Rather than running away while Republicans cry "Foul" every time Democrats Accurately describe the Republican/Ryan Budget as Ending the Public Health Insurance Program currently known as "Medicare" and replacing it with Health Stamps, Democrats appear to be doubling-down on their criticism while getting very specific with their new Interactive Map which shows District-by-District how the Ryan Plan Screws You.

Via TPM

Democratic Reps. Henry Waxman (CA) and Frank Pallone (NJ), voters can now see what Democrats say is the direct impact of the Republican plan to turn Medicare into a voucher system on every congressional district in the country.

The Republican's budget would end Medicare as we know it. It also slashes Medicaid programs that cover millions of seniors in nursing homes and provide basic coverage for tens of millions of children," they write. "These Republican proposals would have a devastating impact on every congressional district in the country for generations to come."

You can say that again, and again. In fact. Please do!

Some of the highlights, and lowlights, over the flip.

Since I'm in Los Angeles, that's where I focused and this is what I found in the report.

First there's the argument that "nothing changes" for any seniors currently on Medicare or over the age of 55. That is a Lie.

Higher drug costs. The Affordable Care Act, which Congress enacted last year, reduces drug costs for seniors and the disabled on Medicare by closing the gap in prescription drug coverage known as the “donut hole.” This year, beneficiaries who use between $2,840 and $6,450 worth of prescription drugs will receive a 50% discount on those brand-name drugs; by 2020, the donut hole is completely

eliminated. The Republican budget repeals the provisions in the Affordable Care Act that close the donut hole. This will increase costs for the 10,200 Medicare beneficiaries in the district who entered the donut hole last year. For the average beneficiary, the cost increase will be $520 this year and more than $9,800 over the next decade

Elimination of new preventive care benefits. The Affordable Care Act provides Medicare beneficiaries with free preventive care benefits starting January 1, 2011. The new preventive benefits include a free annual wellness visit and the elimination of any deductible or copayment for preventive services such as breast or colon cancer screening. The Medicare Actuary estimates that the free preventive care, combined with other cost saving measures in the Affordable Care Act such as changes in provider reimbursement, will save the average beneficiary $2,500 over the next decade.

In the aggregate, the Republican plan would increase their spending by $263 million over the next decade.

Ok so these provisions are both already in effect and provide two levels of cost relief to seniors on Medicare that Ryan would REPEAL.

There's also the issue for beneficiaries of Ryan's MediStamps Program - (I absolutely refuse to call it "Medicare" because it's NOT) - of exactly what would it cover?

Elimination of Medicare’s guaranteed benefits. Medicare provides essential guaranteed benefits for all who qualify and enroll – the right to basic health coverage, including coverage for doctor and hospital visits, stays in skilled nursing facilities, home health care, and other health care needs; the right to go to any doctor or hospital that accepts Medicare; and strict protections that do not require older Medicare enrollees to pay higher premiums.The Republican budget eliminates these guaranteed benefits for anyone age 54 or younger. It replaces the entitlement of coverage with a federal contribution of diminishing value that the individual can use to purchase health insurance on the private market.

Unlike current Medicare that guarantees that all persons eligible for the program will receive coverage, Ryan's privatization of care will allow providers to choose what they will cover and what they won't cover. It would take the "Pre-existing Condition" problem that currently exists with Private/Non-Medicare insurance and GIFT that problem to our Seniors.

Yippie!

And of course, there is the fact that Ryan's Plan will effectively price our seniors right out of the Health Care Market with rising costs.

Increased annual costs. The private health plans required under the Republican budget would cost more than today’s Medicare, and the federal contribution provided to purchase the plans would not cover all costs of care. According to the nonpartisan Congressional Budget Office, a newly enrolled beneficiary in 2022 would face out-of-pocket costs that are $6,000 higher than their costs under traditional Medicare. By 2032, these out-of-pocket costs would be approximately $12,000 more than traditional Medicare

Adjusted for inflation that would be about $7000 in Today's Dollars , but that's still pretty horrific. And over time, it gets worse.

According to the Center, the average 54 year-old would need to save an extra $180,000 by age 65 to pay for the extra costs. For today’s 44 year-olds, the additional savings required would be $287,000.

Time to start stuffing the piggy bank now then, oh, and forget about that old pipe dream: Retirement.

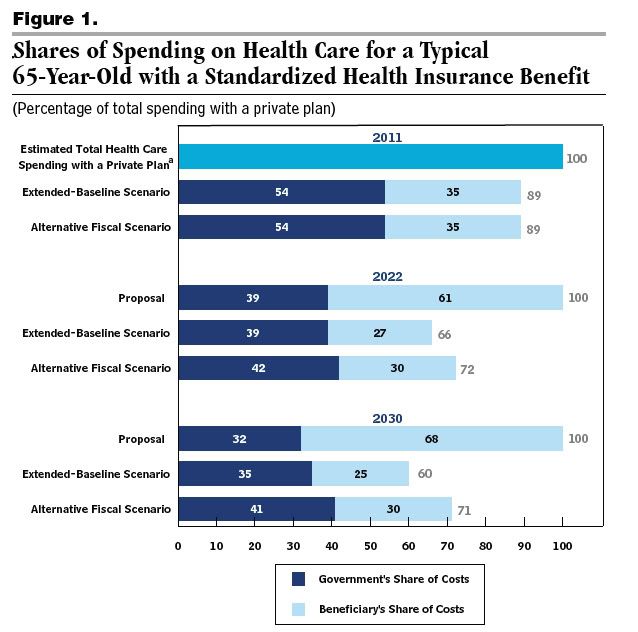

But wait - It gets worse - Ryan's plan increases the Medicare eligibility age from 65 to 67, which means that if you're 55 now you get Medicare in 2022, but if you're 54 now you won't even get your MediStamps until 2024, and they still won't provide you with anywhere near the funds required to actually pay for the cost of care. (The Stamps will only cover about 39% of costs according to this Chart I screengrabbed from CBO's analysis of Ryan's Plan)

Click to Enlarge

Let me also add that Ryan's plan would repeal the current High-Risk Pools which have been implemented in dozens of states to provide care for those who are currently blocked by pre-existing condition bans.

It would repeal the ban on the ability of Health Insurance companies to Rescind Coverage that people have already paid for.

It would repeal the ability for kids as old as 26 to be covered under their parents insurance. Via Gallup

WASHINGTON, D.C. -- Twenty-four percent of Americans aged 18 to 26 were uninsured in January through April of this year, down from 28% in 2010, and fewer than in 2009 and 2008. Americans in this age group became eligible to remain on their parents' health insurance plans under a provision of the new healthcare law that began in September 2010.

It would raise taxes on businesses by removing the 35%-50% tax credit for small businesses which have been used to help allow them to buy health care for hundreds of thousands of their employees for the first time ever.

Blue Cross Blue Shield of Kansas City, the largest health insurer in the Kansas City, Mo. area, reports an astounding 58% increase in the number of small businesses purchasing coverage in their area since April, 2010-one month after the health care reform legislation became law.

“One of the biggest problems in the small-group market is affordability,” said Ron Rowe, who oversees small-group sales for the Kansas City operation for Blue Cross Blue Shied. “We looked at the tax credit and said, ‘this is perfect.”

Rowe went on to say that 38% of the businesses it is signing up had not offered health benefits before.

It would repeal restrictions on excessive co-pays and deductibles of so-called "Junk Insurance" in the small business market that currently exist in the Affordable Care Act.

(2) ANNUAL LIMITATION ON DEDUCTIBLES FOR EMPLOYER SPONSORED PLANS.—

(A) IN GENERAL.—In the case of a health plan offered

in the small group market, the deductible under the plan shall not exceed—

(i) $2,000 in the case of a plan covering a single

individual; and

(ii) $4,000 in the case of any other plan.

The amounts under clauses (i) and (ii) may be increased by the maximum amount of reimbursement which is reasonably available to a participant under a flexible spending arrangement described in section 106(c)(2) of the Internal Revenue Code of 1986 (determined without regard to any salary reduction arrangement).

It would repeal the $275 Million that has been provided to the States to help them detect and prevent private insurance price gouging as well as repeal the additional clarity of rules to help detect and discover accounting tricks designed to help hide their real profits and costs.

It would Repeal the Health Care Exchanges which would in 2014 allow individuals and small business the same purchasing power and economy of scale that large corporations currently enjoy when purchasing their insurance.

It would repeal the 85% Medical Loss Ratio Limit for Insurers in the Exchange, and repeal the leverage State Insurance Regulators currently have to block insurers who are currently gouging their beneficiaries with costs above the 85% MLR level by denying them access to the exchange and requiring that they pay REBATES to their customers for any premium charges above the 85% MLR. This impacts us NOW, because if there aren't going to be Exchanges in 2014, there isn't any leverage to push for lower premiums with insurers today.

Lastly it would repeal the plans most unknown, underreported and misunderstood provision. It would repeal the Office of Personnel Management's ability to contract a "Semi-Public Multi-State Option" where the Director of OPM would be able to offer Multi-State plans within the Exchanges in 2014 that meet the Medical Loss Ratio, Premiums and Profit Margin as set by the Director. These plans would have full and total price controls in place, and would only differ from the FULL public option only in the fact that those handling their day-to-day operations wouldn't have "U.S. Government" stamped on their paychecks. They would be government contractors.

(Full Disclosure: I've been a Government Contractor or worked for one for most of my adult life - so I don't have a problem with this idea at all, as it differs quite strongly from privatization since the Director, yet again, can completely Dictate the Profit and Premium Levels of these plans.

(4) ADMINISTRATION.—The Director shall implement this subsection in a manner similar to the manner in which the Director implements the contracting provisions with respect to carriers under the Federal employees health benefit program under chapter 89 of title 5, United States Code, including

(through negotiating with each multi-state plan)—

(A) a medical loss ratio;

(B) a profit margin;

(C) the premiums to be charged; and

(D) such other terms and conditions of coverage as are

in the interests of enrollees in such plans.

(5) AUTHORITY TO PROTECT CONSUMERS.—The Director may prohibit the offering of any multi-State health plan that does not meet the terms and conditions defined by the Director with respect to the elements described in subparagraphs (A)

through (D) of paragraph (4).

(b) ELIGIBILITY.—A health insurance issuer shall be eligible to enter into a contract under subsection (a)(1) if such issuer—

(1) agrees to offer a multi-State qualified health plan that meets the requirements of subsection (c) in each Exchange in each State;

I admit there is no guarantee that this will produce an insurance option as cost effective and efficient as Medicare, or even that that any contractor will be able to meet the Director's requirements if they are highly aggressive - all of that remains to be seen - but CBO did Score it as being no less cost effective than the Full Public Option would have been, so there is that relatively sunny prediction to consider.)

Under Ryan's Plan we see all these additional out-of-pocket costs, while losing all of these care options and guarantees. Hundreds of thousands of people who've lost or never had heath care before, but now do through their parents, small business or high-risk pools will lose their care, meanwhile the 30 Million Americans who would eventually get low-cost care through the Exchanges Will Never Get Coverage because Ryan doesn't even TRY to address that problem.

And to those who argue that we should just accept Ryan's plan because it's the only one "On the Table" - that is false. The People Budget also saves $Billions in Medicare Costs by allowing it save 40% on it's Drug Prices by negotiating for them the way the VA does, while adding the FULL Public Option (eliminating the third-party contractor) and even Single Payer to the table.

There's a lot we can do, the question is are we going to do something that saves a government buck at the cost to seniors pocket books and their health or are we going to continue implementing and enhancing a plan that will protect coverage and bring down costs for everyone?

Vyan