The first quarter advance GDP report was released last Friday. At +3.2%, the report showed an amount of growth that had been expected. As more complete data is available, is is usual there will be revisions at the end of this month and next month.

Probably the most welcome part of the report was the return of the consumer, as personal consumption expenditures grew by 3.6% compared with the last 3 months of 2009. One of the key issues in this recovery is whether it can be sustained in the absence of government stimulus. In the first three months of this year, at least, consumer spending pointed towards a "yes."

I have devoted most of my blogging attention in the last year to the cause of jobs, jobs, jobs -- as in when will they start to return and how robust will a return be. The good news as to jobs from the GDP report is that it confirms that we can expect continued job growth, and it is confirming the strong signal that has been sent by real retail sales that job growth is likely to be stronger than most people expected. A fuller discussion below the fold.

I. Econoblogosphere reaction to the GDP report

Most of the reaction to the report was mixed. In general, optimists were reasured by strong consumer growth. Pessimists were concerned by the end of inventory liquidation. Here's a nice roundup of opinions by Phil Izzo:

• The 3.2% rise in GDP (annualized) in the first quarter confirms that the U.S. economy continues to recover but the growth path ahead will remain bumpy. While growth is less than half of the robust 5.6% pace in the last quarter of 2009, the underlying dynamic is actually healthier and better balanced: More of the rise in GDP came from domestic demand and less from an inventory correction. Still, the strength and durability of this recovery remain in question, as the economy sails into strong headwinds over the next few quarters....– Bart van Ark, Conference Board

• Consumer and business spending are the key elements of this data for me, and, from that standpoint, I see this release as strong, even though real domestic demand came in two ticks below my projection... Consumer and business spending should remain strong, construction will perform better (look for a weather rebound and an additional boost to housing from the tax credit), inventory replenishment should continue to add to output. –Stephen Stanley, Pierpoint Securities

• Businesses went from liquidating [inventories] in the fourth quarter at a very slow rate to building stockpiles in the first quarter of the year at a healthy rate... Final sales of domestic products rose by only 1.6% even after the huge incentive offered to individuals to spend during the quarter... –Steven Ricchiuto, Mizuho Securities

• Inventories added 1.6 percentage points to Q1 growth (0.3 more than anticipated). ...Still, the pace of accumulation was very modest (+$31 bil) and, after a brief pause in Q2, we see plenty of room for additional inventory restocking during the second half of the year and into 2011. –David Greenlaw, Morgan Stanley

• Prospects of double-dip recession can be firmly taken off the table. More encouraging is ...the release of pent-up demand by consumers which resulted in a 3.6% rise in personal consumption. –Joseph Brusuelas, Brusuelas Analytics

• Consumers led GDPgrowth .... Truth is, real final sales of domestic product of 1.6% and a 1.7% average in the past three quarters remains anemic considering the decline that preceded it and the amount of monetary and fiscal stimulus. –Steven Blitz, Majestic Research • That all important 70% of domestic economic activity (the consumer) expanded expenditures by 3.6%, which was actually slightly above our own expectations.... Consumers’ interest in durables was heavily constrained by a lack of credit availability through mid-2009; while credit is now accessible, consumers don’t seem interested in borrowing, but they’re nonetheless purchasing durable goods at a pace not seen since 1Q 2007. –Guy LeBas, Janney Montgomery Scott

• This is an encouraging report . The cyclical components of GDP one would hope to see rebounding at this stage of the recovery - consumer spending, equipment and software investment and inventory accumulation - are doing so, although the drag from other components, including investment in structures and state and local government spending, is likely to temper these gains for some time. –Peter Newland, Barclays Capital

• The good news is that the economy continues to recover as real GDP expanded for the third consecutive quarter and has grown at an average pace of 3.7% since the recession trough (by our estimates) in the second quarter of 2009. The bad news is that this pace of growth has not been sufficiently fast to make major inroads into unemployment.... Final demand growth needs to pick up to sustain this growth pace through 2010 (which is our forecast) and there are encouraging signs in consumer spending and business equipment that this is occurring. – RDQ Economics

Prof. James Hamilton of UCSD writing at Econbrowser, was disappointed but also saw cause for optimism:

[T]he details behind the 3.2% growth for 2010:Q1 are disappointing. Half of the growth came from the fact that firms were no longer drawing down inventories and have started to rebuild them slightly; real sales of final goods and services only increased at a 1.6% rate during the quarter, which would be an anemic rate in normal times and is particularly disappointing at this point in a recovery. And even 3.2% growth in GDP may not be enough to make progress in bringing the unemployment rate down....

Spending declines by state and local governments subtracted half a percent from the GDP annual growth rate, and residential housing another third of a percent. Nonresidential fixed investment and exports made modest positive contributions to first quarter growth, but I'd really like to be seeing them contribute much more.

But I suppose an optimist could see in all this the potential for much better numbers to come once the recovery gets on track. And even if growth of real final sales remains tepid, Inventory restocking could continue to make a big contribution to GDP growth the rest of this year.

Blogger Calculated Risk saw the same need for job and income growth:

The peak of the stimulus spending is in Q2 2010 (right now), and then the stimulus spending starts to taper off in the 2nd half of 2010. So underlying demand better increase soon - and that means jobs and incomes going forward.

The most pessimistic pundit was Dean Baker:

If we pull out inventories, final demand grew at a 1.6 percent annual rate, almost exactly the same as the 1.7 percent rate in the 4th quarter of 2009 and the 1.5 percent rate in the 3rd quarter of 2009.

In other words, we are still looking at a very weak economy ...and one which may not even be growing fast enough to create any jobs at all.

My co-blogger Bonddad had the following take:

GDP is composed of PCEs -- personal consumption expenditures, investment (residential and non-residential), a net of imports and exports and government spending. Let's take each of these areas in turn.

Personal Consumption Expenditures:

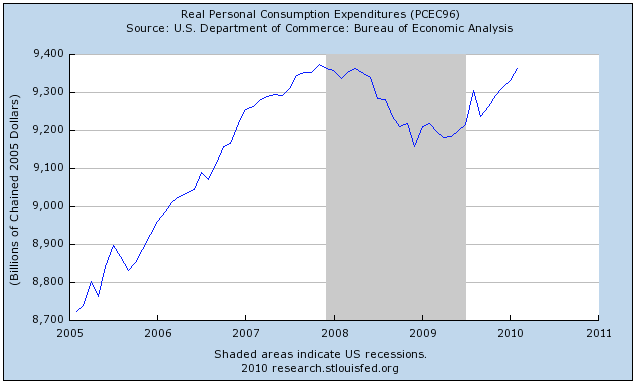

Real personal consumption expenditures increased 3.6 percent in the first quarter, compared with an increase of 1.6 percent in the fourth. Durable goods increased 11.3 percent, compared with an increase of 0.4 percent. Nondurable goods increased 3.9 percent, compared with an increase of 4.0 percent. Services increased 2.4 percent, compared with an increase of 1.0 percent.

These are strong numbers and indicate the consumer is "back."

II. The good news: the GDP report confirms other, more leading data, that job growth will continue

Personal consumption expenditures generally track closely with retail sales, and here is how they looked through February:

With personal spending in March increasing by 0.6%, and PCE prices only increasing 0.1% (reported just this morning), that graph only looks better with one more month added.

For a year now, I have been pounding on the fact that growth in the Leading Economic Indicators leads to GDP growth, leads in turn to job growth.

In a diary a couple of weeks ago I said tht Strong Job Growth Looks Likely for the Rest of 2010. In it, I noted that March Leading Economic Indicators were reported up 1.4%, meaning for the last 12 months the LEI are up ~12%! This is the strongest reading in two decades:

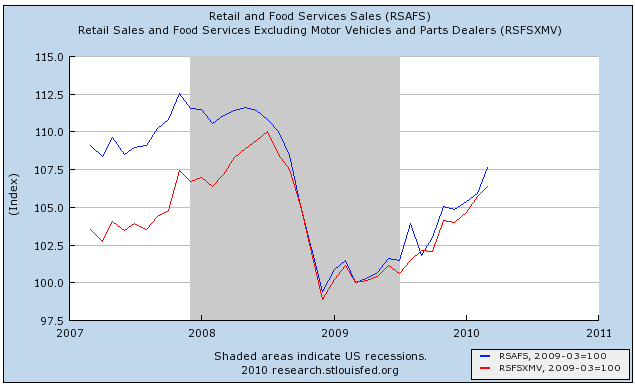

I further noted that retail sales were reported up 1.6% including autos due in large part to Toyota's rebates (blue line), and up 0.6% ex-autos (red line). This accelerates the return of the consumer since the bottom a year ago:

In the past I have pointed out just how important retail sales adjusted for inflation (a/k/a real retail sales) are for future job growth. With the economy finally adding jobs, this strong showing has major implications for job growth for the rest of this year, indicating that it is likely to be stronger than most suspected.

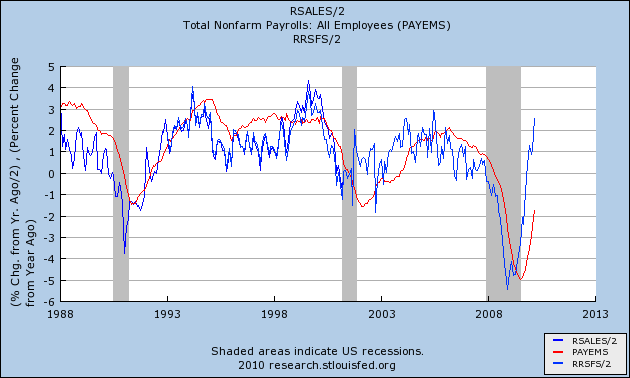

Because real retail sales are historically much more volatile, these graphs take the YoY percentage change in real retail sales and divide by 2 (blue line), which historically yields a very close fit with YoY payroll changes (red line).

Here it is for the two "jobless recoveries" and up until now:

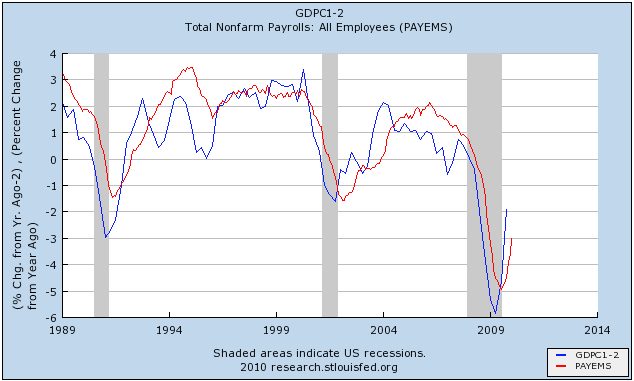

I also looked at GDP and compared it with payroll growth, noting that YoY percentage changes in GDP (minus two percent) appears to lead payroll growth:

The problem is, however, that GDP is only reported quarterly, so by the time you learn the GDP for a quarter (like Q1 2010, you already know what the payroll growth was. At best, YoY GDP when initially reported, can give guidance about payroll growth over the next couple of months.

Firday's GDP does exactly that. Here is what the graph of GDP vs. payroll growth over the last 5 years looks like, with Friday's +3.2% added:

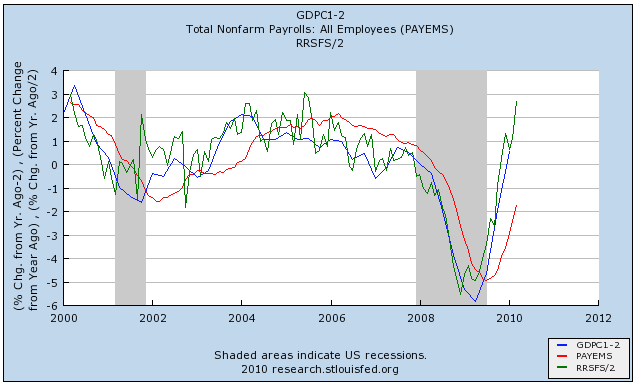

Now let's put together both the latest real retail YoY growth numbers (green), with the updated GDP through Q1 2010 (blue), and compare with YoY payroll growth:

In summary, the good news from Friday's GDP report is that it continues to track nicely with real retail sales, and confirms that job growth can be expected to continue. Put another way, we should expect the red line to continue to move up towards the present values of the blue and green lines. While any given month's payroll growth (0r not) can be an outlier, in general we should expect good job growth for the next few months.

In my next diary, I'll look at some of the problem issues shown by the latest figures, including wage stagnation, Oil prices, and other headwinds.