In the real world, I am an insurance broker and a small business owner. In these dual roles, I am acutely aware of how difficult it is to for small businesses to find affordable health insurance. This is why I've concluded that any healthcare reform in America that exempts small business is no reform at all.

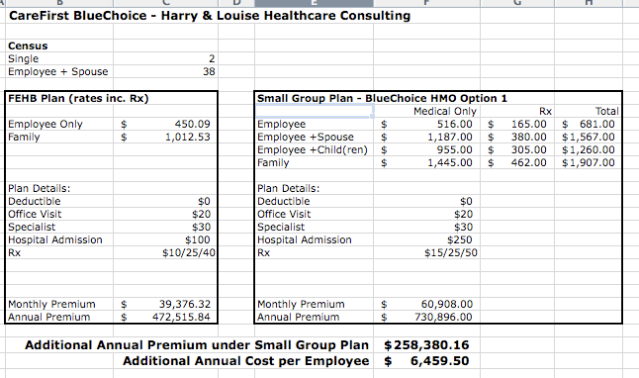

As an exercise to highlight the difference in purchasing power between large organizations and small businesses, I ran the following scenario: what would it cost to insure the 40 GOP senators in a small group plan.

This exercise is possible because community rating for small groups uses very little data. And the little data required to rate this group is public data - date of birth and marital status - found on Wikipedia. I ran this hypothetical business - let's call it Harry & Louise Healthcare Consulting - through the CareFirst BlueCross BlueShield rate model.

And the results? It would cost $258,380.16 more to insure these Senators as a small business than it would cost to insure them in a comparable Care First plan available in the FEHBP. That represents an increase of 55%.

*******************************

According to the Medical Expenditure Panel Survey conducted by the Department of Health and Human Services (and nicely summarized at the Kaiser Family Foundation's statehealthfacts.org), ninety five percent of companies with 50 or more employees offer health insurance, while only 43% of firms with fewer than 50 employees do. And 69% of the uninsured have at least one family member employed full-time.

In a 2008 survey performed by the National Small Business Association, 69% of small businesses expressed an interest in providing health insurance but only 38% of the surveyed businesses offered a plan. Fifty-eight percent of small businesses who were hit with rate increases were unable to provide raises to their employees, and 39% reported holding off hiring new employees.

Insurance is ultimately a game predicated on large numbers. It is easier to absorb catastrophic risk over a large pool of people. Small businesses just don't provide the requisite numbers to spread risk, so their plans must generally have higher premium costs per employee. And this higher cost drives away many small businesses from providing insurance.

Exempting small businesses from any healthcare reform ignores the biggest problem in our employer-based health insurance model - it ends up excluding a significant portion of the uninsured population. As long as the employer-based health insurance model is going to remain the foundation of the healthcare payment system, then affordability of coverage remains a significant hurdle to universal coverage.

***************************

So how do we get out of this fix? Small businesses that fear they can't afford insurance already don't offer it today, so it is understandable that they oppose any employer mandates. They've merely transfered their fear into opposition. The example of the 40 GOP senators drives this problem home is graphic detail. Small businesses already feel screwed by the marketplace. Mandating employer coverage just feels like piling on.

Providing the 50% tax credit is a good start, but it doesn't address the bias that small businesses face - they pay more for the same coverage that larger firms receive.

The common way of overcoming this pricing bias in insurance is through pooling. This is why the public option is so important. Pooling is something the government can do quite effectively with a public option. It is extremely more efficient than pushing individuals into the market to purchase insurance by themselves. It will put small businesses on equal footing with large firms in terms of pricing their health benefits. If we combine this lower face cost of insurance with the proposed tax credit, then we've made significant inroads to affordability for healthcare.

As the NSBA survey noted, small businesses want to offer their employees health insurance. But the healthcare reform efforts won't start gaining traction with small businesses until they see the significant cost advantages they will be provided with a public option. Graphic examples like the one above can drive home the savings small businesses could realize under a public option. It begins to turn the eye of small businesses to doing something they'd like to do - offer health insurance.

Wouldn't the possibility of a 55% discount - before the tax credit - make you open your eyes to the possibilities too?