Simon Johnson on the Doom Cycle (MMBM) from Roosevelt Institute on Vimeo.

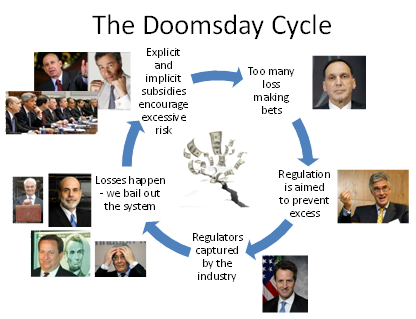

A succint explanation of consumer abuse and corporate socialism and how it perpetuates the doom cycle.

From The Doomsday Cycle by Simon Johnson and Peter Boone:

Given the inability of our political and social systems to handle the hardship that would follow economic collapse, we rely on our central banks to cut interest rates and direct credits to bail out the loss-makers. While the faces tend to change, each central bank and government operates similarly. This time, it was Mervyn King, Gordon Brown, Tim Geithner and Ben Bernanke who oversaw policy as the bubble was inflating – and are now designing our rescue.

When the bailout is done, we start all over again. This has been the pattern in many developed countries since the mid-1970s – a date that coincides with significant macroeconomic and regulatory change, including the end of the Bretton Woods fixed exchange rate systems, reduced capital controls in rich countries and the beginning of 20 years of regulatory easing.

The real danger is that as this cycle continues, the scale of the problem is getting bigger. If each cycle requires greater and greater public intervention, we will surely eventually collapse.

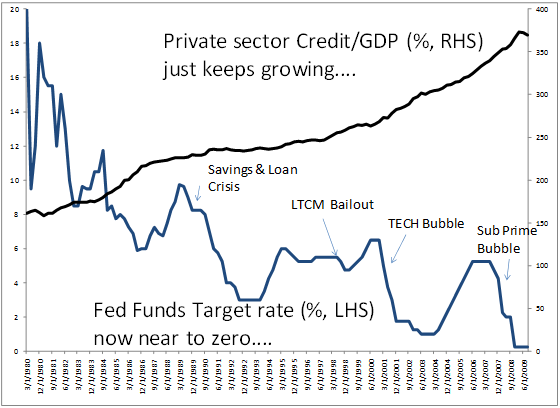

Since the '80s, private sector debt to GDP has kept growing. So did the transfer of risk to society as a whole because of our regulatory system. There's nothing to discourage the excessive risk-taking and gambling that the system enables despite attempts at "regulatory oversight". The cycle will repeat itself.

What will happen when the next shock hits? We believe we may be nearing the stage where the answer will be – just as it was in the Great Depression – a calamitous global collapse. The root problem is that we have let a ‘doomsday cycle’ infiltrate our economic system.

The solution? Rejecting the argument by the "too big to fail banks" that we actually need them.

We believe that the best route to creating a safer system is to have very large and robust capital requirements, which are legislated and difficult to circumvent or revise. If we triple core capital at major banks to 15-25% of assets, and err on the side of requiring too much capital for derivatives and other complicated financial structures, we will create a much safer system with less scope for “gaming” the rules.

Once shareholders have a serious amount of funds at risk, relative to the winnings they would make from gambling, they will be less likely to gamble. This will make the job of regulators far easier, and make it more likely our current regulatory system could work.

... Today, Bank of America and the Royal Bank of Scotland are each priced to have just 0.5% annual risk of default above their sovereigns during the next five years in credit markets. This is a remarkably low implied risk considering that both banks were near to collapse just a few months ago. Creditors are clearly very confident that they will be bailed out again if necessary. Indeed, they are more comfortable lending to large risky banks than to many successful corporations.

In a nutshell, nothing's changed at the policy level and the next collapse will be bigger than this one.

Edited to add:

Here's what Joseph Stiglitz

and Elizabeth Warren had to say: