All in all, we have a terrible quarter for financial companies:

In all, at least nine major banks have warned or announced they will take write-downs, set aside funds or take charges of roughly $21.8 billion related to subprime lending, the credit markets and leveraged-buyout debt.

From CBS.Marketwatch:

Merrill Lynch & Co. became the latest and biggest casualty of the credit crisis Friday, warning that it will write down nearly $5.5 billion and report a loss when it announces third-quarter financial results.

Most of the write-down, $4.5 billion, comes as the firm marks to market the value of collateralized debt obligations, or CDOs, and subprime mortgages.

Merrill is hardly alone in this matter.

Reinforcing views that the plight of the financial sector is closely tied to upcoming moves by the Fed on interest rates, Washington Mutual Inc. (WM:

Washington Mutual Incsaid Friday that it expects third-quarter earnings to drop by about 75%.

The Seattle-based lender credited the drop-off largely to factors related to weakening conditions in the nation's housing market.

"It's not a complete surprise since about three quarters of their loan portfolio is tied to mortgages," said Fred Cannon, analyst at Keefe Bruyette & Woods. "Just like most other lenders, they're facing extreme pressure from the meltdown in mortgage markets."

From CNN:

Bank of America and JPMorgan Chase are thought to be on the verge of announcing combined losses of $3 billion from mortgage-backed securities and leveraged loans when they report third-quarter earnings this month, according to a news report today.

JPMorgan (Charts, Fortune 500) is expected to announce losses on leveraged loans of $1.4 billion, Sanford Bernstein analyst Howard Mason said in the report. He also anticipates it will suffer an additional $700 million in writedowns on mortgages and mortgage-backed securities, said FT.

Bank of America (Charts, Fortune 500) is expected to see around $700 million in leveraged loan losses and mortgage writedowns of $300 million.

So -- what's going on with these financial companies? They are writing down the value of mortgage related loans and bonds along with collateralized debt obligations and collateralized loan obligations that are on their books. The bottom line is the mortgage market problems are starting to filter out into the economy at large.

The question now becomes, "is this a one time event, or the beginning of a long term trend in the financial companies?"

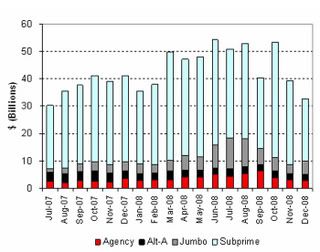

There is no firm answer to that. However, I don't think so. First, here is a chart from the blog Calculated Risk that shows the rate of delinquencies for various years of subprime mortgage loans. Notice that 2007 has a huge upward trajectory.

Also note that according to the following two charts, there are a ton of ARMS resets coming down the pike over the next 12-18 months. The first chart is from the Bank of America and the second is from CSFB. Both charts from from Calculated Risk (see link above).

Finally, Herb Greenberg at CBS.Marketwatch has some very astute observations about the way Citigroup announced its earnings and what was and wasn't mentioned in the call.

First, among things not said at Citigroup: There was no mention of 2008 and no explanation of the word "normal," and a spokeswoman declined to elaborate. However, normal quarterly earnings for Citigroup, other than an unusually strong second quarter, have been about $1 a share, give or take a few pennies. Analysts are expecting earnings of $1.10 a share in the fourth quarter. That is a penny below what they were anticipating for the third quarter, an estimate which has since been revised down to 47 cents a share.

Next, despite the timing, the guillotine that Citigroup took to its earnings guidance wasn't just because of the mortgage mess. The company blamed it largely on $5.9 billion in unexpected losses and charges. A little more than half were from such things as subprime-mortgage-backed securities and "fixed income credit trading" - the kind of hits you would expect from a credit and mortgage meltdown.

But the rest reflected increases in consumer-credit costs in the form of higher losses and reserves on the likes of home-equity loans, mortgages and credit cards. This isn't a new issue for Citigroup, which a quarter ago warned that consumer-credit costs would be rising in the third quarter. The company, however, didn't say by how much. In other words, mortgage mess or no mortgage mess, earnings still might have missed expectations. The spokeswoman declined to comment.

Then there was the conference call, or lack thereof. After making its announcement, rather than holding a call with investors, Citigroup offered up a brief prerecorded message, with more detail, from Prince and Chief Financial Officer Gary Crittenden. That is one way to avoid answering tough questions. Writing on Deal Journal, a blog on WSJ.com, The Wall Street Journal's Dennis Berman said it was "almost like a Politburo shunning the world around it." The spokeswoman says the company went the prerecorded route "because we wanted to get information out quickly and efficiently."

That brings up something else: The release of earnings, and a live question-and-answer session with analysts, has been pushed up to early on the morning of Monday, Oct. 15, from Friday, Oct. 19, making it among the first of the big banks rather than one of the last to post earnings during the week when most money-center banks are expected to report.

The bottom line is it appears the financial companies are looking to seriously manage the news cycle, which increases the concern.

So -- is this a one-time deal? The reset and default graphs from above say otherwise. So do some analysts:

"This is a multi-year problem, and the market, which has become very enthusiastic about these stocks, doesn't have a clue as to how deep the problems are," said Richard Bove, an analyst with Punk Ziegal & Co. "The write offs they are taking are the beginning of a process that will take at least a couple of years to work out. This is simply not a one-shot development."

Update [2007-10-9 7:58:56 by bonddad]:: Jerome a Paris makes the following point below:

because today's losses are NOT caused by the underlying problems, but by changed market perceptions, that prevented banks from refinancing various transactions, on which they chose to bear losses simply in order not to keep them on their books.

These losses are very real, and have very little to do with the underlying mortagage markets. When these reveal the full extent of their losses, then more pain will accrue to the banks.

I agree with this sentiment. The market has not fully devalued these various investments based on fundamentals. When that happens expect more of this.