Most people are somewhat familiar with the concept of investing. You put some money in now, and you get paid back later what you put in plus a little extra. The little extra is interest. Sometimes the little extra ends up being a debt and you owe money, but that is how investing goes.

Social Security works the same way: there is pay-in through FICA taxes, a balance that earns interest, and a future payout. While everyone is focusing on improving ‘solvency’ by decreasing payouts (and eventually increasing pay-ins), curiously no one seems to be talking about interest rates.

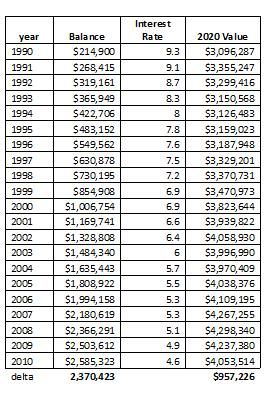

The social security trust fund is currently paying an effective interest rate of 4.4%. It has been higher but it has been trending down and it expected to go lower before it recovers. This low rate is forcing more and more money to be dumping into the trust via FICA taxes. It is also negating the effect of a rising balance. For example, using social security trust data, we can throw a stick in the sand and calculate the value of the trust in 2020 based on previous surplus levels and interest rates (values in Millions):

The way the above table works is this: If the $214B in the fund had been left alone and the 9.3% interest rate stuck, it would be worth $3.09T in 2020. This calculation is repeated for each row based on the new balance and new rate.

The 2020 value of the fund actually peaks in 2008 and is declining. Not only that, but despite having added $2.3 Trillion dollars to the surplus, the future value has increased by only $957 Billion. We might have been better off burying that money in the back yard.

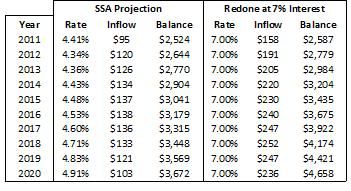

Of course, fixing the interest rate does wonders for the fund. Here is the Social Security Administration’s own projection through 2020, both as they see is and with a better interest rate (Values in Billions):

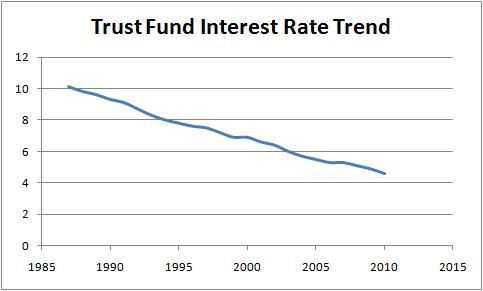

The result of an interest rate bump to 7% is an extra trillion dollars by 2020! Now social security trust fund interest rates are fixed by law to an average of interest rates on government bonds. In theory that is a simple follow-the-market command. Except, the “market rate” is rather curious. Here is a plot of interest rates:

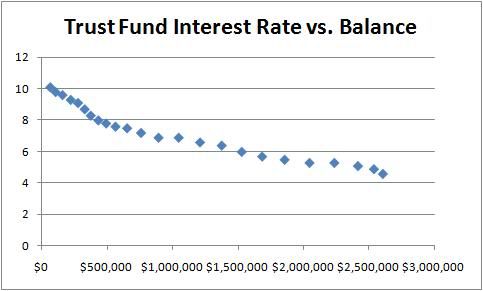

What is curious is that rates have dropped steadily through two economic cycles. Can you even spot the cycles in the graph? Now look at rate versus fund balance:

The more money you put in, the worse the rate. The thing to remember about a market is it takes two parties advocating for their own interests for it to function. When one of the biggest players (the SSA trust fund) does not advocate its own position, well it gets what others decide. The major others in this case are: other inter-governmental agencies, China, and Japan. All of these institutions have a vested interested in a low rate to either keep apparent debt minimized or to maintain currency advantage for trade purposes.

Side-note: when I mentioned it might be better to bury part of the surplus in a hole in the ground, what I’m getting at is that it appears the surplus itself is driving interest rate down. New issuances are actually under 3%. If this link isn’t broken, a fully funded social security trust fund would bankrupt everyone but the wealthy (who may never pay income taxes again).

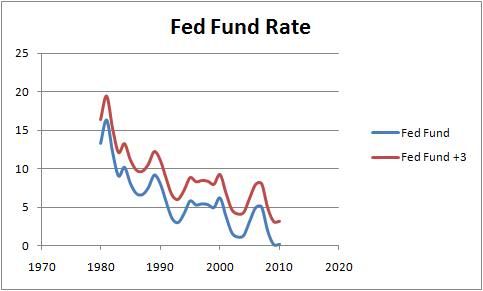

If you want to keep "politics" out of it, a slick alternative to the current setup is to specify interest rate as something like fed-fund+3. Not only does this follow more realistic lending rates, but it has the interesting effect of shooting a benefit to SSA whenever the fed decides to “cool” markets by raising rates. Here is the fed rate and a +3 rate:

Remember, the social security trust fund acts as a loan from low-income individuals to high-income individuals trough a trick of the tax code. We need to demand a fair rate. Markets only work when you know what you want, define it, and go demand it. If you simply demand ‘fix it’, you will probably get the monkey-paw solution of increased pay-ins and reduced benefits.

Update:

Here is a link to the spreadsheets

Last minor update/note:

Interest rate carries a negative connotation. Rephrase it as rate-of-return. The interest rate on the fund is YOUR rate-of-return on YOUR retirement investment. Demand better!!!!