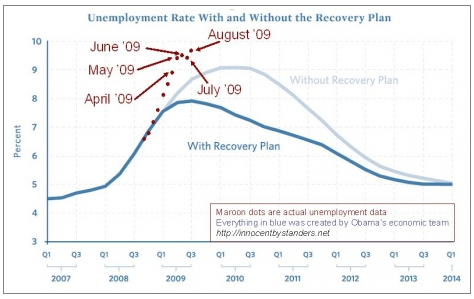

With potential steep losses in next year's elections, the jobless situation is focusing the concentration of Washington's Village democrats marvelously, via a "Jobs Summit" today. Better late than never, I suppose. Somebody on CNBC actually made some sense yesterday by noting that Congress and the Obama Adminsitration probably wish they had paid more attention to this issue, and less on healthcare, this year. Certainly there was an atmosphere of "Mission Accomplished" conveyed by the Administration once they passed the stimulus legislation in February, dusted off their hands and moved on to the next item on their "to-do" list.

Instead, here is what happened to employment, compared with the Administration's baseline estimates in February (and this is 3 months old!):

How is the economy in general, and the jobs situation in particularly, doing at this point? Below the fold is a Report Card for Congress and the Obama Administration.

Here is a "report card" on the economy, and jobs, for November. Some parts of the economy are indeed having a V-type of recovery. Others are showing anemic growth. But where income and jobs are concerned, so far there is no recovey anywhere to be seen.

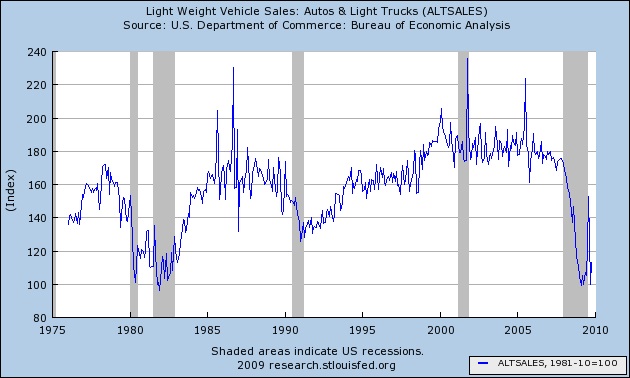

Certain parts of the economy are actually having a V-shaped type of recovery. For example, even excluding cash for clunkers, auto sales have improved by nearly 2 million vehicles (from 9.1 to 10.9 million on an annualized basis), or 20%, from their bottom earlier this year:

This improvement beats every other improvement except for 1982-83, and only trails that V-recovery in sales slightly.

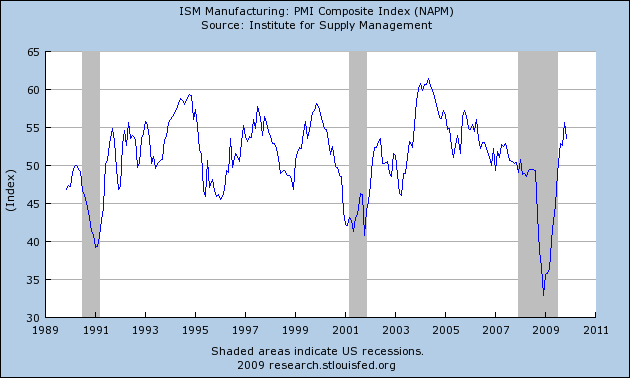

Similarly, the Institute for Supply Management's manufacturing index shows that manufacturing is are not just expanding, but expanding at a faster manner than in 2002-03, and slightly faster than 1992", although not so fast as 1983:

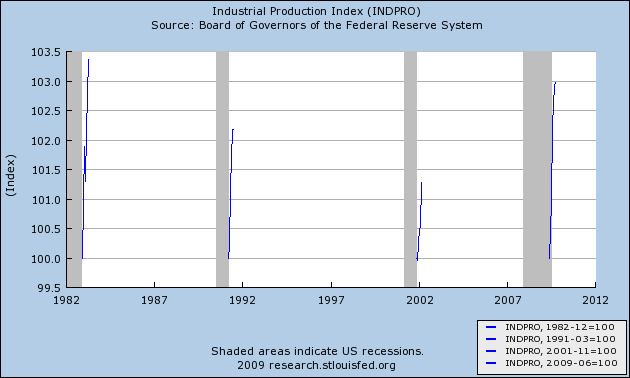

The same can be said for Industrial Production, which is growing at a rate well in excess of the two "jobless recovies" and is close to that of 1983's V-shaped recovery:

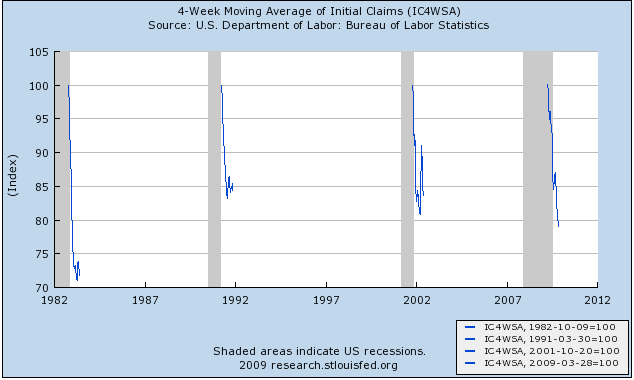

In at least one repect, the employment situation is also improving in a way more consistent with a V-shaped scenario -- namely, layoffs. Here is a graph of Initial Jobless Claims showing declines on a percentage basis from their recession peaks.

This data on this graph does not include last week's or this morning's jobless claims -- which put those claims down 23% from their peak, which is very different from the "jobless recoveries" and very much resembles 1983.

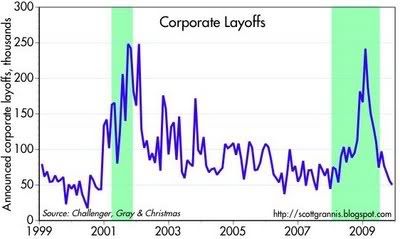

That layoffs are abating, at least at larger firms, is also demonstrated by the latest data from Challenger's jobs survey (released yesterday)hat tip Scott Grannis:

Note that announced layoffs are already down to where they were in late 2003 and 2004, after the "jobless" part of that recovery had ended.

Global trade is driving that portion of the economic expansion:

which confirms something I've noted for a while now: the US consumer used to be the "locomotive" of global recovery -- this time s/he is the caboose, bringing up the rear.

Contrarily, one thing that is only "recovering" very weakly is housing:

Earlier this decade we had the biggest housing bubble since the 1920's, and while it looks like new home sales bottomed in January 2009, the rate of increase is subpar not only measured by every other post-WW2 expansion, it appears also to be lagging the recovery from the 1933 bottom during the Great Depression (1934 showing an ~35% increase).

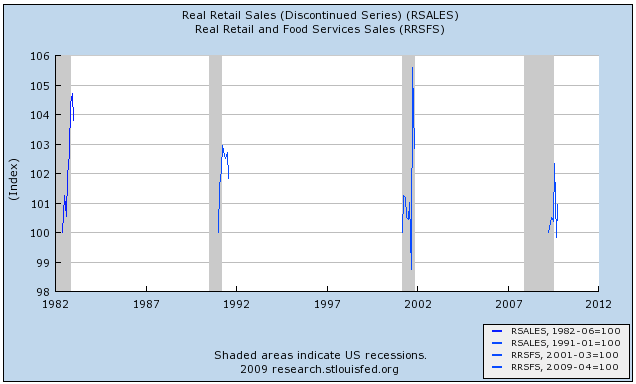

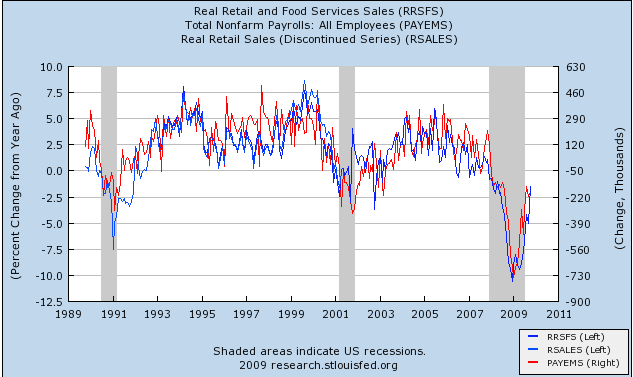

Real retail sales are also improving only at a snail's pace as per the most recent Census Bureau adjustments. Here is a graph comparing the trend in Real Retail Sales since its smoothed bottom in April with the first 7 months of growth during the expansions of 1983, and 1992, and the first eight months of growth in 2001 (September and October 2001 show extreme volativity for obvious reasons so I also included November):

Real retail sales are something of a "Holy Grail" leading indicator for jobs growth. When they have grown at least 2.5% on an annual basis, on average job growth has follwed ~5 months later. That sales growth hasn't happened this year.

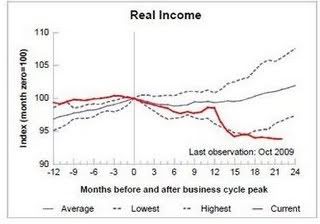

What is definitely not improving at all so far is income and jobs. Here is the latest measure of "real income" as measured by the Federal Reserve:

Real income is still declining, as opposed to virtually every other recession and recovery since WW2.

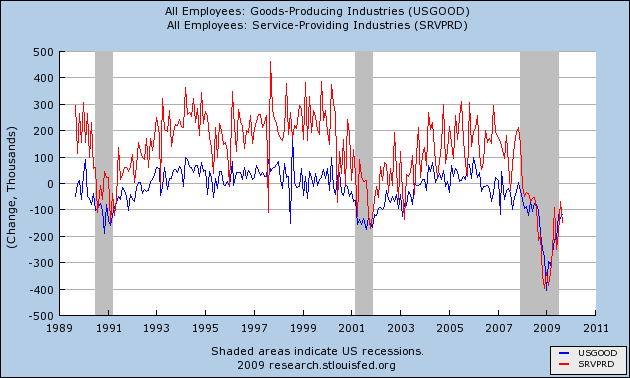

This morning the Institute for Supply Management reported that the services sector of the economy started to contract again in November, and that employment in that sector continued to shrink. This is important because as I've indicated previously, in this "Great Recession" services employment has been particularly hard hit, much moreso relative to manufacturing than in any post-WW2 downturn, as shown on this graph:

For the last 10+ years, the ISM nonmanufacturing employment index has correlated particularly well with job gains or losses. This graph is current through last month:

That services employment is mired in strong contraction argues that the bleeding in that sector is going to continue unabated, at least for now. If there is a (relatively) bright spot here, it is that in this recession, employers have behaved exactly as if they were making employment plans based on year-over-year real retail sales, as shown by this graph:

in which red shows monthly payroll gains/losses, and blue is the year-over-year percentage gain/loss in real retail sales. Unless this holiday season is even worse than last year's, the Y-o-Y% number should turn positive.

In summary: as the Congressional Budget Office recently reported:

(1) the stimulus from earlier this year is almost single-handedly responsible for turning the economy as a whole from contraction to growth, and has probably kept the economy from shedding about 1,000,000 additional jobs; BUT

(2) the stimulus has not been successful in turning around the jobs market into actual growth. While manufacturing (exporting to other countries whose citizens actually have an improving standard of living) has expanded, services in general and retail in particular have shrunk, and are continuing to do so, and that's where 7/8 of Americans have been employed.