March nonfarm payrolls were just released. +162,000 jobs were added in March. Subtracting 48,000 Census jobs, the economy still added 114,000 jobs! January was revised up +14,000, and February up to -14,000. Had there not been blizzards on the east coast, February may well have been positive as well.

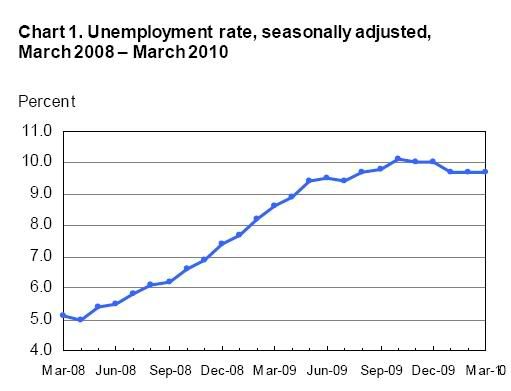

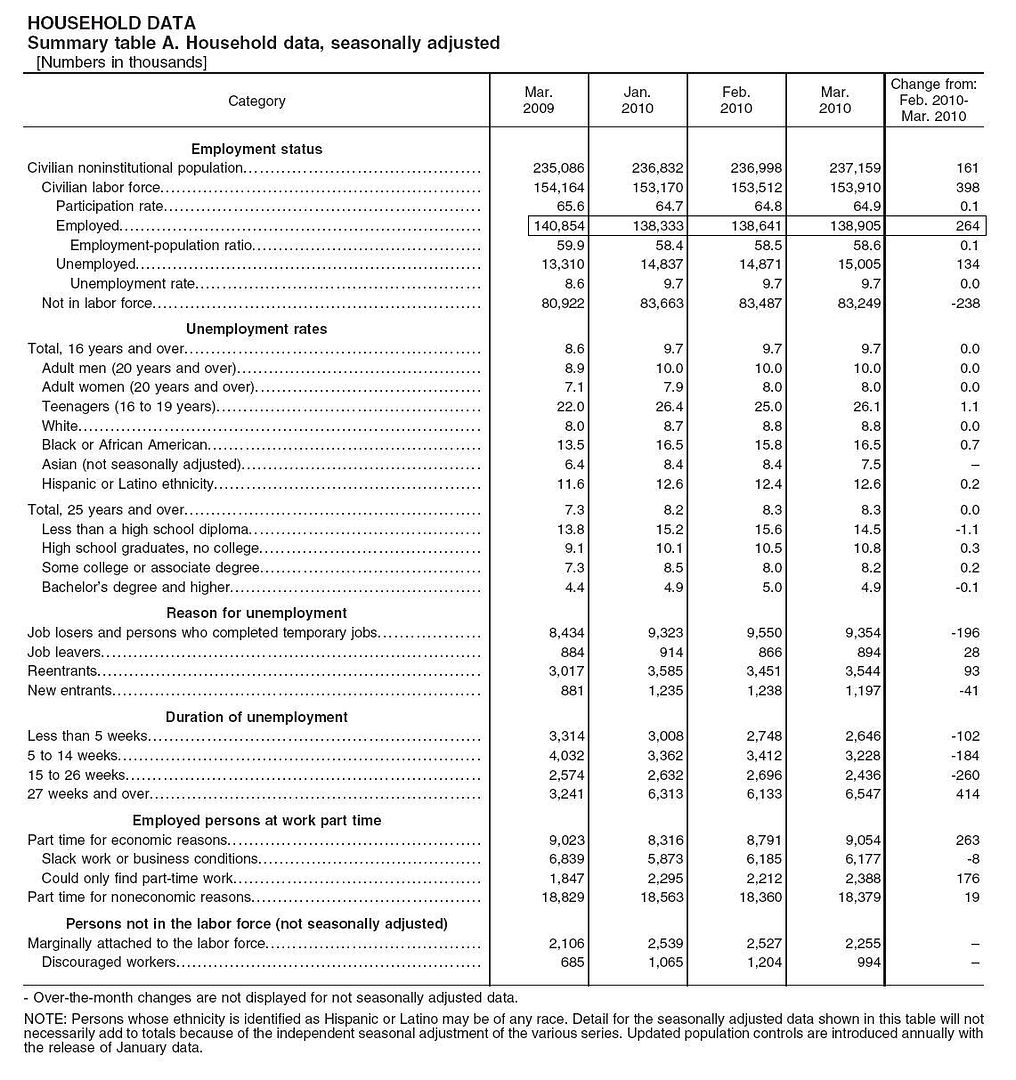

The separate Census Bureau household survey showed +264,000 job growth. Unemployment remained the same at 9.7%. What is particularly positive is that it did so even though +398,000 people were added to the labor force, and the labor participation rate increased to 64.9%.

There was further good news in the establishment report in that the workweek increased to 34.0 hours from 33.8. Temporary hiring also increased +40,000. A total of +313,000 temporary jobs have been added to the economy in the last 5 months.

Unemployed persons in all durations between 1 and 26 weeks declined. That is more good news, because it means fewer unemployed "in the pipeline." The only negative here is that long term unemployed over 26 weeks continued to increase, by +414,000 in March.

The only other negative in the report was hourly earnings, which declined ( - 0.1%).

This is unabashed good news. Jobs have finally turned the corner.

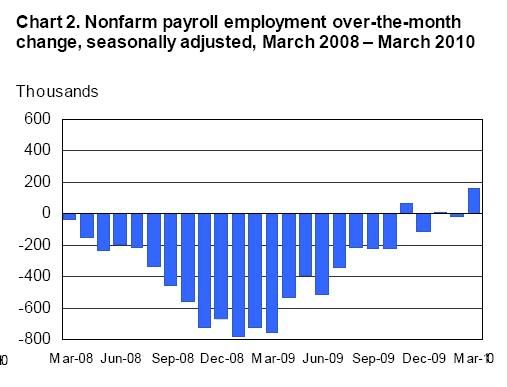

As indicated above, the BLS reported that +162,000 jobs were added to the economy in March. January and February were also revised upward, as shown in this graph:

The unemployment rate held steady at 9.7%:

I'm not sure how legible this chart is going to be, but it indicates from the household survey that +264,000 more people reported they were employed in March than in February (unlike the BLS survey, the household survey does not include any "birth/death" noise).

Back in September, when monthly job losses in excess of 200,000 a month were being reported, I predicted that the bottom in jobs would be in November or December, +/- one month. With today's revisions, it appears my call was correct by the skin of its teeth! Jobs actually bottomed in December, and retested that exact low in February before rebounding strongly this month. February will be revised again next month, so I could go back to being wrong then.

This Recovery has turned out to be much less "jobless" than the 2002-03 recovery so far. In that case it took about 2 years for employment to bottom out, and a similar amount of time for the unemployment rate to bottom. If ECRI (the business cycle institute which has had a stellar record calling this recovery) is correct, in terms of the unemployment rate, this recovery has been like prior V shaped ones, as the umemployment rate peaked in October, only 3 or 4 months after the trough in the economy as a whole. Much like 1992, where jobs started to get added only a few months after the trough, with today's revisions the bottom was reached 5-6 months after the trough, and a strong turnaround has begun 8-9 months after the trough.

The big issues now will be (1) sustainability, and (2) whether enough jobs are added monthly - at minimum 100,000 a month - to bring the unemployment rate down signficantly. And of course, there remain the issues of wage growth and the types of jobs being created, as to which more pessimism is probably warranted.

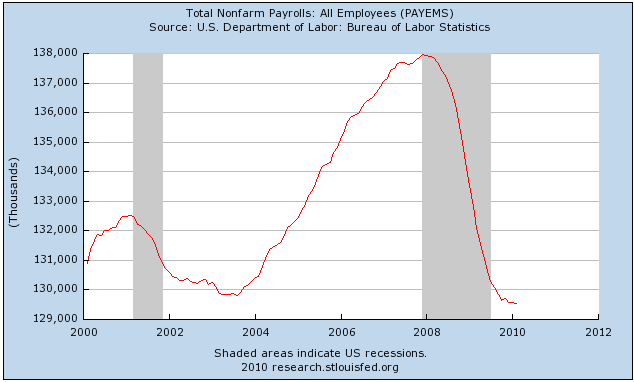

I would like to close by reiterating the closing of my diary Monday. We have turned the corner and are actually adding jobs in the economy as a whole, there will continue to be strong drag on growth from a pitiful construction sector for some time to come. This final graph shows just how high a cliff we have to scale, just to get jobs back where they were three years ago:

But we have begun the climb.