I am writing this diary in a response to a deceptive campaign I see going on here. The activists at FDL are being slandered even though their efforts are one of the few actually getting results. It should not be something held in contempt if one truly believes in working for progress, as this is the way the progressive reforms of our history were brought forth that we all hold so dear. They want to hold our representatives accountable because in case anyone forgot we live in a representative Democracy via a Republic. They are holding their feet to the fire on what they campaigned on, what the American people want, and what their constituents want for the most part. Chris Bowers put it well as well as mcjoan:

Chris Bowers: In addition to this broader grass roots and media strategy, besides turning out at town halls and other health care events and making your support know directly to members of Congress so you’re also showing local and national media your support for real health care reform, there’s also this elite strategy. I think it’s very important that if you have a blog, or if you keep a diary on another blog, or if you’re just a commenter, that it’s essential that we push back hard against strategies like the one that Jane was mentioning like the one Paul Begala was mentioning in the Washington Post. Because as soon as there is no block of progressives saying they will vote against legislation unless it meets a certain criteria, there’s only one direction health care negotiations will take and it will never turn around. The bill will simply become weaker and weaker and it will become weaker though every step of the process. It will become weaker as the three bills are merged in the House and the Rules Committee.

It will become weaker when it comes from the Finance Committee. It will become weaker than that when it comes to the Senate HELP Committee and Finance Committee bills are merged. It will become weaker on the floor of the house. It will get weaker on the floor of the Senate. Then it will get weaker as they both pass it in Conference. It will get weaker every step of the way. That is exactly what happened in the America Clean Energy and Security Act.

At no step in the process for that essential climate change legislation has that bill gotten more progressive. It has gotten worse at every step and will continue to do so. Tom Harkin whom was chairing the Senate Committees that have oversight over the ACES bill has already said he will incorporate every single concession that was made to Colin Peterson and the blue dogs in the House of Representatives as the starting point for his bill in the Senate. It’s only going to keep getting worse through that Committee. It will keep getting worse on the floor of the Senate and then when the bills are merged in Conference it will get worse and worse.

There will be more giveaways to polluters. There will be lower RES standards. The Clean Air Act will be gutted even further and god knows what else is going to end up in there on top of it. That’s going to happen on health care unless the progressive block holds! There has been push-back to the left to make bills more progressive on several occasions simply because of the progressive block.

Instead of Senators Hagan and Bingaman in the Senate HELP Committee forcing concessions to that bill, they were pushed into line. Instead of all of he concessions that Henry Waxman made to the blue dogs and the Energy and Commerce Committee standing in place, several of those were walked back immediately by progressives in the Committee. This is the only strategy that has ever been shown for bills to be moved to the left, to become more progressive and stronger. And as soon as we drop that demand and as soon as we drop that block like Paul Begala and sadly even President Clinton says, there’s only one direction that any piece of legislation will take. It will become worse. It will become weaker. It will become more pro corporate. We have to push back against that narrative to elites as hard as possible.

mcjoan: And to follow up on that, it’s not going to be just health care. This is the big first fight in which we have to draw the progressive line. If we fail here, then it going to be the rest of this term and next term where we keep losing on progressive issues.

I’m pushing back against another failure of an elite strategy I see right here and it’s people here who are lobbying for the insurance industry (whether tacitly or they just want any crap reform bill to pass which benefits them and theoretically all of us which is false), which is hilarious and ridiculous at the same time, while they are slandering everyone at FDL who posts here trying to make this place just an echo chamber of the DNC. This contempt for real activism is something I can no longer ignore. All sorts of accusations about disclosure have been thrown their way, and unless you don’t pay attention to their writing, you would know exactly how and when they spent their money and now since they were pressured to be more explicit, it’s even more clearly out there in the open and they deserve every penny for their work and you see exactly what you are getting unlike the many BS partisan DSCC, DNC, and DCCC mailers that don’t tell you that they are funding blue dogs and Conservadems.

There are posters here with a vested interest in defending the insurance industry; industries they work in, whether it’s life insurance or some other form the point remains the same. There seems to be a pattern. I’m not going to call out names, but I’m sure you will get the idea of whom once I post some relevant information. It’s bad enough that this is going on, but then they have the gall to even pretend to care about the 45,000 who die a year by the industry they are tacitly defending whether they want to admit it or not.

What else makes it worse is that they are going to downplay this immoral effect of sick-for-profits by comparing those profits with other more profitable industries as if people dying so insurance companies can make a ridiculous profit considering they don’t do anything of value, as if this is an apples to apples comparison. It’s actually pretty insulting and sickening and you will see that we pay for their profits via gains and losses in the stock market in connection with Wall Street; another variable they conveniently left out. It’s also economically ignorant as well as morally ignorant to defend profits this way. For every health profit margin off of the sick there is less demand in our economy and greater costs we all bare at the emergency room. Also a recent study found that 62 percent of all bankruptcies filed in 2007 were linked to medical expenses and about 1.5 million families lose their homes to foreclosure every year due to unaffordable medical costs. Of those who filed for bankruptcy, nearly 80 percent had health insurance. You see, this is not good for equity as the value of abandoned homes drops and affects the homes around it, but yet profiteering off of that is somehow OK just because profits are bigger in other industries? Talk about a non sequitur in the grand scheme of things in the lack of seeing the bigger economic and moral picture.

An industry that puts barriers for those who need preventative care like screenings and checkups of all types which then turns out over time to equal the crux of all health care costs via a sicker population does correlate with the 30% of administrative overhead causing barriers that causes this problem with our population. This sick reality is being used to defend a system as if it has little to do with these costs as if they are an exogenous variable onto itself despite billing departments and other forms of administrative waste in association the increasing umber of uninsured and the insured who still don’t get access to care adding up from year to year. Not to mention other factors not even accounted in administration costs technically but in association with economies of scale from a monopolistic structure.

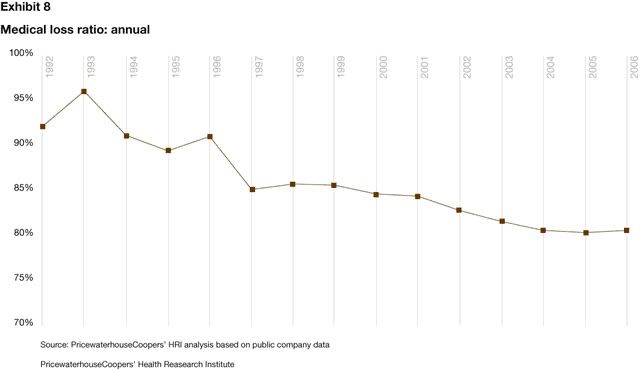

Now it’s well known that profits are not the only cause of health care inflation but in correlation to denied care and barriers to preventative care causing the most expensive problems with that sickest 10% equaling 2/3rds of all health care spending it's absolutely a huge factor over time. I find that none of the posters here who defend the insurance industry have the depth of knowledge and character that Wendell Potter does as he explained how Wall Street puts pressure on the for profit insurance industry involving Medical Loss Ratio in addition to other pressures related to stock performance in relation to this problem. You cannot separate the overhead and the profits off of Medical Loss Ratio from the most costly problems either. You hope you can apparently, but you can’t. Some people act as if there is not a disturbing trend at all. As the trend goes down, insured people are then put down via denied care to keep stock prices up with a failure of a health care system that cannot work at all in this country without any public element to keep it in check going by the facts.

.

.

Wall Street is not happy about the prospects of a public option because public options don’t fit well within a need for greed society like the kind that have caused our economic crisis in collusion with the insurance industry. But they leap with joy at the prospects of our House of Financial Lords working to defeat any kind of public option at all:

http://www.americanprogress.org/...

It’s not clear which direction Congress will take. But it is clear that Wall Street is watching the legislative maneuvering with great interest. The equity analysts at Credit Suisse, an international financial services group, are very upbeat on the prospects for insurers and in particular the largest among them, Minnesota-based UnitedHealth Group:

Recent events in Washington reinforce our view that health care reform will include a substantial expansion of the Medicaid program and the creation of an insurance exchange with either no public plan option or a fallback public plan option. We believe UNH is best positioned to capitalize on the growth opportunities that will emerge through reform. Specifically, we conservatively estimate that Medicaid expansion can add $0.05 to annualized earnings per share and that the creation of an exchange and/or increased employer-based coverage would add $0.25 in annualized EPS.

Independent equity research firm Argus Research Group has a decidedly more pessimistic view on UnitedHealth Group:

Moreover, we take a cautious stance on the managed care sector in general as we wait to see what form the final legislation on universal coverage will take. One proposal, a government-run public plan, would pose serious risk and competition to commercial plans currently offered by private insurers such as UnitedHealth.

Standard and Poor’s Stock Report offered a similar assessment:

...We think investors see health care reform, currently being addressed by President [Barack] Obama and Congress, as helping to reduce medical cost trends... But we suggest investors remain cautious, on our view that the idea of a public plan is still alive.

Here is one of the many missing variables when this armada of tacit insurance defenders here at kos downplays the profit margins of Insurance Robber Barons that cause the exploding costs of a sicker population in correlation as well.

Shareholders have a lot at stake. If the cloud of health care reform is lifted and earnings rise even marginally the value of these stocks could soar. The 1.1 billion shares of UnitedHealth Group are divided amongst 14,000 institutional and individual shareholders. Credit Suisse projects the shares to rise from near $27 a share level where they have traded at for most of the summer to $33 in the reasonably near future. Analysts for Morningstar see potential appreciation in the shares of 66 percent, or to about $48. But even at $33 the total increase in the value of UnitedHealth Group shares will increase by nearly $7 billion.

There has also been a lot of crap posted downplaying the effectiveness of Medicare’s administrative costs, so let’s look at this comparison of Medicare versus these insurance champions’ UnitedHealth Group who manipulate the studies I mentioned earlier with it’s subsidiary the Lewin Group cited by Republican Congressman in order to downplay the effectiveness of Medicare and HR 3200. Except it gets kind of hard to defend for profit failure and the collateral damage associated when you actually look into it and put it in proper perspective. At the last link:

One perspective on the reasonableness of the "operations" or administrative costs charged by private insurers such as UNH is to compare them with the administrative costs of the Medicare program. In 2007, Medicare paid out $434 billion in benefits or nearly eight times the amount paid by UNH. But according to the budget justification that the Centers for Medicare and Medicaid Services, or CMS sent to the Congress in 2008, the cost to the government of processing the claims, determining the appropriateness of the billings, and administering the reimbursements in 2007 was less than $2.3 billion. In other words, Medicare was covering nearly eight times as much medical care for less than a quarter of the administrative cost. In addition, Medicare’s administrative costs in 2007 equaled less than a third of UNH’s before-tax profits.

Nationwide there are 4,400 government employees who work for CMS (including those who work to administer the federal share of the Medicaid program). Their annual salaries totaled $383 million in 2007. The profits that Stephen Hemsley reaped from the exercise of one year’s worth of stock options this past February would not only pay the salary of the administrator of CMS but of every employee in the agency for more than three months.

It will be pretty hard to discount this example, but some will try. I have other flaws and missing variables from their ‘shilling for my insurance industry’ examples while we are on the subject. The low administrative costs of Medicare correlate over time to be even greater as more and more people get preventative health care (if they have the access that a public option or it’s there to catch them if they are denied) and so procedures are then less costly giving the benefits of bringing down cost inflation even more as there is more than just the cost of administration. It’s a lot better and we could improve Medicare because it was basically ruined by Republicans and GWB even though they couldn’t get their hands on SS(thankfully) they successfully partially privatized Medicare and now we have HMOs and Big Pharma sucking it dry. I was happy to see Nancy Pelosi take steps toward this road and especially happy that she didn’t want to even talk about a trigger, because neither do I. Of course then some people pulled the reimbursement rates distortion, which though they could be improved, don’t really take into account the data that disproves the flawed theory that physicians will stop accepting Medicare patient under those rates in this robust public option scenario.

Yale’s Jacob Hacker: the author of the public option has it down. (I’m glad Edwards put it as part of his political platform making it a political reality thus forcing the other candidates to take suite thus giving us the momentum to talk about it now.)

http://institute.ourfuture.org/...

Another source of comparative insight is the relative costs of the public Medicare plan and private plans that contract with the program through Medicare Advantage. The gap between the administrative costs of the public Medicare plan (2 percent) and those of private plans (11 percent) has been mentioned. But the experience of private plans within Medicare offers a more general portrait of the (limited) ability of private plans to restrain costs.

As is well known, Medicare Advantage plans are substantially overpaid relative to what it would have cost to provide coverage to the same enrollee in the public Medicare plan—13 percent more on average per person, as calculated by MedPAC and confirmed by the CBO.25 This overpayment reflects two main problems: a method for paying plans that subsidizes their participation in Medicare Advantage and the ability of the plans to attract healthier (and hence less costly) people with Medicare. Both of these problems can and should be addressed—in Medicare and in any new framework for public-private competition.

The Medicare Advantage and true Medicare data comparison is missing in this failed attempt at "even if we went to Medicare for All or had a Medicare like option it wouldn’t solve our problems" excuse I’ve unfortunately heard by these bad Samaritans shilling of their industry. Any premise from a false one with missing variables like the privatization of Medicare in 2003 is utterly useless and dishonest. And you have a major private public administrative study right there. 2% compared to 11% is a major difference like almost 1/5th the cost of partial private Medicare Advantage. Not something to scoff at and must be added or making any honest Medicare comparison.

The next time any of these Humana I mean, "humanitarians" wants to try and point out how insurance profits aren’t really that much of a problem in comparison to be able to defend a for profit ineptly regulated system, remember this; another missing variable making their assertions and examples misleading; a missing component from a study from Milliman USA that examines the pattern of annual gains and losses in the private health insurance industry -- known as the underwriting cycle -- and its impact on Health Plan premiums and profitability.: This is from 2003 but still relevant in my view as things are even worse in this vein now.

Over the last few decades, typically, Health Plans realized underwriting gains when health care cost trends were falling, and experienced losses when trends were rising, according to the report. This pattern changed toward the end of the 1990s, it notes, when underwriting losses were replaced by gains, even as health care costs were rising.

"This was due to insurers attempting to improve their profitability after having eroded their surplus by aggressively pricing in reaction to the stiff competition (for market share among health plans) in the mid-1990s," according to the report. "Financial problems contributed to consolidation in the market, reducing competition and allowing Health Plans to raise premiums. This trend correction began to produce gains in 1999 and 2000 that have continued through until 2002."

The report explains that underwriting refers to Health Plans paying or reimbursing for health care in exchange for a premium. When Health Plans collect premiums that exceed the amount of money that they pay out for health care ("claims costs") and the cost of doing business, they experience an "underwriting gain." When their collected premiums are less than claims and business costs, Health Plans experience an "underwriting loss." Health Plans' profitability is determined primarily by underwriting gains and losses, and by investment income.

A disturbing trend you would think these "experts" would notice in their defense of the industry, but apparently not. A break in the trend similar to the one Dean Baker noticed in 2002 with a break from the Housing prices and inflation trend. You would think would sound the alarm as well as consolidation of our monopolistic insurance market. Historically, this type of market hardly ever benefits consumers no matter how much anyone inside the industry wishes it were so.

(From the PDF of the study linked to on that page)

A health insurer or Health Plan accepts responsibility for paying for the health care services of covered individuals in exchange for dollars, which are usually referred to as premiums. This practice is known as underwriting. When a health insurer collects more premiums than it pays in expense for those treatments (claim costs) and the expense to run its business (administrative expenses), an underwriting gain is said to occur. If the total expenses exceed the premium dollars collected, an underwriting loss occurs. Health care cost trends refer to the rate of growth in health care claim costs.

To protect the interests of the beneficiaries of Health Plans, insurance regulators require that Health Plans have additional funds put aside over and above the amount they expect to have to pay out for health care services in a given period. These funds are known as surplus and serve to meet a company’s risk based capital (RBC) requirements. The investment of these fund provides an important additional source of revenue for Health Plans, returns on invested assets.

That’s right, returns on invested assets. But wait, there’s more!

Health Plans must maintain adequate surplus levels. They also have a claim reserve for claims incurred but not yet paid. These funds are invested and the return on this investment is another source of revenue. Gains and losses on investments can affect premium levels, adding another layer of uncertainty in determining what premium rates will be adequate in a given year. The high returns on invested assets during the boom of the 1990s allowed Plans to partially offset underwriting losses during the last low point of the insurance cycle. As the economy slowed, the evaporation of these returns was another contributing factor to the sharp increases in premium levels experienced over the past several years. Health Plans heavily invested in equities (e.g. stocks) were especially hard hit. For example, Blue Cross/Blue Shield plans with an average of 19.3% of their portfolios invested in equities (compared to 3.6% on average for publicly traded health insurers) faced a significant loss of investment income.

This is important information left out when trying to downplay profits, just because other Wall Street firms pressuring insurance companies and more profitable companies do exist doesn’t excuse a sick for profit system that causes all ailments and even greater costs to build up in correlation with this failed system that treats human beings like a commodity. I wonder why the Wall Street connection isn’t mentioned more by some here that love this industry and want to make excuses for it? I know one reason why, but perhaps there is another. An inept understanding of our crisis through a gilded view of the for profit model as they are swimming in it. According to the regulatory law mentioned above these companies have to keep a surplus; consumers are stuck with paying for the incredible gains and incredible losses(You have to count losses as well) from these same investments with their premium dollars or through their health with rescission and medical loss ratio.

Some of these investments are toxic and since an insurance company usually has to stay afloat by law according to their RBC requirements along with added pressure by Wall Street investing in them and that their stock portfolio keeps going up; that cost is passed onto the consumer as they are priced out of the market thus pointing to the trend of uninsured and under-insured. This is a hidden addition to the profit margin that is still obscene(Many wish you wouldn't notice so their industry can look betetr with their flawed example defending profits), and with the added losses to that margin it adds up to a lot more than realized. This varies from state to state as some states better regulate insurance companies via community ratings so these losses are not pared off on the public as much, but it’s still a problem that is quite rampant and more costly than some people want to admit, even though a portion of the sickest population caused by this system costs the system the most. Some people are able to try and point to that to defend the system that caused that costly population percentage to be that way. All in the manner of unenlightened self-interest, but that fails on many levels.

It’s also not something that gives one comfort in the ineffective insurance regulation touted here by some to defend the system even though it’s been tried and failed as a US model in many different states having missing for profit variables that make it a success elsewhere. There are clear-cut examples that show this I will provide later. The for profit model left alone with no public option doesn’t work for anyone but Wall Street and their puppets; insurance companies, HMOs, and big pharma.

There are two primary components to the profitability of health insurers – underwriting gains and losses and investment income (including realized and unrealized capital gains and losses). Therefore, if an insurer must achieve a specific gain to satisfy stockholders minimum capital requirements or insurance regulations, whatever they cannot generate from investments must be generated through underwriting results. Federal Income Tax and other reductions to income average about 0.5% per year net, and must also be reflected in the equation.

There it is. A for profit model by statute is explicitly tied to Wall Street. Wall Street brought down our entire economy and erased billions in wealth. To think that insurance companies are not invested, especially considering AIG and Travelers Group which merged with Citibank and Citicorp into Citigroup once Glass Steagall was repealed to let insurance get involved with banking in association with CDS via mortgage derivatives unregulated by the Commodity Futures Modernization Act is not smart. Health insurance companies have some of thee same investments. It’s also immoral to let or defend even tacitly people’s health and well being traded into that bear market. Which brings me to the next derivative scheme.

Life insurance is already going to be the next shell game. Think about that next time someone who works in life insurance wants to make predictions about trusting insurance markets to write their own regulations(like too big to fail banks and AIG) now that derivatives of all sorts including on people’s lives are now openly being traded again. To some this is not a problem and they have it all worked out in their flawed actuarial predictions, but not me. I like cause and effect reality and reflection rather than comfortable lies with statistics to pretend our for profit model just needs a little tweaking like Wall Street needs just a tiny bit of tweaking. Wrong. Both need a complete overhaul or at least the beginning that could lead to one on health care at the very least.

You'd think some profiteering schemes are too sick even for Wall Street. But think again.

Wall Street is hoping that health care reform fails so not only will insurance company profits and salaries rise but big banks can get in on the business. Goldman Sachs and other bailed out banks are putting big bucks into death bonds. When their last sub-prime mortgage scam went bust, we lost our houses. This time, we'll lose our lives.

If insurance companies get their way and the quality of American health care continues to decline, the value of "death bonds" --- life insurance policies bought from the sick and elderly that increase in value the sooner the policyholders die --- will skyrocket. It's not sick enough that private health insurance CEOs are making millions by putting profits before patients, cutting care and denying claims left and right. Now Wall Street wants in on the scam.

Check out this video where I take to Wall Street to ask executives and average folks what they think about this latest gruesome scheme from the big banks.

More Wall Street stock manipulation financed through premiums. Kind of hard to say, "It’s not so bad. We can patch it up" but go ahead and try to explain how 52.4 billion spent on pumping insurance stock prices through buyback will lead to better health outcomes.

The rising premiums paid by employers and families not only generate oversized net earnings, they also fuel controversial financial maneuvers designed to pump up insurers’ stock prices, which in turn help executives reach their personal bonus targets. From 2003 through 2008 the seven largest publicly traded health insurers, which cover 116 million Americans, spent $52.4 billion buying back their own shares. Buybacks reduce the number of shares that are publicly traded, raising the value of existing shareholders’ stakes. Companies make share repurchases with excess cash on hand or with borrowed funds.

Buybacks are a way of removing money from a company’s balance sheet for the benefit of investors, reflecting management’s decision not to invest in improving a company’s operations, making the health system run more efficiently or reducing customers’ premiums. The companies prefer to hand over the money to Wall Street investors and executives whose soaring compensation packages depend on reaching earnings-per-share goals that often would not be achieved without buybacks. Insurers have demonstrated through their actions that they do not use consolidation to bring efficiency to the health insurance marketplace.36 Instead health insurance companies use their size to engage in anticompetitive behavior, rig the system to impose premium increases that grow faster than individuals, families, and businesses can afford, and ensure "astounding levels of profit" for themselves and their shareholders.37

This is where I really expose the elitist BS going on here about how we can just trust that regulations (that insurance companies will be writing themselves like the banks did and we are now seeing the same shell game once again as I have shown above) Work! Except they were tried and they didn’t; the same regulations being peddled here as a replacement for the public option that certain insurance workers support even though they say they are open to a public option but spend most of their time attacking it and the great front pagers like mcjoan fighting for it. Here it is; the same BS being touted as a replacement for the public option exposed because it was tried in Massachusetts:

Unsubsidized Care for the Middle-income Uninsured

For the Commonwealth Choice program (the unsubsidized menu of plans for those earning more than 300% of the FPL) the Connector selected six large commercial insurers. The Connector classifies the available commercial plans into four levels: Gold, Silver, Bronze, and Young Adult. The first three levels are based on the comprehensiveness (i.e. actuarial value) of the plans. For instance, lower-priced Bronze plans include a $2,000 per person deductible, restrictions on site of care, co-payments, etc. Gold plans resemble a traditional Blue Cross policy, but are very expensive. The fourth level (Young Adult Plans) offers a slimmer benefit level with caps on total benefits and is available only to adults younger than 27 years old.

Actuarial magic! That magic didn’t come to fruition. Remember this when anyone talks about how certain people just don’t understand the insurance regulations in the bill like the pseudo insurance worker geniuses here unable to see cause and effect reality. These types of regulations against insurance monopolies have been tried in numerous states by themselves and failed. It’s sad to see people pushing them, as if they are a magic panacea so we can sell out so their industry can make more money off of death. These people are conceded and wrong. Now give back the magic risk ball, Nostradamus.

A no brainer:

Access to Insurance Does Not Guarantee Access to Care

Massachusetts health reform has had a salutory effect on access to insurance, having provided half or more of the state’s previously uninsured residents with insurance policies. Yet, it has had a lesser effect on access to care. For some state residents, the reform has actually made access worse, even before the latest round of cuts to safety-net providers. Many low-income residents had been eligible for completely free care (including medications) under the state’s old free care system, including all residents earning less than 200% of poverty.

Access to care was often excellent for low-income residents living near a safety-net provider such as a public hospital or community clinic, but less than adequate for those living further away. The new insurance policies that replaced the free care system require co-payments for office visits and prescriptions, which are difficult for many low-income patients to pay. For instance, at Cambridge Health Alliance, doctors and nurses have cared for patients who were forced to interrupt care for HIV and even Hodgkins lymphoma, two serious but highly treatable conditions, because they were unable to afford the new co-payments. (Several of these cases have also been reported to the state).

Moreover, the situation is likely to worsen. For fiscal year 2009 the Connector went through protracted negotiations with the four non-profit insurers participating in Commonwealth Care (the subsidized insurance program). In order to bring the state’s cost increases down from 15.4% to 9.4%, the plans boosted co-payments and enrollee contributions, making services even less affordable for the near-poor families enrolled in Commonwealth Care. Several safety-net providers are now demanding (for the first time) that patients whose condition is not immediately life-threatening make up-front co-payments before seeing a doctor. Many middle-income Massachusetts residents continue to have private policies with substantial gaps like co-payments, deductibles and uncovered services.

The new law has put the state’s imprimatur on high deductible, high co-insurance plans by offering them as "Bronze Plans" through the Connector. Such skimpy plans are known to decrease access to care, and provide little financial protection in the face of a prolonged and expensive illness. For instance, studies of medical bankruptcies have found that more than three-quarters of those bankrupted by illness or medical bills have health insurance at the onset of the illness that bankrupts them4. Bankruptcy sometimes occurs when a breadwinner loses employment, and with it health insurance, due to illness. In other cases, bankruptcy occurs in families who keep their private insurance throughout an illness, but are bankrupted by gaps in their coverage like co-payments, deductibles, and uncovered services. The Massachusetts reform failed to address the problems of these so-called underinsured.

And yet this is being touted as a replacement for a public option? And we’re told "these regulations work! I know what you’re going to say:

"What do you know about actuarial economics, priceman?! I’m an expert! Besides what other time have these actuarial assessments failed and when have the experts ever been seriously wrong in this field?"

Besides the Mass example I just presented, I will answer in the tradition of the Late Show’s with David Letterman’s top ten list:

The Top Ten Casualty Actuarial Stories of 2008

By Christina Gwilliam and Michael Christian

The most obvious failures will soon be seen in theatres everywhere. I can’t wait to see the love story, myself. So calling me names for pointing out the flaws in these predictions on positive outcomes and how they have not been based on reality will really look silly to anyone who’s been paying attention to what has been going on. You know, since the combination of insurance on garbage assets and commercial and investment banking was merged along with no regulation on derivatives via Alan Greenspan’s "flaw" as he puts it. Many people have lost everything because of them and we all know people who have watched their 401ks disintegrate. It’s really not time to get condescending in this field according to health care and especially insurance actuarial predictions in general as it flies in the face of one of one of the most significant factors of this financial crisis. I could literally feel the failure in the example of Ike as I went through that and it was horrible and it wouldn’t be a good idea to tell people here that they just don’t get the magic of actuarial models.

The ninth-ranked story is the failure of the catastrophe models to accurately predict losses from Hurricane Ike.

After making landfall in the Galveston Bay of Texas as a Category 2 storm, Ike continued to move north and caused significant wind and rain damage in ten Midwestern states. ISO’s Property Claim Service estimates the insured losses over $10 billion, making it one of the costliest storms in history. The destruction caused by this wide storm with low wind speed and high storm surge is forcing modelers to revisit their model assumptions and insurers/reinsurers to revisit their catastrophe risk management plans.

Now another basic lesson that you would think certain people on this site with such condescension towards activists would warrant basic study on the subject, but here we go. The same people touting that the regulations in whatever bill comes out of the Finance Committee merged with HR 3200 in Conference can suffice without a public option often cite Switzerland as an example. I think they are very confused and delusional so I am going to put this very plainly.

THIS IS SWITZERLAND.

They say:

"This is a clear example that multiplayer private insurance works without a public option, so there. I work in the insurance industry! I know!"

Do you? I don’t think so.

After all, if they did they would know that in order to compete in the market for compulsory health insurance, a Swiss health insurer must be registered with the Swiss Federal Office of Public Health, which regulates health insurance under the 1994 statute. This is statute is called the Federal Health Insurance Act of 1994. It states quite clearly for anyone to see at the Federal Office of Public Health’s website. It helps to know these things when trying to pretend this model even relates to any of the bills in Congress (something to remember when denigrating other people as emitting this is pretty damn embarrassing):

Social health insurance gives everyone living in Switzerland access to adequate health care in the event of sickness, and accident if they are not covered by accident insurance. Social health insurance is operated by a number of insurers. Only those which meet the conditions set out in Swiss legislation, and which are not profit-making, are authorized to handle social health insurance. They must apply the legal provisions in an identical manner and separate from other insurance (for example, complementary insurance according to by private insurance law). If an insurer becomes insolvent, the cost of its statutory benefits are taken over by a joint body funded by contributions made by the insurers on the basis of their social health insurance premiums.

The role of the insurers is not restricted to reimbursing the cost of services provided to insured persons. They also work together with the cantons to encourage health promotion. Insurers and cantons operate a joint body whose aim is to promote, co-ordinate and evaluate steps aimed at promoting good health and preventing illness.

Once again, the insurers were not allowed to earn profits from the mandated benefit package, although they have always been able to profit from the sale of actuarially priced supplementary benefits (mainly superior amenities). If this were any part of any of the bills there would be even more opposition than HR 676 or Bernie Sander’s single payer bill, so it’s really dishonest to even try to make this comparison at all.

Since this basic information was purposefully left out in order to defend the insurance industry some of the posters work in, I feel it’s necessary to show what country we live in as well (most of us who post here anyway).

THIS IS THE UNITED STATES OF AMERICA.

I know, you say, there’s no need for that! That’s condescending! No, it’s necessary, unfortunately. Because we live in the U.S it’s even more necessary to expose how little those touting regulations in place of a public option know about the history of the subject and why they won’t work without any public option mechanism.

Because this is the U.S and on the books we have the McCarran-Ferguson Act which exempts state from federal antitrust laws in the business of insurance, pretending that the regulations touted in place of a public option can achieve the desired results could only stem from a willful ignorance of the highly concentrated non competitive insurance markets in each state of a monopolistic for profit insurance model running rampant in our country and some people want to accept that? As Paul Rosenberg of Openleft puts quite succinctly, this is a very bad Herfindahl-Hirschman Index and it doesn't bode well for a successful system without a public option, period, unless you support monopolies which is essentially supproting market failure. You see, unlike some, I'm not a big fan of too big to fail institutions and hierarchy like I'm not a fan of a too big to regulate insurance model. Again a serious variable that should be mentioned while trying to prop up industry regulations without any public safety net to compete at all, but strangely it has been absent.

This is why the accusation that some people only care about their industry and are lobbying for it here has teeth, because this is not even being discussed by these people. We should increase federal regulation so that federal antitrust law applies to health insurance companies in coordination with state laws. We want to coordinate a systemic national policy rather than rely on local governments to overcome the corruption that may occur to the dominance of local insurance companies. Another is that we may want to set policies about pricing that cannot easily be addressed at the local level. We may not even get the desired results unless the laws have teeth as we see monopolies in the insurance market, and the reason why a change in antitrust law is probably necessary, is that health insurance in our for profit model is naturally monopolistic.

A natural monopoly is a monopoly that exists because the cost of producing the product (i.e., a good or a service) is lower due to economies of scale if there is just a single producer than if there are several competing producers.

A monopoly is a situation in which there is a single producer or seller of a product for which there are no close substitutes. Economies of scale is the situation in which the cost to a company of producing or supplying each additional unit of a product (referred to by economists as marginal cost) decreases as the volume of output increases.

Economies of scale is just one reason for the existence of monopolies. Monopolies also exist because of sole access to some resource or technology and because of the use of non-market means to eliminate competition, including buying up competitors, colluding with suppliers or customers to discriminate against competitors, enacting legislation to restrict competition, threatening costly lawsuits or even engaging in physical violence.

If there are multiple firms in an industry that is characterized by natural monopoly, all except the one that can attain the largest volume of output, and thus the lowest production cost, will generally exit the industry because they will not be able to compete on a price basis. Once a single firm becomes established in an industry that is characterized by natural monopoly, it is very difficult for competitors to emerge because of the very high costs for production facilities (including infrastructure) that allow a scale of output equal to or greater than that of the existing monopolist and because of the uncertainty that they will be able to oust the existing monopolist.

This also applies to why hospitals are monopolized because of the different much worse insurance bureaucratic structures due to a for profit model’s economy of scale to make paperwork and patient records more complicated and hospitals not able to make it unless they conform and so they are also consolidated and costly having to incorporate the economy of 'for profit' inefficiency scale in their models of practice or they can't compete because that's the name of the game in our horrendous system.

Also next time Wyden talks about competition remember that monopolies equal market failure and no competition state by state.

It’s very important that people who consider themselves progressives don’t forget this. So the next time you see a post inferring how stupid they portend to think mcjoan or Hunter is because they are not shilling for a failed for profit model with absolutely no public option in the equation, remember that they are both excellent and are doing excellent work for the benefit of real progress that affects peoples' lives. Remember how easy it is for those in the industry to get caught up in what their version of reality is rather than cause and effect reality.

It also helps to know some history of the progressive movement, too. There was a reason Teddy Roosevelt(where the initial idea of UHC came from in this country influencing his cousin FDR) had to bust some of the railroad monopolies up; sometimes you can’t regulate monopolies; and those wanting to think we can should really study what the conditions were that gave rise to Eugene Debbs, Samuel Gompers and the AFL and all of the Labor movement in reaction to the monopolistic abuses during the progressive era. It was by the same types of Robber Barons we are facing today.

And in that tradition, I have to ask Kossacks, "Which side are you on? The insurance/big pharma syndicate cartel or what the American people voted Democrats and president Obama in for? Are you willing to acknowledge reality even if it is a sacrifice for you and your industry for your fellow men and women?

I think most progressives hope so, because you should.