A number of symbolic levels have been reached or breached in recent days on the commodity markets, with many predicting more to come (see below), but a number of voices are now fighting back and saying that this is not so significant, unlikely to last, or both. Let's take a look at their arguments.

Via the

Financial Times

IPE June Brent fell 42 cents to $69.44 a gallon [sic] while Nymex May West Texas Intermediate eased 51 cents to $68.11 in electronic trading.

(...)

Gold prices moved lower after flirting with $600 level on Wednesday. Gold traded at $596.20 a troy ounce from New York's late quote of $597.50/$598.30 amid profit taking ahead of the Easter holiday.

(...)

Other precious metals also traded lower with silver at $12.62 from New York's late quote of $12.82/$12.85 while platinum eased to $1,074 a troy ounce from New York's late quote of $1,086.

Copper eased back to $6,090 a tonne for three-month delivery from the record $6,105 reached in the previous session while zinc traded at $2,975 from the record $3,005 a tonne reached on Wednesday.

Oil is up on a combination of geopolitical worries (with the insurgency in Nigeria and the tensions surrounding Iran bearing most on the market, in a context of ever increasing demand and tight supply:

IEA says Opec must lift output to meet demand

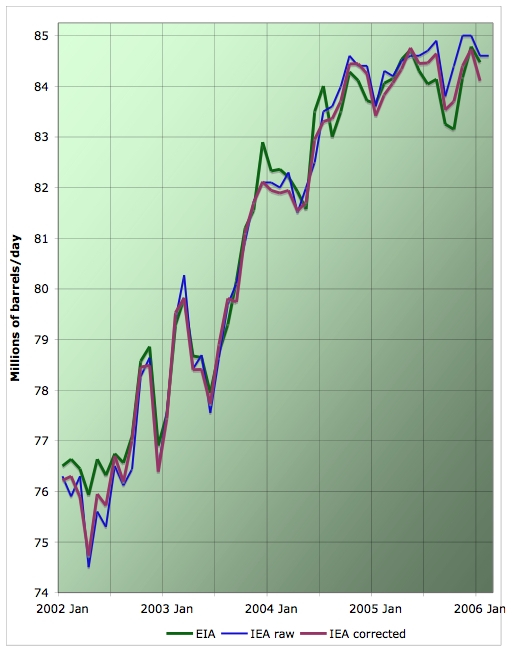

Demand for oil has tested the Organisation of the Petroleum Exporting countries to the limit, the International Energy Agency said yesterday.

Opec will have to increase output this year to meet global oil demand and make up the shortfall from Russia, Nigeria and from other, non-Opec, producers, the IEA said.

(...)

Opec, which accounts for 40 per cent of the world's oil supplies, is not the only producer struggling to lift output as demand rises, however. The IEA slightly reduced its forecast for non-Opec supply growth this year owing to weather-related outages in the US, Mexico, Russia and the North Sea, while mechanical problems, start-up delays and strikes afflicted output in South America, Canada, Chad and Sudan.

(...)

The IEA highlighted concern over shortages in drilling equipment, qualified staff and service company capacity that might impede capacity growth over the "next two to three years".

There was some respite on the demand side; the IEA revised down its global demand growth to 1.47m b/d from 1.49m b/d, which still represents an acceleration in demand growth from the 1.05 b/d increase last year.

That last sentence is something that needs to be repeated again and again: despite the record high prices, demand is increasing faster than before. So, not only high prices are not slowing demand, they are not even slowing demand growth...

Which means that, when supply gets really tight, something that seems pretty likely to happen from the warnings we get on all sides (including from the IEA as stated just above), the prices required to get demand to ajust to supply (instead of supply to demand) will need to be considerably higher than today.

Rising Commodity Prices Impede Further Oil Exploration

PARIS - Soaring commodity and raw material prices are increasing the cost of oil and gas projects by up to three times, Organization of Petroleum Exporting Countries ministers said Friday.

Although current high oil prices may be helping to drive much-needed crude investment, the rising cost of construction projects could curtail new energy production development, they warn.

Addressing delegates at Petrostrategies annual oil summit in Paris, Qatari Oil Minister Abdullah al Attiyah said: "Our costs have tripled from two years ago, due to high (commodity) prices. And its not just that, it is also contractors who have tripled their prices."

And, as a side note, not only is our oil increasingly coming from unstable or hostile countries, it is also less and less under the control of the Western oil majors, which have trouble renewing their resources as they are kept out of the main oil producing countries:

Finding new oil fields is getting harder, but not impossible

WITH the price of oil hovering near $70 a barrel, oil companies cannot pump the stuff fast enough. But in order to keep pumping in the long run, they also need to keep finding it. Unfortunately, most big Western oil firms are getting worse at exploration. Neil McMahon, an analyst at Sanford Bernstein, calculates that such companies had an average reserve-replacement ratio of 129% over the past five years--meaning that they found 29% more oil and gas than they pumped. But last year the ratio fell to 114%.

These figures understate the problem, since they include not only newly discovered oil, but also oil acquired through takeovers and purchases--"drilling in the canyons of Wall Street", as the old industry hands call it. Last year, for example, Chevron bought Unocal, prompting an apparent rise in its reserves, while several other American oil companies bought stakes in oil fields in Libya. Strip out such additions, according to Sanford Bernstein, and last year's average reserve replacement falls to a meagre 87%: overall, reserves are shrinking. The numbers get even bleaker if you are interested in new discoveries, as opposed to the more efficient extraction from existing fields. Wood Mackenzie, a consultancy, estimates that the ratio then falls below 50%--one reason why the industry is increasingly looking to the technology of enhanced extraction.

Even those companies with relatively high ratios are often relying on just one or two bumper additions to their books. Exxon Mobil's overall reserve replacement, for example, has averaged 114% over the past decade. But in 2004 and 2005 the vast majority of its new reserves came from just one field in Qatar. Exxon did not discover the field itself--it is developing it with Qatar's state-owned oil firm.

And that's not just for oil. All commodities are going up, pushed by a combination of strong world demand (with a significant contribution by China), tight supplies, a strange reticence by producers to invest in new capacity, and increasing production costs.

Despite this, and big announcements that prices are set to go higher (for instance, gold could soon reach 850$/oz according to a consultancy), a number of bearish voices have sounded a loud warning in recent days. I'll take two articles, from the Financial Times and the Economist.

It's unsustainable

Bears drowned out by chorus of bulls (Financail Times, April 11)

Analysts forecasting an imminent bursting of a market bubble have had to watch as prices for a host of commodities surge to fresh peaks, seemingly on a daily basis. But as prices ascend, so do the risks of a correction that could send shock waves through financial markets. "Current high prices are unsustainable," says Simon Hayley, senior international economist at Capital Economics.

Here is a guide to some of the potential triggers most commonly cited for a correction:

? Higher-than-expected rises in interest rates in the US, Europe and Japan may reduce liquidity in financial markets, which would not only affect commodities, but equities too.

? Signs of slowing economic growth in the US. (...)

? China has been a big driver of increased demand for commodities as its economy has continued to expand. But growth may slow, (...)

? An easing of demand from investors for commodities. Funds flows from investors have driven up demand for commodities. But that demand is prone to reversal.

? High prices could see cheaper alternatives substituted for expensive commodities. This is one fear of many producers. A classic example is to substitute plastic pipes for copper equivalents.

One last trigger for a correction could be a capitulation of the bears. Markets have had a long history of turning just when every bear turns positive or every bull becomes negative. In the current chorus of bulls calling commodity prices higher, bears seem thin on the ground.

It's not a big deal anyway

A new set of ties binds higher raw-material prices and bond yields--for now

AT FIRST glance, it has the hallmarks of a classic inflation scare. In the past week commodity prices--from oil to orange juice, silver to sugar--have reached eye-popping levels. (...) Meanwhile, long-term nominal bond yields in America and elsewhere have risen to levels not seen in more than a year. On April 7th the yield on America's 30-year long bond climbed the 5% barrier, sending a flutter of fear through global markets. (...)

The rising costs of money and raw materials took leading roles in that economic horror movie, the 1970s, when inflation ran amok and growth froze. (...)

There are plenty of reasons why hot commodity prices have not caused too many worries about inflation. One is that markets are confident that central banks will act to contain inflationary pressures. A second is that cheap Chinese exports have held down global prices. Another is that manufacturing's share of the world economy is declining; another is that the intensity with which industry uses raw materials is also shrinking--thinner steel in cars, for example--so that commodities' importance to inflation has diminished. And in real terms commodity prices are still well short of their 1970s peak (see chart 2). They have been on a downward trend since the 19th century, punctuated only by wars and other supply shocks: producers have generally coped with periods of surging demand, and probably will do so this time.

(...)

But whereas in the past higher commodity prices spelled bad news for bond markets, now the shoe may be on the other foot. Few expect that higher long-term interest rates will halt global economic growth, but they probably will have a dampening effect. That in turn should restrain demand for commodities.

So, what should we think? There are basically three messages in there:

- the first one is simply the usual "the markets will set things right": increasing prices will lead to higher supply and lower demand and prices will cool down. The interesting twist is that none of these two articles emphasise supply growth - they don't even mention it. (And, as discussed in my earlier diary on commodities, producers are unwilling and/or uanble to invest). All the adjustment is expected to come from the demand side, as growth slows in the US and China (not good news, by the way), and alternatives are found to the newly expensive commodities.

The big problem with that argument is that, as we've seen for oil above, demand seems pretty damn unelastic, and much higher prices will be required for the adjustment to come from that side. Everybody points out to the easy ways we ca nsave on energy, metals, etc... but so far IT IS NOT HAPPENING.

- the second argument is more financial in nature. It basically amounts to saying that speculators will stop pushing the market up as returns get lower compared to safer alternatives in a context of rising interest rates (and gently slowing growth). i.e. the "commodity bubble cannot be bigger than the financial bubble, and as the financial bubble is gently deflating, all will be fine as well on the commodity front;

- the final argument is that commodities don't really matter anymore. We don't build stuff anymore, we're more "efficient" with our inputs, and prices are not that high in real terms, so there's no need to worry.

I personally think this is naive, but I'll open myself, as usual, to criticism that I have been crying wolf for a while and growth is still around. I think that the financial bubble will burst, not deflate, and that we will have a nasty economic crisis on our hands - and yet I don't think that'll be enough to slow down commodity price hikes. Demand for commodities is unelastic, and supply is, quite simply, struggling (via the Oil Drum).

What say, you, bears? Do you really expect demand destruction?