U.S. existing home sales slipped for a sixth straight month in September, a real estate group said on Wednesday, underscoring a weak spot in the economy that some analysts think could lead to lower interest rates next year.

Just hours before an announcement from the Federal Reserve that it was holding the federal funds rate steady, the National Association of Realtors said home resales slowed to an annual rate of 6.18 million from a 6.30 million pace in August.

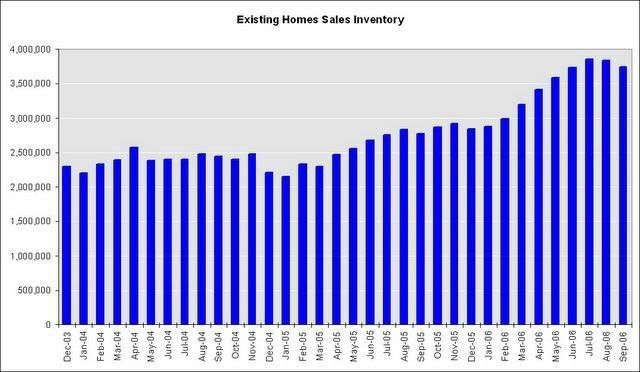

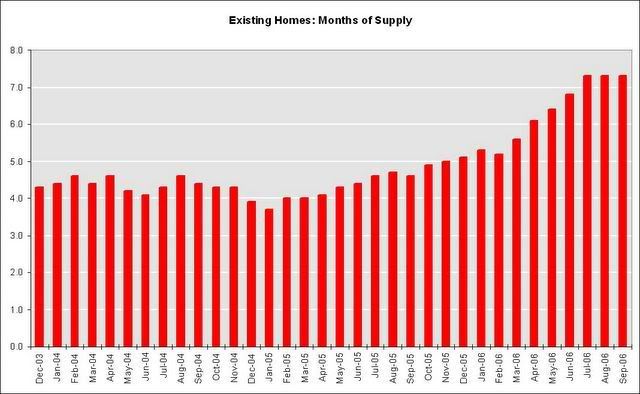

The inventory of homes for sale fell 2.4 percent, or 93,000 units, to 3.75 million, its second consecutive drop, although the number of unsold homes on the market remained at a relatively high 7.3 months' supply.

The median sales price fell 2.2 percent to $220,000 from a year earlier. Prices in August had fallen for the first time in 11 years.

OK - so here are some pictures to see where existing home sales are. These come from the blog

Calculated Risk which has done an excellent job of covering the housing market.

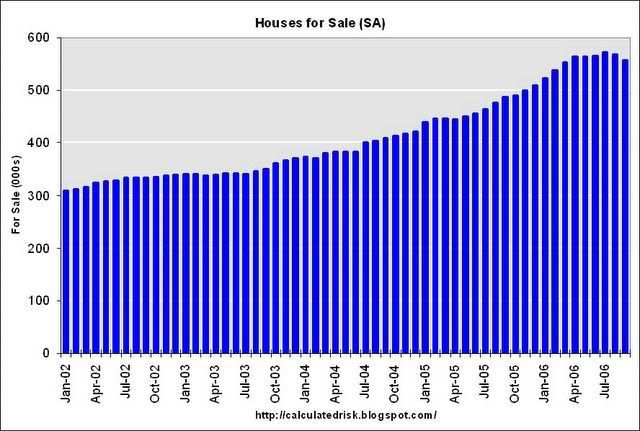

Notice that while inventory has dropped for the last two months, it is still at very high levels.

Also notice that the months available for sale have changed very little:

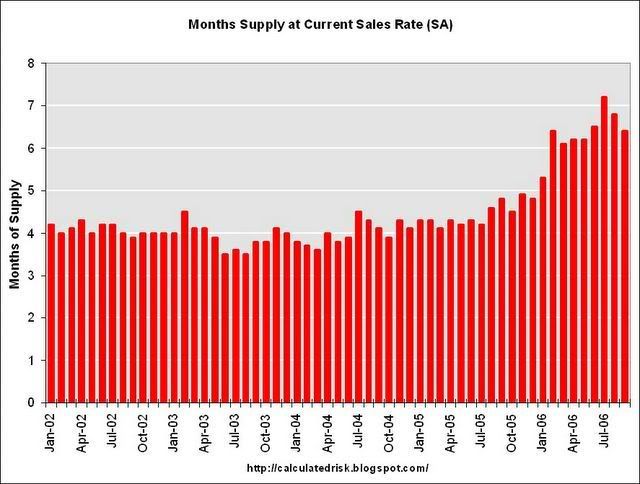

Short version - there is still a ton of inventory on the market. While there was some happy "we're near bottom" or "things are bottoming out" talk regarding this figure, the incredibly high levels of inventory tell a different story. It's going to take more than a few months to clear this inventory.

Finally, remember the existing home sales market is about 6 times larger than the new homes market.

New Home Sales

New-home sales in the U.S. unexpectedly rose for a second month in September as prices declined by the most since 1970.

Purchases increased 5.3 percent to an annual pace of 1.075 million during the month from a 1.021 million rate in August, the Commerce Department said today in Washington. The median price of a new home dropped 9.7 percent from a year earlier.

The reports suggests that builder incentives, lower mortgage rates, and falling prices will keep this year's housing slowdown from deepening. It also signals the Federal Reserve, which kept interest rates unchanged for a third month yesterday, is successfully managing an economic slowdown that it hopes will stifle inflation.

Let's break this information down a bit. First, it is good news that new home sales rose. However, there is a biiiiiiiig caveat to this figure.

U.S. homebuilders slashed prices at the fastest pace in 36 years in September, boosting sales to the highest level in three months, the government said Thursday.

Here's a chart of the price action from CBSMarketwatch:

More importantly

Home builders have piled on incentives, including vacations and new cars, to sell homes. Such incentives are not subtracted from the sales price reported to the government.

Let's pit these points together. New home sales rose, but homebuilders had to slash prices to get that increase. In addition, the sales price figures are most likely optimistic because about 75% of builders are using incentives which aren't counted in the official price figures. There's a difference between aggressive pricing and a fire sale. This looks more like a fire sale.

And while the months available of new home inventory is decreasing:

The absolute level (the total number of new homes available for sale) is still at very high levels:

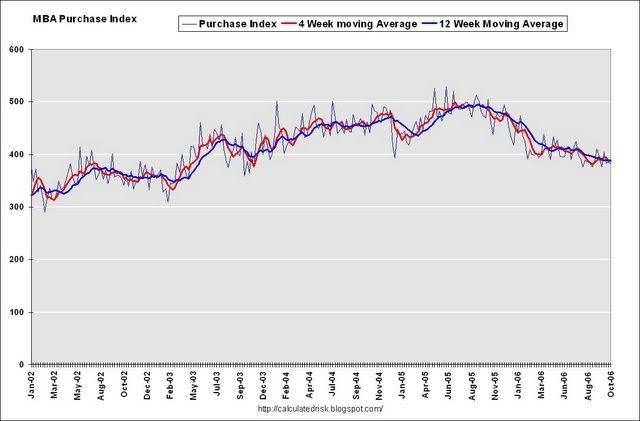

And those high inventory levels are occurring when mortgage activity is dropping. Notice how the MBA purchase index still has a downward slope. In addition, current levels are closer to 2004 purchase levels.

That means housing firms are faced with a terrible choice. They've already used massive incentives and price cuts to get the fastest price drop in 36 years. Now they can continue this level of discounting further eating into their profits, or they can return to the older higher prices and further depress their sales. That's not a great choice.

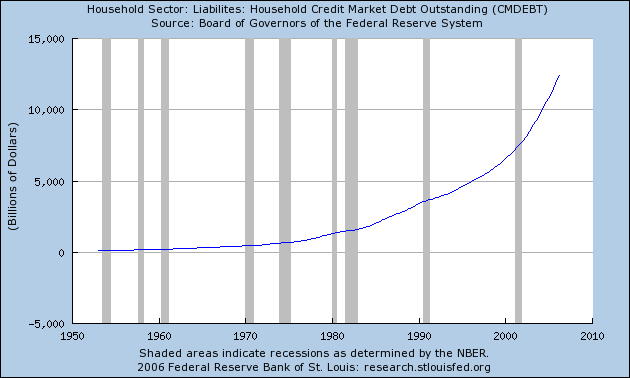

And what nobody has answered is this question: who's going to buy these houses? Despite the price drops, home affordability is incredibly low and the amount of debt in the US economy is already at incredibly high levels - over 90% of GDP and over 120% of disposable income.

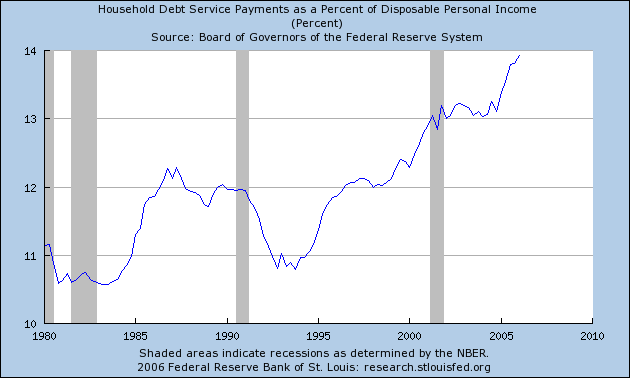

And households are already paying a record amount of their income for debt service:

While there is a debate going on among economists, San Francisco Federal Reserve President Janet Yellen has it right:

....a significant buildup of home inventory implies that permits and starts may continue to fall, and the market may not recover for several years