What would you say to an insurance system in which those who pay more in premiums receive a payout which is 17% lower than those who are protecting identically-sized assets?

And what if in that same insurance system a person who paid not one dollar into the monetary pool, received a month payment which is 38% higher than a person whose years of payments entitled them to a monthly stipend?

And what if that perverse result violates not just basic fairness, but shatters the underlying philosophy of the insurance system?

Well, we have such a result in the United States: it's the Social Security benefit system which was designed for family and income patterns which are now the exception, rather than the norm, in the United States.

§ § § § § § § § § §

Two foundational principles underlie the Social Security benefit system: equity — that those who contribute the same amount should receive the same benefits; and adequacy — that benefits should be sufficient to keep beneficiaries from poverty.

The equity principle was built in to Social Security with the implementation of the dedicated payroll tax. Franklin Roosevelt said

I guess you're right about the economics, but those taxes were never a problem of economics. They are politics all the way through. We put those payroll contributions there as to give the contributors a legal, moral, and political right to collect pensions…With those taxes in there, no damn politician can ever scrap my Social Security program (Schlesinger 1958, 308–309) quoted at U.S. Social Security at 75 Years: An International Perspective)).

However, true, actuarial equity was left behind with the implementation of spousal and dependent benefits in 1939 — an effort to address the other principle of Social Security benefits, income adequacy. At the time, 80% of households consisted of a married couple with children, and 85% of those marriages had a sole breadwinner. The spousal and dependent benefits were a necessary addition for the support of widows who had no independent source of income. The rationalization was that women had contributed to society by raising children, although there was no "motherhood" requirement to collect the spousal benefit. In the 1960s, divorced spouses in marriages lasting over 20 years were enabled to collect a full spousal benefit, and in 1977 the years of marriage required to collect a spousal benefit was reduced to 10.

Much has changed since then. Today, 77% of households in the top quintile of earnings rely on two workers to achieve that level of earning. One of the results of this change in family earning patterns is the shattering of the fundamental principles of Social security:

A high wage earner receives benefits that replace 78 percent (Koitz, 1996; Century Foundation 1998). But research demonstrating the redistributive impact of Social Security benefits has been based solely on retired worker benefits. Thus, while retired worker benefits redistributes from higher to lower lifetime earners, spouse and widow benefits redistribute from single to married persons, from employed to unemployed persons, and from lower earners to higher earners (Harrington, Meyer, 1996).

Linking Benefits to Marital Status: Race and Diminishing Access to Social Security Spouse and Widow Benefits in the U.S.

First, a primer on how a couple's Social Security benefit is calculated. A worker has the right to a primary benefit based on his§ own earnings record and, additionally, a spousal benefit§§ equal to one-half of the primary benefit. If the spouse has her own earnings record she can not receive both the full spousal benefit and her own primary benefit. Instead, she receives, in addition to her primary benefit, that amount, if any, which is the difference between the spousal benefit less her primary benefit. Thus, if the higher income partner qualifies for a primary benefit of $2,000 (PB1), and his spouse for a primary benefit of $750 (PB2), the spousal benefit (SB) would be expressed by the equation (PB1*.5)-PB2, or $250. Combined, the Social Security benefit for this household is PB1+PB2+SB — $3000.

Upon the death of one spouse, surviving spouse receives either the full higher-waged spouse's Social Security benefit (PB1), or a combination of the difference between her own benefit (PB2) and her spouse's benefit:PB2+(PB1-PB2). For our couple, the formula would be $750+(2000-750), or $2000.00. In this household, the surviving spouse's Social Security benefit has been reduced by one-third, exactly the same result as if the surviving spouse had never qualified for her own benefit at all.

The inequity arises between households when the same amount of income is earned in different percentages between the two spouses. The formula used by Social Security favors the single-earner income household, and smaller the difference between the higher and lower income in the household, the less the household receives in benefits, and the higher the percentage of Social Security income lost to the surviving spouse.

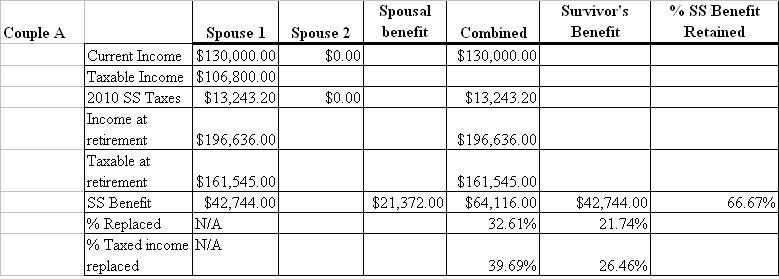

To demonstrate, let's look at three households, each of which had an income of $130,000 in 2010. I have used Social Security Benefit Calculator at tax.com at tax.com, using the assumption that each person is currently 52 years old, will retire at full retirement age of 67, with salary increase rates of 3%, and an inflation rate of 3.1%. Using these assumptions, the final year's salary will be $196,636.

With Couple A, the husband is the sole breadwinner; his spouse does not work outside the home.

Only the first $106,800 of Spouse 1's earnings are subject to Social Security taxes, so the chart shows income replacement rates for both the total $196,636 in ending income, and the taxed ending income, calculated using the same 3%/3.1% salary increase/replacement rates.

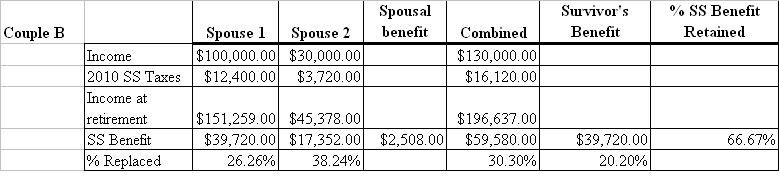

In Couple B, the $130,000 earned in 2010 was split between the spouses' jobs. Spouse 1 earned $100,000 and Spouse 2 worked part-time and earned $30,000.

In 2010, Couple B paid $2,876.80 more in Social Security taxes than Couple A, yet their benefit is less by all measures: $4,536.00 less in dollars, 2.31% less in percentage of full income replaced, and 9.39% less in taxed income replaced. Further, the survivor of Couple B will have a far smaller percentage of income replaced than the survivor of Couple A — 20.20% as opposed to the 26.46% of Couple A's taxed income.

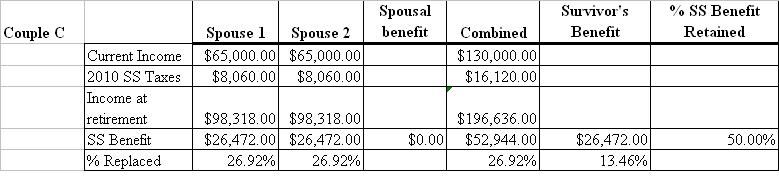

But, at least in this scenario, the Couple B survivor retains the same 66.67 percentage of Social Security benefits as the Couple A survivor. When we look at Couple C, each of whom contributed $65,000 to the total household income of $130,000, the outcome is even more inequitable.

Couple C also paid taxes on the full $130,000 in 2010 income. However, because their income was equal, Couple C will receive $6,636.00 less than Couple B, and $11,172.00 less than Couple A. Couple C's income replacement level is 26.9% and, at the death of one spouse, the surviving Couple C spouse loses 50% of the household Social Security benefit, resulting in a household income replacement level of only 13.46%.

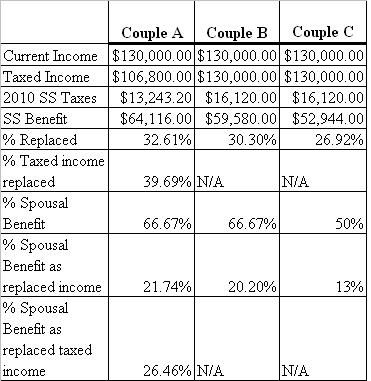

This is the comparison of the three couples earning the identical amount in 2010:

§ § § § § § § § § §

§ § § § § § § § § §

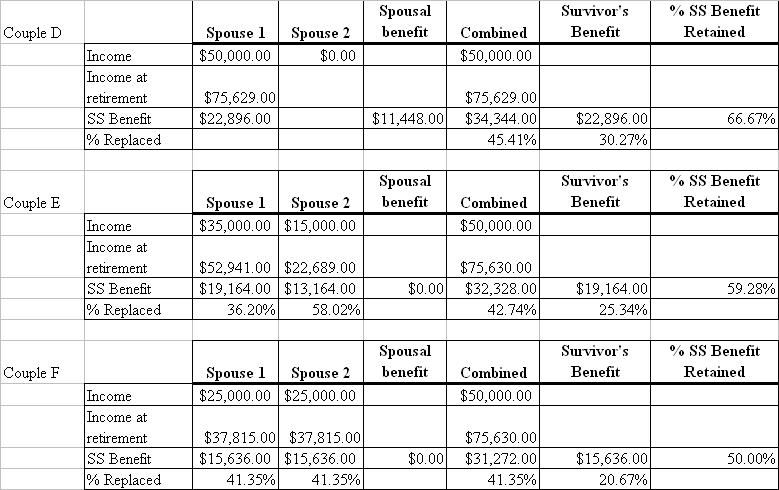

One would suppose, in an effort to keep low-income households and survivors out of poverty, dual-income households wouldn't be penalized by the structure of Social Security benefit calculations at lower income levels. However, the same pattern of diminishing returns prevails at a $50,000 mid-range earnings level:

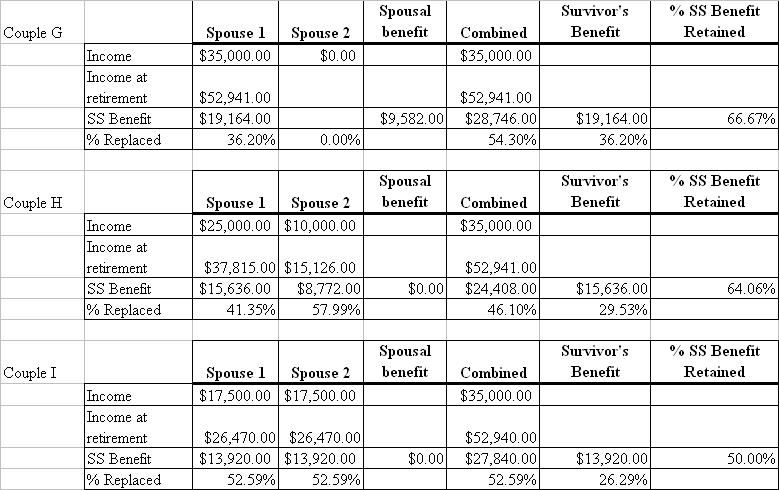

and at the $35,000 low-income earnings level:

Ironic, isn't it, that those politicians who rail against unemployment, disability and welfare benefits as being disincentives to work, say nothing about the structure of Social Security benefits which reward choosing to stay out of the labor force.

The more economically equal a marriage partnership is, the more the couple is punished.

§ § § § § § § § § §

The rules involving divorce and the spousal benefit also can lead to some very bizarre consequences. To qualify for a spousal benefit from an ex-spouse, the marriage had to have lasted more than ten years, and you can not remarry unless you are over 60. Thus, if your marriage lasts only nine and a half years, you're out of luck.

Further, multiple spouses of the same earner can qualify for a spousal benefit, with no reduction in the earner's, or the earner's current spouse's, benefit. Thus, if a Republican senator wants to serially marry four women, and none of those spouses remarry or have become entitled to their own benefit, while that Senator lives each ex will receive the 1/2 spousal benefit, and upon his death four full benefits would be paid.

The ten-years-or-nothing rule causes great problems in a society where divorces are occurring more frequently, and more marriages are failing to last for ten years — or women are bearing children outside of marriage. The pattern of short or no marriage is more prevalent among low-income women (see, generally Women, Marriage and Social Security Benefits Revisited).

The equity and adequacy problems have been known for decades — indeed, before the Greenspan Commission in the early 1980s, policy analysts were discussing the issue. Alas, because any reconfiguring of the system will lead to some retirees having their benefits reduced, the discussion was quietly tabled, and hasn't had much of a public hearing since.

However, the changes in marriage patterns, the lesser support for the survivor of dual income marriages, the overall lower wage structure of all but the highest income workers, and the evisceration of defined benefit pension plans and worker savings, means that in the future the inequities and inadequacies of the Social Security benefit system will become even more critical for all but the wealthiest among us but, especially, for women.

Having crossed my eyes looking at various documents across the web, I believe that a combination of raising the cap on income subject to Social Security taxes, income sharing, and targeted benefit increases, is the best way to meet a better balance between equity and adequacy.

As to the first item, in 1983 about 90% of wages were subject to the Social Security tax. However, with rising income equality as of 2006 that percentage has reduced to 83.6%. Raising the cap back to the 90% level, and having it automatically raise to maintain that level of taxation, will help stabilize overall Social Security funding.

"Income sharing" means simply that — each spouse in a marriage is credited with one-half of the total taxed income during the years of the marriage. Thus, the spouse of 9 years 11 months maintains his or her interest in the income earned during that marriage; the high-income single-earner couple won't benefit at the expense of the non-married individual or dual-earner couple.

"Targeted" benefit increases means that any additional benefits which would granted for people who earn less because of time spent in child rearing or eldercare, because of a pattern of low wage jobs or periods of unemployment would be directed at those who's combined Social Security benefits and other sources of retirement income fail to keep them from poverty. I believe a supplemental benefit which would bring retiree income to 150% to 200% of the poverty level would be appropriate.

Additional Reading:

Earnings Sharing In Social Security: Projected Impacts of Alternative Proposals Using the MINT Model, Iams, Reznik and Tambourini, Social Security Bulletin Vol. 69, No. 1, 2009, Office of Retirement and Disability Policy

How Will Declining Rates of Marriage Reshape Eligibility For Social Security?, Syracuse University Center for Policy Research

Divorce and Social Security; National Center for Policy Analysis, May 1999

Is Poverty a Disappearing Problem For Older Women, Harrington & Herd, Huffington Post, February 20, 2008

Baby Boomer Women: Secure Futures or Not, Paul Hodge, Editor, Kennedy School of Government, Harvard

Women and Social Security, Favrealt, The Retirement Project, December 2005

U.S. Social Security at 75 Years: An International Perspective, Hoskins, U.S. Office of Retirement and Disability Policy

The Treatment of Family and Divorce in the Social Security Program, Steurle, Testimony before Senate Special Committee on Aging, February 22, 1999

Women and Social Security; Google Books Result, Aging: Concepts and Controversies, Harry R. Moody

Raising the Taxable Minimum, Urban Institute

Social Security Spouse and Survivor Benefits for the Modern Family, Fevreault and Steuerle, Urban Institute, March 2007

Social Security Reform and Older Women: Improving the System, Smeading, Estes and Glass, Geronotology Society of America, June 1999

Women, Marriage and Social Security Revisited, Tamborini and Whitman, Social Security Bulletin, Vol. 67, No. 4, 2007

§I'm using traditional gender designations for the simple reasons that trying to remain gender-neutral is clunky, and in a majority of households the husband has a higher aggregate earnings record.

§§There are additional benefits available for dependent children which I am not including in this discussion. It's complicated enough just dealing with the spousal benefit issue.