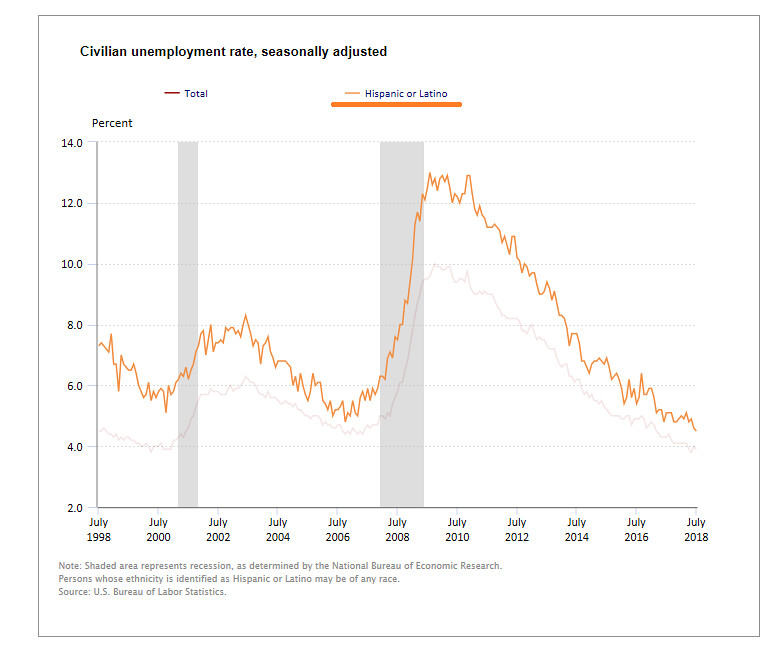

Here are the figures for the Hispanic labor force.

Unemployment rate (%), Hispanic/latino. Link: https://www.bls.gov/charts/employment-situation/civilian-unemployment-rate.htm#

Unemployment rate (%), Hispanic/latino. Link: https://www.bls.gov/charts/employment-situation/civilian-unemployment-rate.htm#

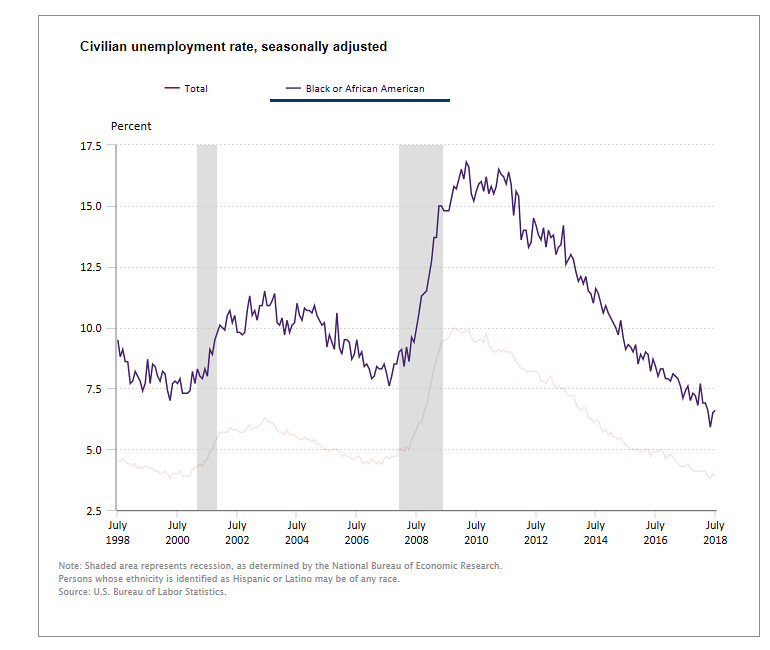

Here is the chart of the monthly unemployment rate for blacks/African-American.

Unemployment rate (%), black/African-American. BLS link: https://www.bls.gov/charts/employment-situation/civilian-unemployment-rate.htm#

Unemployment rate (%), black/African-American. BLS link: https://www.bls.gov/charts/employment-situation/civilian-unemployment-rate.htm#

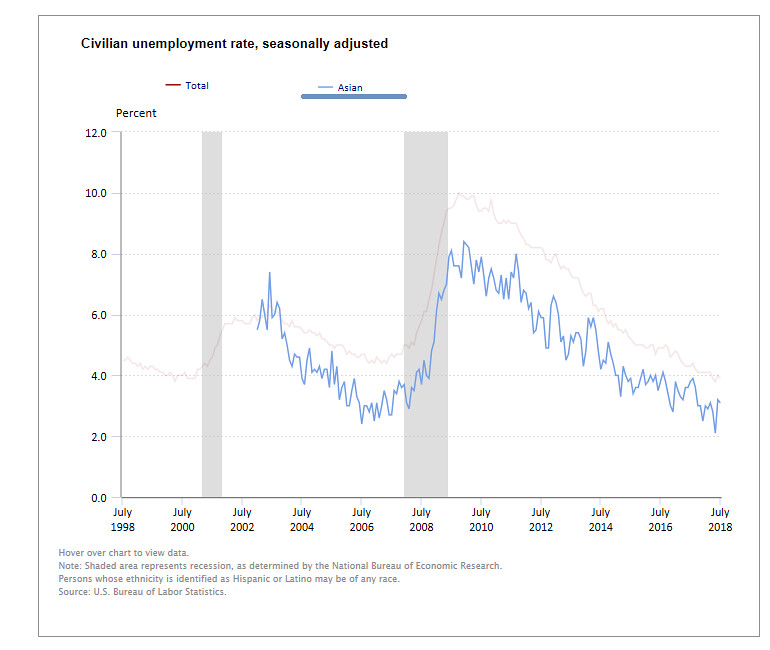

Here is the figure for unemployment of Asian-Americans, in blue.

Unemployment rate (%), Asian-Americans. BLS link: https://www.bls.gov/charts/employment-situation/civilian-unemployment-rate.htm#

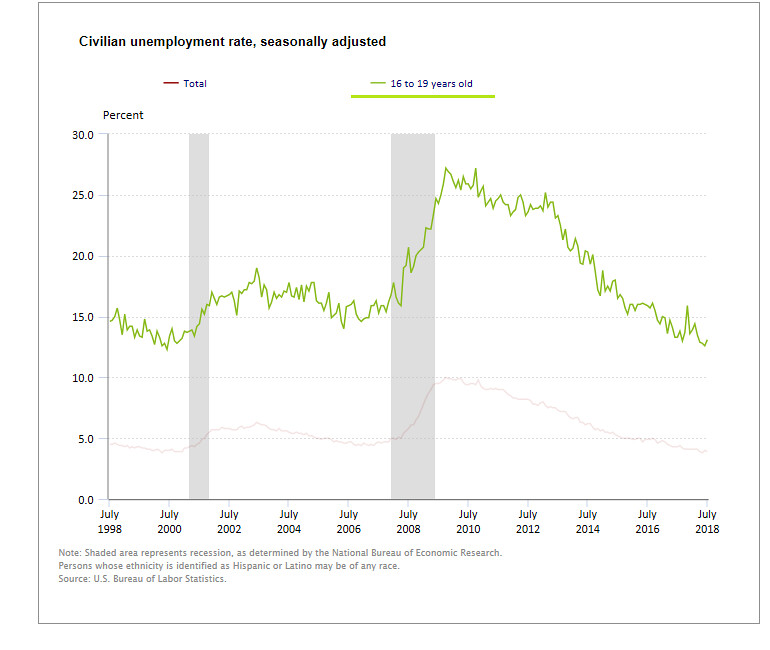

Here is the figure for youth unemployment, age 16-19 years old.

Unemployment rate (%), 16-19 years old. BLS link: https://www.bls.gov/charts/employment-situation/civilian-unemployment-rate.htm#

Unemployment rate (%), 16-19 years old. BLS link: https://www.bls.gov/charts/employment-situation/civilian-unemployment-rate.htm#

The US economy is beneficiary of an expansionary record that has solidified through the last 7 to 8 years.

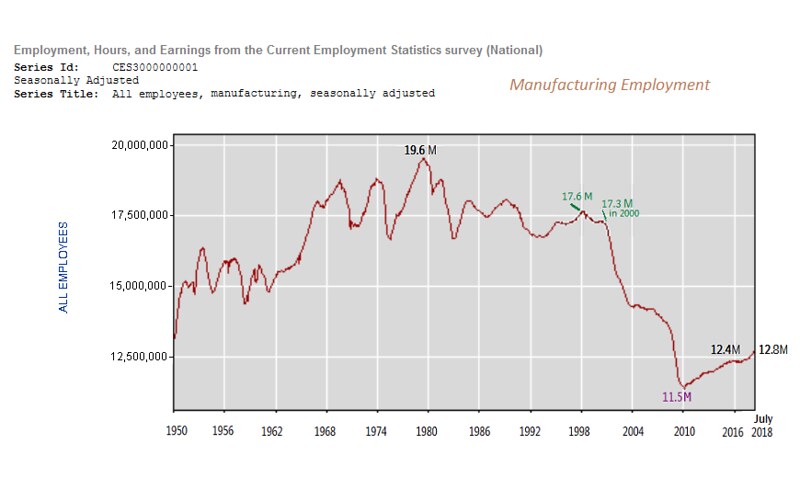

In the key Manufacturing sector, the Obama presidency turned around — from 2010 forward — the earlier enduring slippage in manufacturing jobs. See below.

Manufacturing employment, monthly, seasonally adjusted. Source: Bureau of Labor Statistics.

Manufacturing employment, monthly, seasonally adjusted. Source: Bureau of Labor Statistics.

(Link at BLS for monthly series [set the start year to 1950, and check the box for “include graphs”.)

A slide in blue-collar jobs, since 1980, accelerated in the decade from 2000 to 2010, when the economy gave up 6 million manufacturing positions. Since 2010, the U.S. succeeded in adding nearly 1 million jobs in manufacturing industries through 2016. Through 2016 it was the first sustained upturn in Mfg. jobs since the mid-1990s. Jobs in manufacturing grew to 12.4 million workers at the end of 2016, up from its bottom of 11.5 million in 2010. The upward trajectory of manufacturing jobs is continuing under Trump.

----

Also, note the deficit-yawning tax cut enacted for 2018 and years following will add a sizable ballooning forward risk to the outlook — because the tax cut timing was pro-cyclical and front loaded, and it is adding stimulus right in the midst of a mature business expansion. That is, the tax cut amplifies the expansion at a late stage when the recovery is mature, long-in-the tooth (eight years old, since 2010).

However, tax and spending policy are meant to be counter-cyclical, particularly when the economic growth reverses and the economy contracts. That’s the time when fiscal stimulus (tax cuts or spending increases) will be needed. If we’ve already blown the deficit and tax cuts with a pro-cyclical economic move when the economy is chugging along, then we’ll have no fiscal policy tool to right the economy when it heads into a downturn and seriously tanks.

Therefore, any tax-cut engineered economic burst that may occur may be short-sighted and self-limiting.

On top of that, Trump’s vindictive restrictive immigration policy will literally wall off social security for future generations.

Consider: a limited-immigration scenario shortens slightly the actuarial life of the SS trust fund compared to baseline — because immigrant families are younger than the overall working-age population, on average, and have higher fertility rates than do second- and third-generation households. Social security always depends in part on the next generations funding the last, and in part on the taxes workers have always paid in to the fund.

The current Trump economic program is a feel-good-in-2018, pay-for-it-later strategy. On the heels of the salutary economic momentum that Trump inherited, the turn in 2018 to the debt-embracing tax policy that Congress and Trump enacted, just to goose a mature economic expansion, is high risk to undercut our future prosperity.