On September 24th, Steven Ramirez, a professor of law at Loyola University Chicago, gave a very interesting presentation called "The Subprime Debacle & Subprime Bailouts: Subprime Enforcement, Subprime Accountability, & Subprime Responsibility."

Prof. Ramirez kindly wrote down his thoughts & sent me a copy. Follow me below the fold to read what he has to say about the mess and his proposed solutions to resolving it. After you read this, you'll know more than McCain.

If you agree with his solution, please pass this information on to others and contact your senators/representatives.

From Professor Steven Ramirez, published with his permission.

The single most remarkable fact regarding the subprime debacle is the breathtaking recklessness of the lenders that now seek the most massive public bailout in the history of the US.

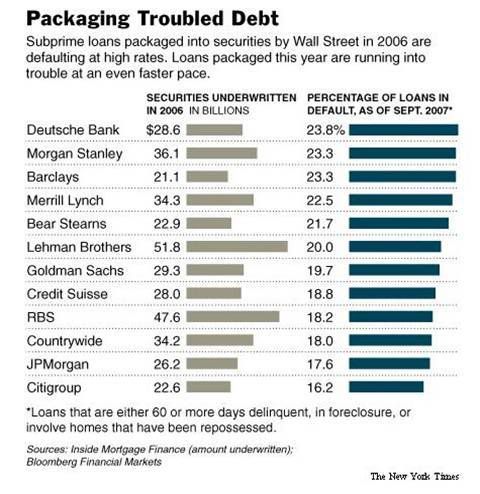

As shown below, the default rates on loans originated in 2006 and 2007 exceeds 30 percent. These loans never should have been made and no bank can survive these kinds of default rates–the losses implied from these default rates will wipe out the interest paid on the entire underlying portfolio and much bank capital. Further, because billions of dollars of such loans were made, their rapid default destroyed the nation’s real estate market.

Since 2007 It’s Even Worse...

- "At the end of June, 5.35 percent of prime loans were past due or in foreclosure, up from 4.93 in March. By contrast, 30.48 percent of subprime loans were past due or in foreclosure, up from 29.53 percent." NY TIMES, 9/5/08

- Overall, delinquencies on 2007 prime jumbo loans rose to 3.22 percent in July, while Alt-A loan delinquencies increased to 14.56 percent. . . .Defaults on subprime loans from last year hit 31.25 percent." Reuters - 8/22/08

The line between recklessness and intentional wrongdoing is often thin. Recklessness may include inexplicable stupidity, but sometimes inexplicable stupidity may be explained by following money.

Pay for Performance or Losses?

• CEO Prince loses $56.4 Billion for Citigroup & walks off with $68 Million

• CEO O’Neal loses $51.8 Billion for Merrill & walks off with $161 Million

• CEO Cayne bankrupts Bear Stearns & walks off with $60 Million

• CEO Fuld bankrupts Lehman & makes $488 Million (1993-2007)

Economist - 8/9/08 and Forbes - 9/15/08

Huge amounts of money ended up in the pockets of these CEOs who ruined their companies (and by extension the economy), which suggests that Professor Joseph Stiglitz, recipient of the 2001 Nobel Prize in Economics, is correct in his assessment that incentives were distorted and raw greed took hold.

"We need to regulate incentives. Bonuses need to be paid on multiyear performance instead of one year, which is an encouragement to gambling. Stock options encourage dishonest accounting and need to be curbed. In short, we built incentives for bad behavior in the system, and we got it." Joseph Stiglitz, Nobel Laurate Economics, 2001

The alternative view is that these bankers were simply very stupid, or as Fortune Magazine has suggested they were smoking something strong.

Given the huge compensation paid to executives for abject failure, and the fact that in the end lending on residential real estate is not complicated, my view is that these CEOs gamed the system to maximize their own payout.

Meanwhile, the taxpayer has been left to clean this mess up.

How much have you spent?

• Bear Sterns: $30 Billion

• AIG: $85 Billion

• FED: $500 Billion in Collateral

• Fannie/Freddie: $5.3 Trillion Debt

• We already own billions of CRUD

• Rogoff: "I can’t imagine a total cost under $1 Trillion."

Financial Times - 9/17/08

So far, the government has already spent hundreds of billions to keep the economy and financial markets afloat. Professor Rogoff from Harvard’s Department of Economics suggests a total final cost to the taxpayer of $1 to 2 trillion. Rogoff is the former chief economist at the IMF which certainly makes his estimate credible. In terms of accountability, the Bush Administration has so far done nothing to enforce the law against the management of these firms that is responsible for this fiasco; on the contrary, the Bush bailout plan now is poised to stuff billions more into the coffers of these firms that will effectively entrench the villains.

The recent failure of Washington Mutual highlights an alternative approach to the Bush proposal. That approach is summarized in the slides that provide an overview of the FDIC/RTC bank bailout process. Essentially, when the government takes over a bank it always wipes out the shareholders, it always terminates management (the board and CEOs), and it always assesses the criminal and civil liability of the managers who killed the bank. I personally represented the FDIC/RTC in numerous civil lawsuits against the former managers of failed banks, and we recovered millions on behalf of the US taxpayer.

Moreover, the legislation (Financial Institution Reform Recovery and Enforcement Act or FIRREA) that funded the FDIC/RTC effort to bailout savings and loans specifically provided for harsher law enforcement mechanisms and whistle-blower incentives so that reckless management would face legal responsibility for their wrongdoing. Unfortunately, the federal courts diluted many of these provisions which hampered FDIC/RTC efforts to recover taxpayer funds.

FIRREA attempted to create a legal and regulatory framework that enforced the law against errant managers, and held them to account for and be responsible for their own recklessness. This sends a message to future managers and creates a disincentive for future recklessness.

The Bush plan is upside down: it rewards the villains, does nothing to help victims, and provides for no enhanced law enforcement mechanisms. Its $700 billion price tag without such provisions simply invites future recklessness by sending a message that the taxpayers will rescue firms from excessive risks, but managers get to keep their large salaries based upon illusory profits.

Accountability & Responsibility

An alternative approach would be to condition any bailout on enhanced law enforcement powers so that the wrongdoers must face civil and criminal exposure. I propose:

- enhanced whistle-blower protections and rewards to lower the cost of law enforcement activities;

- the creation of administrative agencies to investigate and prosecute civilly those who exposed financial institutions to losses from unsafe or unsound financial practices;

- repeal of the Private Securities Litigation Reform Act of 1995 (which protects those who commit securities fraud) to re-energize private law enforcement efforts (and costs the government nothing); and

- the creation of a DOJ Financial Crimes Task Force that is independent of political influence, much like a special prosecutor. This proposal is very similar to the FIRREA approach.

A central part of my proposal is to limit the power of the network of Wall Street cronies who dominate the management of major firms–the old boys network. The groupthink associated with culturally homogenous groups certainly took hold of much of Wall Street when risks were ignored and the profits seemed so easy. Studies demonstrate that culturally homogenous groups make poor decisions. In the US, the vast majority of board seats are held by white males.

One major problem with the board selection process is that CEOs have the power to hand pick directors. Of course CEOs have incentives to stock their boards with their cultural clones in order to maximize in-group bias, and thus their compensation packages.

If the US government bails out Wall Street and takes back equity (as many are now proposing) this equity interest should disrupt the current management of Wall Street that caused this debacle. The government should be empowered to nominate it own directors and the bail out bill should direct the government to seek greater diversity at the boards of the firms it holds equity in.

Let’s be like Buffett (Warren, that is)

• Save the strongest —Goldman Sachs avoided this fiasco

• Preferred stock is senior to common

• No brain-dead management

• 10% return

• "Body Guard"

• No cash for trash for Buffett

The old boys network does not work. This debacle proves that point. Too many firms jumped over a cliff chasing easy money regardless of risk. The government should not now give those managers who caused this mess a blank check. Otherwise, this will happen again.

About the Author:

Steven A. Ramirez is a professor of law at Loyola University Chicago, where he also directs the Business and Corporate Governance Law Center. He formerly worked for the FDIC/RTC and as an Enforcement Attorney at the SEC. He has published widely on securities law, corporate governance (including diversity), financial regulation, and law and macroeconomics. Some of his works are available for free download.

Other Sources:

http://www.ft.com/...

http://www.nytimes.com/...

http://us.ft.com/...

http://www.forbes.com/...

http://www.economist.com/...

Crossposted at Reality Window