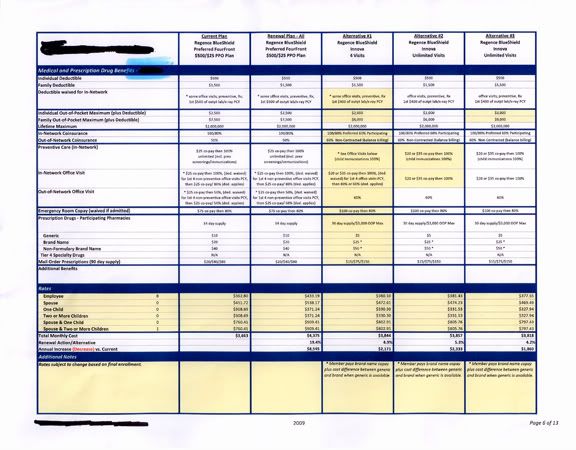

My annual meeting with the two, attractive, suited health care benefits professionals began in the usual way, with me apologizing in advance for anticipated foul language and generally hostile attitude, and them presenting me with a 13 page document that looked mostly like this:

Jennifer Xxxxx, RHU, and Rebecca Xxxxxx, SPHR opened the discussion, as always, with "good news and bad news".

The bad news being, as always, a huge increase in cost of our existing health plan for my small business comprised of 11 employees. This year that increase is 19%. It would have been a mere 4.5%, I was told, if not for the unlucky circumstance of my staff getting a year older. As it were, some of our employees have unfortunately slipped into the next age bracket. Having neglected to fire, as any shrewd and frugal entrepreneur would, some of my long time employees in favor of younger ones, I am presented with an $8,350 annual increase in health insurance premiums.

(I don't recall the excuse for the 22% proposed increase by Premera last year, all I remember is we dumped them for the more "reasonable" Regence plan which, nevertheless, at the time represented both an increase in cost and decrease in benefits.)

The good news, as always, was "we have options", a euphemism for passing more of the cost of health care onto our employees, who are already burdened with a $1080 aggregated annual payroll deduct (25% of the premium), 100% of premiums for additional family members, a fee so outrageous, no employee other than me opts for (more on that later), plus a $500 plan deductible, co-pays for office visits, tests, procedures, drugs, etc., and Lord knows what exclusions.

Jennifer works for Xxxxx Benefit Services, Inc. as a Health Insurance "consultant", meaning the various insurance deniers providers – Premera, Regence, Aetna, etc., pay her company a commission to enroll groups into their plans.

Rebecca works for the employee benefits/payroll company to whom we outsource virtually all of our human resource management functions: Payroll and related taxes, 401K, Cafeteria 125, health insurance administration, vacation accruals, employee orientation and handbooks, and so forth.

Basically, we contract with Rebecca's company to consult with the benefits consulting company in order to figure out which insurer and plan to contract with to provide health insurance for our employees. Their salaries are paid, ultimately, through the fees my company pays Rebecca's company, and the premiums we pay health insurers to screw cover their asses our employees.

The reason we need Rebecca's company (and not just a payroll service) is that the health insurance administration for our little business became, over the years, too burdensome for my partner and I to handle. Those annual renewals came around so fast. There were countless meetings with countless numbers of consultants, new enrollments, cancellations, COBRA, as well as the constant, relentless employee questions and complaints to field, investigate, and follow up on. And there wasn't just one health insurance plan to renew/manage every year. There were three: One for medical, one for dental, and one for vision, for which the various monthly premium statements, I swear, somehow managed to appear twice that often.

I've distilled all that down to one or two meetings a year. The endless stream of employee questions and complaints go to Rebecca, not me, and she gets to explain to my staff why it is actually good news that once again we are changing providers and that they are going to have the privilege of paying still more for even crappier health insurance coverage. ("Many companies are dropping health insurance altogether, if they even provided it in the first place...competitors are laying off employees and closing plants, your employer hasn't laid off anyone, even though sales are down 13% over the prior year, which itself was very nearly a disaster...").

As wonderful as my employee benefits company is (and their fees are reasonable), the health care expense for my family is nonetheless extraordinary, and illustrative of the inviability of continuing a market based health care system that relies on for-profit insurance providers.

Get this, Congress: Factoring in the 19% increase for my Regence health plan, which costs us plenty for deductibles and co-pays, and adding the separate VSP vision plan (which is pretty good relative to the small premium, actually) and pathetic Met Life dental insurance, the total cost for health "insurance", not health care, mind you, but health care "coverage", is, as proposed by two accredited benefits professionals, for my family of four, on an annual basis, $18,070!

Yeah, we have the greatest health care in the world. Lucky us!

I need to make a decision on health insurance in the next couple of weeks. Right now I am leaning towards dumping Regence for an Aetna plan, with a $1500 deductible, and picking up 100% of the premium with no payroll deduct, rather than a 75/25 split with employees. The decrease in premiums associated with the increase in deductible will make up for no longer sharing the premium expense with employees.

Currently, employees pay $90 per month ($1080/year), plus a $500 deductible, for an annual cost of $1580 before any healthcare is paid for by the insurer. If we go to a $1500 deductible, with no payroll deduct for premiums, they are no worse off, and employees who don't require medical services will pay nothing.

One problem with this strategy, is that employees, either because they can't afford it or choose to roll the dice, may deny themselves the "best healthcare in the world" because the first $1500 comes out of pocket. If so, they risk becoming one of the tens of thousands of people that die every year in this country due to lack of access, ability, or willingness to seek treatment. (Isn't the "ownership society" a wonderful thing?)

Excluding fees paid to my employee benefits company, and premiums and other costs born by employees, I currently pay $33,000 per year to provide a "benefit" that increasingly engenders angst, stress, and dissatisfaction in my employees. The sum total of the administrative burden of FICA, Federal Income tax withhold, sales and B&O tax, State Industrial, Employment Security, OSHA, fire and electrical regulations, King County Hazardous Waste, et al, may not exceed the burden of providing health care for my employees.

Why isn't the U.S. Chamber of Commerce demanding single payer universal healthcare on our behalf? Why aren't the Republicans that abhor needless bureaucratic burden on businesses demanding single payer?

When people find out I'm a small business owner and a Democrat, often as not I get this perplexed stare, telepathing "you own a business and are a Democrat? WTF? Are you stupid"?

Well, somebody is stupid. I suppose it very well could be me.