Warren Buffett's holding company, Berkshire Hathaway, owns a variety of "meat and potatoes" companies, from furniture to utility to railroads. Thus Warren Buffet has a unique perch from which to view the economy.

Here's what he said yesterday:

Based on the performance of his companies, he said there has been a 'big pick-up' in manufacturing this year, although it's not as productive as it was three years ago. He believes the retail market in the US has not picked up as much yet as manufacturing, but the sale of luxury goods is improving.

Overall, he pointed out the US economy has picked up and is set for a rapid 'V-shaped' recovery:

'There was a lot of strength in March and April. It won't be translated into huge changes in unemployment soon, but the economy is starting to move.'

Manufacturing data from yesterday and today bear that out.

This has been a "Bifurcated Recovery", where the industrial and manufacturing sector of the economy is rebounding sharply, while that part of the economy most identified with Joe Sixpack is either rebounding very slowly (jobs, finally) or not at all -- (income).

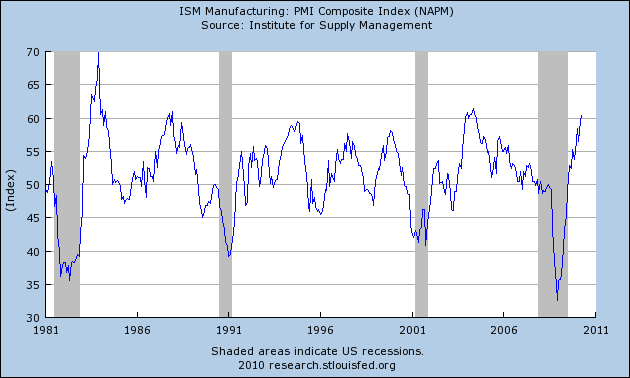

Yesterday and this morning's data confirmed that manufacturing continues to be in a V-shaped recovery. The ISM manufacturing index came in at 60.4 showing fast expansion in the manufacturing sector.

Almost all of its components likewise showed increasingly strong expansion. Inventories continue to shrink, at a faster rate. New Orders are growing very fast at 65.7. Supplier deliveries are falling further behind (a good sign).

And most on point, employment at 58.5 showing not just growth, but faster growth. For manufacturing, this is like the V-shaped recoveries of the 1970s and 1982-3, and not at all like the weak recoveries in 1992 and 2002.

Likewise, auto sales were reported at 11.2 vehicles on an annualized basis, holding on to two-thirds of their strong advance from February to March.

(courtesy Calculated Risk)

Recall that in February annualized sales were 10.3m (as Toyota's sales fell dramatically). March's 11.8m annualized sales were fueled by the resulting Toyota incentives. In April Toyota dropped most incentives, making April the first "clean" auto report since January. Spencer at Angry Bear contends that, as gas prices go up as a share of disposable income, car sales go down. Thus, this was a good number, as it means that gasoline prices have not yet caused a reversal of the improving trend in car sales.

This morning new factory orders blew out to the upside:

New orders received by U.S. factories jumped ... 1.3 percent after an upwardly revised 1.3 percent gain in February, initially reported as a 0.6 percent rise, the Commerce Department said....

When transportation orders were stripped out, orders surged 3.1 percent, the biggest gain in almost five years. Excluding defense, factory orders were up 1.3 percent.

Non-defense capital goods orders excluding aircraft, viewed as an indicator of business confidence, leaped 4.5 percent, the steepest increase since December 2007.

Finally, it is worth noting that for the second month in a row, withholding taxes were up -- +4% year over year -- in April.

In summary, while Jobs have only finally started upward, and Income is still mired in recession, the V-shaped manufacturing recovery is continuing. The ISM employment increase is particularly welcome, and shows that the manufacturing recovery is leading to jobs.

The ISM nonmanufacturing index will be reported tomorrow, and will give us our first peak at April hiring in the services sector.