It has been 4 1/2 months since Bonddad and I said that the turn in many economic indicators suggested that the Recession might be near ending. Just about all economists agree now that the Recession did end sometime during the summer, if for no other reason than that inventories are being depleted, causing GDP to increase --but also due in no small part to Obama's stimulus plan. Furthermore, almost all the economic data that generally is used to signify the end of recessions: real retail sales, industrial production, real income, aggregate hours worked -- is either going up, or at least sideways. The laggard, is with the past two recessions, is jobs. The country lost 216,000 jobs in August, and as Prof. Paul Krugman has noted, the fact that the economy is in Recovery is "irrelevant" to the issue of jobs which is what most Americans care about.

In this diary I will show you that employers are waiting to see if the Recovery will be sustained before they add on new jobs.

I. First things first. Leading economic indicators have been up strongly for 4 months in a row, and look poised for another decent advance when August's number is reported on Monday. As the graph shows, exactly as has been usual in past recessions, coincident indicators are now poised to turn upward.

Those coincident indicators of the economy include aggregate hours worked, generally going sideways, shown together here with the leading indictor of hours worked in manufacturing, which has already turned up:

as is real income, which trended sideways as of last month:

Real retail sales and industrial production, shown together here (in blue and green, respectively) are both heading up:

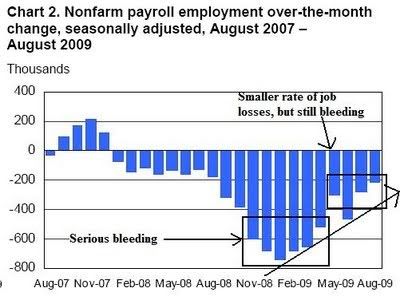

while jobs (red) are still declining.

Jobs have been the laggard. After the number of net losses sharply declined earlier this year, payrolls are slowly trending towards neutrality, but still lost 216,000 last month. At the rate of recent change of ~50,000 to the good each month, it would take until December or January until the economy stops losing jobs, let alone adding enough to stem rising unemployment:

But if the economy as a whole has turned around, why aren't employers adding jobs yet? Because they are waiting to see if the turnaround is sustained.

II. One of the most valuable private sources of data about the economy is the Institute for Supply Management (formerly known as the National Association of Purchasing Managers). Their Manufacturing Index is one of the 10 Leading Economic Indicators. One portion of the ISM index deals directly with employment. The employment index compares the percentage of employers planning to hire, lay off, or keep current staffing levels in the next month. Typically, as a recession ends, first fewer employers plan to lay employees off, and the number intending to keep current staffing levels rises - frequently past 65 to 70 percent. Next the percent intending to hire gradually rises even as the high percent of employers planning no change levels off or declines. In other words, employers tend to hoard plans to actually hire until they are sure that order growth is sustained, and during that interim an extraordinarily high percent will plan no changes. Here is a graph of the 2001 recession and the recovery afterward, showing this typical point:

And here is the current graph:

We just reached the 70 percent no change level in July. In August that dropped to 69, but hiring intentions rose to 13. A shift of merely two percent would give us the 65+/15+ reading that has always coincided with employment growth in the past. The current reading of the index is (- 6), just one short of the (- 5) reading that has typically been a harbinger of growth.

In other words, what the ISM employment index is showing is that employers, whose orders books are growing, are holding off on hiring new employees but instead are holding on to the employees they've got first, to see if the trend continues.

III. This conclusion is buttressed by several other surveys, one private and one by the Philadelphia Federal Reserve Bank.

The temporary placement firm Manpower publishes a "hiring plans" index quarterly. A week ago their Q4 index was reported widely, and very bearishly, in the blogosphere, emphasizing the part that said:

Employers' hiring plans for the upcoming fourth quarter dropped to their lowest level in the history of Manpower's Employment Outlook Survey, which started in 1962. .... Before this year, the survey's previous low point was a net 1% hiring outlook for the third quarter of 1982.

While the blogosphere correctly noted the extremely low levels of employers planning to hire, it missed the two most important forward looking parts of the survey. First of all, bloggers should have taken note that immediately subsequent to the record low hiring plans of 4Q 1982 came a hiring surge that began in January 1983, as employers quickly needed to catch up. Secondly, the blogosphere ignored the announcement that the number of employers planning no change in staffing levels reached an all time high:

There was one positive sign in the survey: 69% of employers said they planned no change in their hiring plans, up from 67% in the third quarter and 59% in the fourth quarter a year ago.

In other words, the Manpower report shows the same thing as the ISM report. Employers are "hoarding" job hiring intentions, holding on to existing employees and planning no change until they see if the upturn is sustained.

Finally, the Philly Fed published its September report on Thursday. This report, along with the other regional Fed reports, is a harbinger of what we can expect from the ISM report in a couple of weeks, and then payrolls shortly thereafter. It said in part:

The region’s manufacturing sector is showing signs of growth, according to firms polled for this month’s Business Outlook Survey. ...

The survey’s broadest measure of manufacturing conditions, the diffusion index of current activity, increased from 4.2 in August to 14.1 this month. This is the highest reading since June 2007 and the second consecutive positive reading. ... The current new orders index also remained positive for the second consecutive month, although it edged one point lower, to 3.3.

Labor market conditions remain weak, despite signs of improvement in overall activity. The current employment index decreased slightly, from ‐12.9 to ‐14.3. Overall declines, however, are still not as widespread as in the first six months of this year. ...

Notice that, like the ISM, business conditions in general and new orders in particular continue to improve. But firms are still shedding employees. H/t to Jake at Econompix, who notes:

In looking at the data, it looks like this has been a pretty typical pattern, especially coming out of recessions. New orders come back, but hiring is delayed until the economic rebound has been proven (hence why unemployment is a lagging indicator).

and supplies the following graph, comparing the difference between new orders and hiring:

Note the spikes in New Orders vs. Hiring at the time of rebounds is similar as that from every prior recession.

In summary, the Manpower and Philly Fed surveys confirm the ISM survey from July discussed above. Employers are all seeing increasing business. They are waiting to make sure there is a further sustained increase in customer demand before they increase plans to hire employees for new jobs.