There's been a ton of action in the markets and mortgage industry over the last few days. The news is coming at a literal "fast and furious pace". Below are some things I wrote on my blog. All of the market analysis is as of the close of the markets on Tuesday.

Yesterday's Intra-Day Chart

Here are today's charts in the following order:

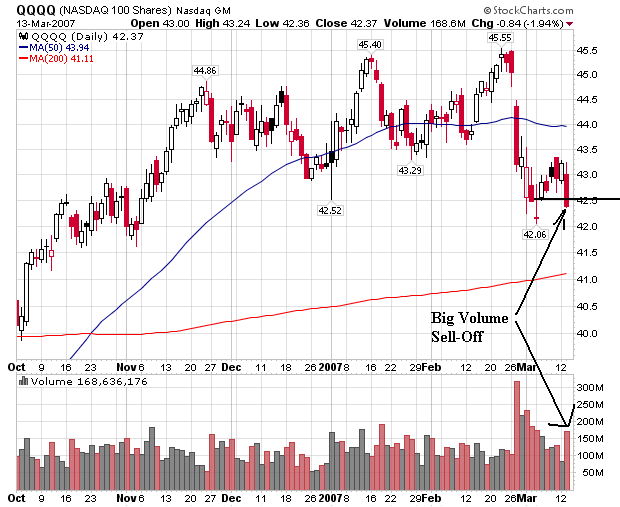

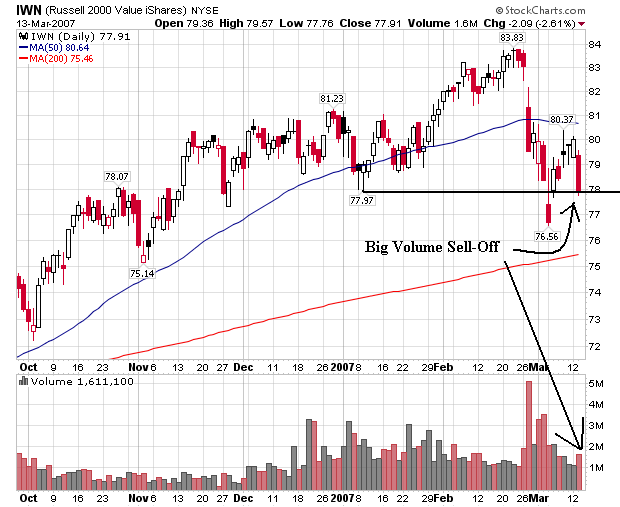

SPY, QQQQ, IWN

The markets first tumbled a bit after 11 EST. Notice the three really strong downward bars on strong volume. This indicates there were a ton of sellers and they were in complete control.

About 12:30 the IWNs sold-off. Remember the Russell 2000 have performed slightly better for the last few sessions, meaning there were more profits to book.

All the averages tumbled again at 1300 and the QQQQs and SPYs had a volume spike at this time. Again -- a ton of sellers enter the market and they are in complete control of all the action.

Notice how all the averages died at the end on extremely heavy volume. This was literally a, "Katy bar the door" moment in the market when everybody wanted to get out.

Also note the markets continued to trade down throughout the day and closed near session lows. These are all bearish signs. The continual downward trend indicates the market could not find a bottom during trading. Closing near a low, on a sell-off on very high volume indicates people were dumping shares. That means they are nervous about what news might come out tonight and tomorrow morning.

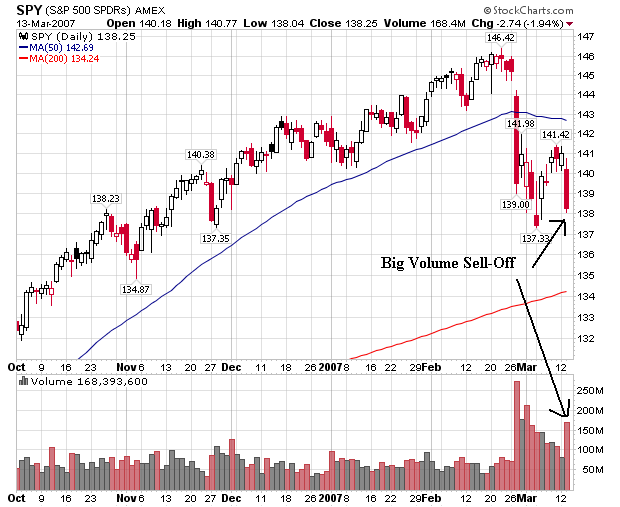

The Daily Charts

Let's go to the daily chart to see what today did to the long-term charts. Here's the SPY, QQQ and IWN to see what happened

Several days ago I wrote the recent rally after the sell-off was suspect because of declining volume, but the declining volume may itself be suspect because it was coming down from a really high level. Well -- now we have confirmation. The rally was suspect.

You'll notice the same wording on each chart: big volume sell-off. Simply put, there were a ton of sellers in the market today, and they were looking to get out. They were willing to take a lower price to get out. That's one of the prime reasons for the drop.

Notice that technically, all the averages have a touch of breathing room -- but not much. Just eyeballing the charts it looks like about 1% on the downside. Another bad day like today and the markets will be looking at a technical break-out on the downside.

Mortgage Market

First -- as of today, 36 lenders have either gone bankrupt, sold their assets or closed their doors.

This statement is from the largest servicer of subprime mortgages, Countrywide Mortgage:

Countrywide Financial Corp. (CFC.N: Quote, Profile, Research) Chief Executive Angelo Mozilo said on Tuesday the U.S. mortgage sector is entering a "liquidity crisis," but that investors and speculators are overreacting by punishing healthier lenders as well as marginal ones.

"This is now becoming a liquidity crisis," and "it's going to get uglier," Mozilo said on CNBC television.

Mozilo said the winnowing out will be "great" for Countrywide, the largest U.S. mortgage lender, which might pick up market share.

And the bad news continues coming:

U.S. subprime borrowers fell behind on their mortgages at the highest rate in four years in the fourth quarter and foreclosures begun on all types of home loans rose to an all-time high, the Mortgage Bankers Association said.

The share of subprime borrowers making late payments rose to 13.33 percent from 12.56 percent in the third quarter, the Washington-based group said in a report today. Foreclosures also rose on loans to borrowers with the best credit ratings, a sign of broader trouble in the mortgage market.

Lenders loosened credit standards on prime loans with the lowest interest rates last year as they competed for a shrinking pool of borrowers. Widespread defaults in the $6 trillion mortgage-backed securities market could push the U.S. economy into recession, said economist Gary Shilling.

``The worst is really yet to come,'' said Shilling, president of A. Gary Shilling & Co. Inc., a Springfield, New Jersey-based economic forecasting company. ``To keep the game going last year lenders simply lowered their credit standards. As a result, you've had a tremendous number of these mortgages that have gone bad.''

The economy isn't even in a recession, and delinquencies are rising at very high rates. That means if we do hit a recession, it's going to get really ugly.

Not only are delinquencies increasing at a high rate, but foreclosures are at record highs:

Many more U.S. homeowners were unable to keep up with their mortgage payments in the fourth quarter, the Mortgage Bankers Association said Tuesday, with the rate of homes entering the foreclosure process hitting a record 0.54% and the delinquency rate on U.S. home loans leaping to 4.95% from 4.67% three months earlier.

"Although the U.S. economy and job market remain solid, the housing market continued to decelerate in the fourth quarter of 2006. Nationally, house prices increased at a slower rate and the pace of sales and construction activity continued to slow," said Doug Duncan, MBA's chief economist.

.....

The foreclosure inventory rate increased to a seasonally adjusted 0.5% from 0.44% for prime loans and to 4.53% from 3.86% for subprime loans. At 0.54%, the rate of homes entering the foreclosure process breached the cyclical peak set in the second quarter of 2002, after the recession, Duncan said.

Duncan said the jump in delinquencies was expected given the housing-market slowdown and that the shakeout in subprime lending should restore equilibrium to that market shortly.

"One of the impacts of (home-price) declines, of which some local markets clearly are registering declines today, is that it's an evaporation of equity or potential equity. And to the extent that a borrower gets in trouble in making their payments, it reduces their options for recovering from that," Duncan said during a conference call with reporters.

Again note we're in the middle of an expansion, although the pace of the expansion is slowing. That means if we hit a recession, we're in for a world of hurt.

And all of this is just the tip of the iceberg according to Fed President Bies:

The nation's banks are just beginning to feel the pain of defaults on risky mortgages they made at low introductory rates when housing prices were soaring, U.S. Federal Reserve Governor Susan Bies said.

Bies, who has been the Fed's top banking policy official in her tenure at the U.S. central bank, said today banks are likely to see more missed payments and foreclosures as consumers with weak credit histories begin to face higher monthly mortgage payments.

``What's happening is the front end of this wave of teaser- rate loans that are coming into full pricing,'' Bies said at a risk-management forum in Charlotte, North Carolina. ``So what we're seeing in this narrow segment is the beginning of the wave. This is not the end, this is the beginning.''

Bies's comments reflect growing attention among bank regulators to the turmoil in the so-called subprime mortgage market and its impact on consumers and U.S. lenders. Many subprime borrowers face large prepayment penalties they can't afford, and they can't refinance or sell their homes, she said.

When a Federal Reserve Banker says "it's the beginning of a wave", you really should listen.

In case you were wondering about the last time we had a problem in the housing market:

If this slump follows the same pattern as the last one, in 1991, it will persist for at least another year and may fuel a recession. New-home sales declined 45 percent from July 1989 to January 1991 and about 1 percent of all U.S. jobs, or 1.1 million, were lost in that recession, said Robert Kleinhenz, deputy chief economist of the California Association of Realtors.

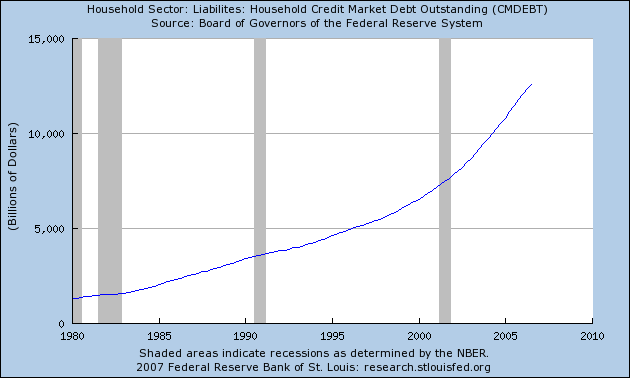

The last 6 years of economic growth has been fueled by easy credit. While wages have barely increased over inflation (or should I say gas prices), total household debt has increased at an alarming rate. Here's a chart from the St Louis Fed of total household debt outstanding:

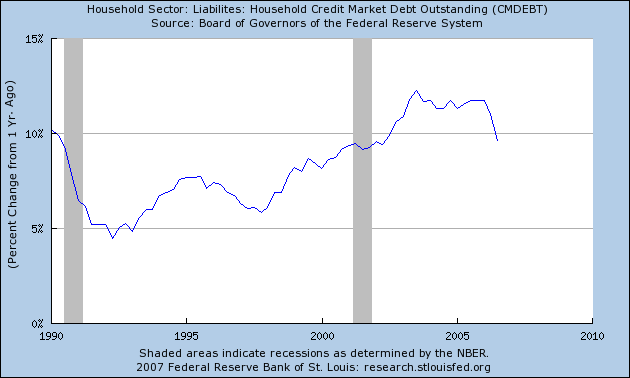

Here's a year over year percentage change in the same chart.

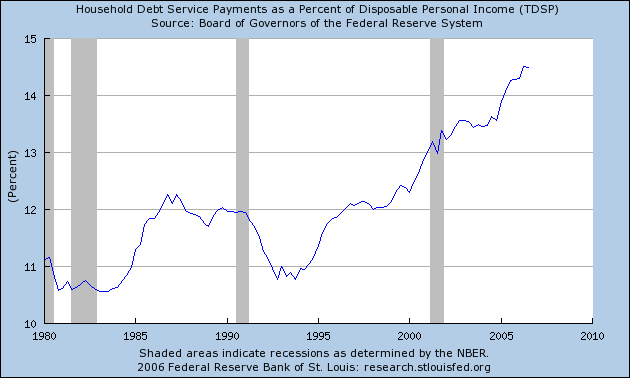

And finally, here's a total debt payments as a percentage of disposable income:

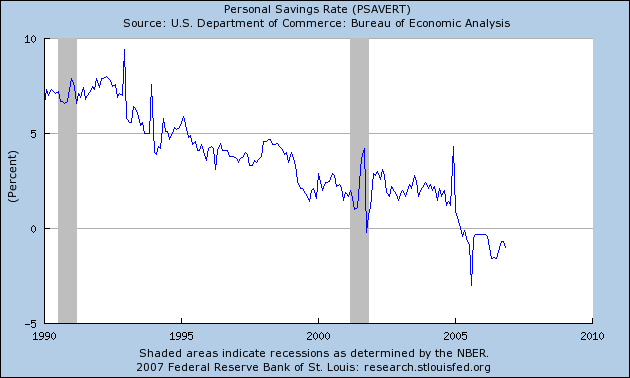

And in case you were wondering, the US savings rate is negative and has been for awhile. That means people aren't ready for a financial shock if it comes:

All of the debt in the system is starting to take a toll as easy credit terms and low interest rates expanded credit to everyone wit a pulse. Now we're discovering that all those people with pulses may not have been the best credit risk.

Both of these events -- the mortgage industry problems and yesterday's sell-off -- are inter-related. Concerns about the mortgage business are running deep. This is especially so considering the news we've have as of late, all of which has been extremely negative. Given the economy is slowing, don't expect a let-up in this type of news anytime soon.

Update [2007-3-14 8:38:23 by bonddad]:: Below, New Deal Democrat gives an excellent, shorter version of the points made above. Here is a link to the comment with the links he cites:

There are actually 2 related but different panics going on. First is the Housing Panic, as to which:

Foreclosures are at a 20 year high already. A more up-to-date, but short term graph showing that foreclosures are trending even higher, can be found here.

And it will only get worse as the number and $volume of ARM resets explodes now and for the next 5 years, as shown by Exhibit 42 on Russ Wiinter's blog post yesterday.

The loss of the subprime mortgage buyer will ripple through the housing market.

In short, expect more inventory, moe distressed inventory, and fewer qualified buyers for housing.

The second is the Lending Panic, as to which:

There is more leverage in the stock market than in any time in the last 50 years, and less cash reserves in mutual funds to fund redemptions than ever.

The Countrywide Financil CEO says there is a liquidity crisis.

Next most likely to be hit are the

Senator Dodd proposes a "helicopter drop" bailout.

Let's look at who his major campaign contributors are.

This may explain the coincidence that the next bagholders in line (holding the bad debts) when places like New Century go bankrupt, are the very same investment houses.

My summary: at this point, we know the Housing panic will get worse. We don't know how far the Lending panic will spread. What we do know, as I keep hammering away at, is that we are more at risk for an old fashioned "bust" or "panic" than we have been at any time since the great depression.