(Author's Note: The full title of this peace is: "The Fiscal Summit Counter-Narrative: Part Four, The Deficit, the Debt, the Debt-To-GDP Ratio, the Grandchildren, and Government Economic Policy")

The neoliberal austerian ideology often emphasizes the consequences of excessive deficit levels, a high national debt, and a debt-to-GDP ratio. Among those supposed consequences are rapidly increasing and high interest rates in the bond markets, inability to “borrow” to pay for imports, inability to maintain spending levels on entitlements like Social Security, Medicare, and Unemployment Insurance, an increasing threat to government solvency, and a growing national debt burden that will have to someday be repaid by heavily taxed children and grandchildren.

These have been the main themes of the annual Peter G. Peterson Fiscal Summits, the latest of which was held on May 15, 2012. This series is presenting a counter-narrative to the austerian ideology being spread by Peterson and his associates, including David Walker, Robert Rubin, Bill Clinton, and President Obama, who mouth the myths of the austerians frequently and uncritically. The counter-narrative was developed at the Fiscal Sustainability Teach-In Counter-Conference held on April 28, 2010.

In developing the counter-narrative of the Teach-In, Warren Mosler, President of Valance Co. Inc., Financial Management Services, often credited with originating the synthesis of different perspectives that became Modern Monetary Theory (MMT), gave the presentation on the topic in the title of this post. My role at the FS Teach-In was to act as a non-interventionist MC and facilitator of the proceedings. So, I had the pleasure of hearing all the presentations including Warren's lunch time effort.

At the time, I thought his presentation was very successful and much fun due to Warren's conversational, and very open manner. But, perhaps, in part, due to my involvement in conference details, I didn't appreciate its brilliance fully until later when I read the transcript, and perhaps not even then, since I've found that writing this review involved a fresh realization of the depth of Warren''s understanding of the MMT paradigm, and the breadth of his knowledge about how financial systems work both in the United States and globally. In the vernacular, Warren did “a bang-up job.”

His presentation refutes a number of popular austerian myths including: the government is running out of money; the Government can only raise money by taxing or borrowing; We can't keep adding additional debt to “the national credit card”; We need to cut spending and entitlements; our main creditors, like China will cease to buy our debt making it impossible for us to raise money for deficit spending; our grandchildren must have the heavy burden of paying our national debt; Government deficit spending isn’t sustainable because the Government is like a household and that since households sacrifice to live within their means, Government ought to do that too; and “printing money,” i.e. deficit spending without selling debt instruments in corresponding amounts, is necessarily inflationary. Audios, videos, presentation slides, and transcripts for the presentation are available at selise's site and a slightly different version of the transcripts is available from Corrente as well.

Warren Mosler's Presentation On The Deficit, the Debt, the Debt-To-GDP Ratio, the Grandchildren, and Government Economic Policy

Warren begins by providing his own take on fiat currency systems. He asks: “How do you turn litter into money?” He goes on to ask if anyone will buy his business cards at $20 apiece. Seeing no takers he asks if anyone wants to stay after his talk, clean the carpet, and tidy up the room and offers to pay one per hour, and then notes there aren't a lot of takers. But then he adds:

“. . . Look, there’s only one way out of here and there’s a man at the door with a nine millimeter machine gun. Okay? And you can’t get out of here without five of my cards.

“Now things have changed. I’ve now turned litter into money. Now, you will buy these, you will work for these things if you want to get out. The man at the door is the tax man and that’s the function of taxes. Stephanie talked about how taxes do it. But you can recreate that…”

Warren next talks about a currency called

the buckaroo introduced at the University of Missouri at Kansas City (UMKC) “ten or fifteen years ago” to replicate a currency to help students understand National Income accounting, currencies, and the idea that currencies can work the same way in small open economies as in large open economies like the US. You earn buckaroos by doing public service or community service. The rate of pay is one buckaroo per hour. The buckaroos are freely exchangeable. There's a buckaroo tax of 20 per year. And you can get them by working for them or buying them from other students. The schools ran a deficit, and at the end of the first year 1100 buckaroos were earned and 100 buckaroos were paid in taxes. The deficit didn't affect the school's credit rating.

The deficit is equal to the savings in buckaroos by the students, the first lesson they learned. “The government’s deficit equals non-government savings of financial assets. To the penny. . . . Was it a problem that more community service was being done than was needed to pay the tax? Of course not.”

Also, Warren points out that the value of the buckaroo has been fixed to the value of one hour of student labor for fifteen years, but in the market where students buy and sell them they started out at $5.00 apiece, and now sell for $15.00 apiece. The price of the buckaroo in dollars and Euros has increased, and the buckaroo has greatly outperformed the S & P 500 over 15 years. So, the buckaroo appreciated because it works for its original function which is “. . . . provisioning the community with student labor — to move labor from the private sector to the public sector. And of course to teach National Income accounting and how a currency works to the students.”

So, Warren moves on to the question: “What is money?” He points out that we're not the gold standard, but we still think we are, and says that: “There is no such thing as a government saving in it’s own currency.” He again points to the value of the buckaroo rising from $5 to $15 apiece, also says that UMKC has an infinite amount of buckaroos and asks: “Does that mean the School is infinitely wealthy? No. Was the School collecting them from these students to get the buckaroos to be able to pay them? No.”

Warren also points out that UMKC had a Zero Interest Rate Policy (ZIRP) on the buckaroos it issued including the excess 100 issued in his example. “Did that cause hyper-inflation? No, the currency gained in value. It appreciated. It didn’t go down in value. And do we see that happening in the real world? Sure. We’ve had Japan with a zero interest rate policy for twenty years. It’s been one of the strongest currencies in the world. With the lowest interest rates.”

Warren asks next whether UMKC should try to run a surplus in buckaroos if it anticipates paying them out in the future, and then makes another key point of MMT: “There is no such thing as accumulating a reserve in your own currency when it’s a floating exchange rate like that.” And he then asks whether UMKC can even run a surplus, and points out that on day one of the program they could not, because they have to spend first, in order to collect taxes in buckaroos. He points out further, that the Fed has to buy securities the same day its selling them to provide the money people use to buy them at auctions.

Warren then takes up the issue of printing -- “the P word.”

”There are three ways to spend with a gold standard: tax financed, debt financed and money financed which was called “printing money.” Tax financed was easy. You taxed and then you’d spend. Debt financed you’d sell bonds and then you’d spend. And the last way was “printing money” and that’s where the term “printing money” comes from. It has no application to whatsoever with today’s currency arrangements but it’s still used and it still has the same connotations.

“The reason they used to debt finance was because if the government spent by printing money and didn’t sell bonds to get that money back — that was a convertible currency, you could get gold from the treasury, you could cash it in. So they were always at the risk of running out of reserves and going broke and that type of thing. So any government deficit spending had to be…. and that’s why the rules that Randy was talking about that are left over from the gold standard include the requirement that Treasury borrow money before it spends. Inapplicable with today’s currency arrangements.”

Warren then gives evidence that we're still on gold standard thinking.

”Why did the Democrats cut Medicare? Why did the Democrats raise taxes? Why did the Democrats visit China? . . . .

“Why did the Democrats form the bipartisan committee to report back on ways to reduce the deficit? Why did the Democrats put Social Security and Medicare on the table? Why are we here? Right?

“Gold standard thinking. They think the government has run out of money. It’s not because they are worried about inflation, although they are or they might be. They think the government is spending now limited by how much it can borrow from the likes of China, leaving that debt to our children to pay back. We’ve all heard this many many times. We’ve seen President Obama, Secretary of State Clinton, Treasury Secretary Geithner go over to China to negotiate with our bankers to make sure everything is okay because they believe we are dependent on them to fund everything from Afghanistan to health care.”

Warren then emphasizes that the point of the currency is to provision the public sector of a nation. He says there are a lot of ways to do that: a command economy with slaves; a lump on your head and you're in the British navy. Now the more civilized way to do it is to impose a tax, “. . . . with a man at the door with a 9 mm to enforce it, and then show you what you have to do to earn the money to pay the tax. And that’s how we provision our public sector.”

Warren continues with the point that “taxes create unemployment,” because when taxes are imposed money must be earned to pay those taxes, and there's no guarantee there would be enough money available to pay for full employment. “We take people out of the private sector, we get their time out of the private sector with taxes. Government spending then employs those we just unemployed. . . . The whole point of getting the students unemployed with the buckaroos was to get student labor to help out in the hospital.”

And he continues:

”If we’re going to tax, and then not hire all of them and leave 20 million people looking for paid work who can’t find it, and because of our monetary system can’t support themselves, and we’re destroying our entire social fabric, why are we doing this? We should lower the taxes. . . .

“Unemployment is the evidence that the budget deficit is too small, that the government has not spent enough to cover the demand to pay its own tax, plus any residual savings demand that comes from that tax liability. Unemployment can always be eliminated with a fiscal adjustment. You either cut the tax and the people go away, or go ahead and hire them to do what you wanted them to do, which is the reason you started the tax to begin with.”

Warren had much more to say:

On monetary operations: “The federal government neither has nor doesn’t have dollars. Government spending: . . . they just mark up the numbers in our bank account. It doesn’t come from anywhere; it doesn’t use anything up. Government taxing: they simply mark down numbers in our bank accounts. They don’t get anything; they don’t pile anything up.”

On Deficit spending: “. . . the guy in Treasury has changed more numbers up than the guy at the IRS has changed numbers down. That's called the deficit, We can call it whatever we want. The national debt is that difference from the beginning of time, 13 trillion dollars.”

LetsGetItDone Comment: Not from the beginning of time, I don't think. What Warren defines here is the gap between tax revenue and spending and he equates that to the debt. But there have been times in our history, namely during the Civil War, World War II, and if I recall correctly, for a brief time during the Kennedy Administration, when the Treasury created and spent money without issuing debt. Even today, Treasury revenues come partly, though in small amounts, from coin seigniorage profits. In addition, the national debt, some of which was probably denominated in foreign currency was paid off completely during the Administration of Andrew Jackson. So, any current debt subject to the limit, denominated in US dollars, can only date from 1835.

The more important point here, however, is that the negative gap between tax revenues and spending need not equal the national debt subject to the limit. It only does so when that gap is closed with credits resulting from the sale of debt instruments redeemable in a specified period. If spendable revenue is generated from other sources, then the cumulative deficit, defined as the gap between spending and tax revenues isn't equal to the national debt subject to the limit. In fact, if sufficient money is created without issuing debt instruments specifying a period for repayment of principal, "the national debt" could be completely retired, while the cumulative deficit could continue to increase as needed to fuel private sector savings. This possibility is illustrated by the buckaroo example where deficits can occur every year, but no debt instruments are ever issued.

Warren then continues by raising the issue of inflation. He offers a slide saying WARNING! OVERSPENDING CAN CAUSE INFLATION!!! and explains that he doesn't want anyone saying he forgot about inflation, even though he knows they're going to say it anyway. And then he says that when the Government spends they put money in a checking account at the Federal Reserve Bank called a reserve account so that people can sound professional when they that “. . . our reserve balances went up . . . .“ The national debt is in another kind of account at the Fed called Treasury Securities. That's a savings account because “You give them money; you get it back with interest. . . . Cash is the exact same information as your checking account but it’s written on a piece of paper, so instead of getting your balance on a computer screen or bank statement, you get to carry it around with you. . . it’s a thing you can use to make payments to the government for taxes.”

”Once the government has spent, that money appears in one of those three forms. So if the government spends without taxing, just spends, that’s called deficit spending, say on day one the government just spends a hundred dollars, it’s going to be one of three places. It’s going to be cash in circulation, or in a checking account, or in your savings account, somebody’s savings account. There’s no other choice: the dollar has no other existence, other than those three places.

“And all of this equals the world’s net savings of dollar financial assets. There are thirteen trillion dollars or so in the savings accounts and checking accounts and cash equal to the penny to the cumulative deficit spending. That’s how much the government has spent and stuck into those accounts, but hasn’t yet taxed and taken out of those accounts. Spending puts the money into the accounts; taxing takes it out. If you put it in and don’t take it out, it’s a deficit; it’s our savings; it’s held by you, me, China, whoever owns Treasury securities.

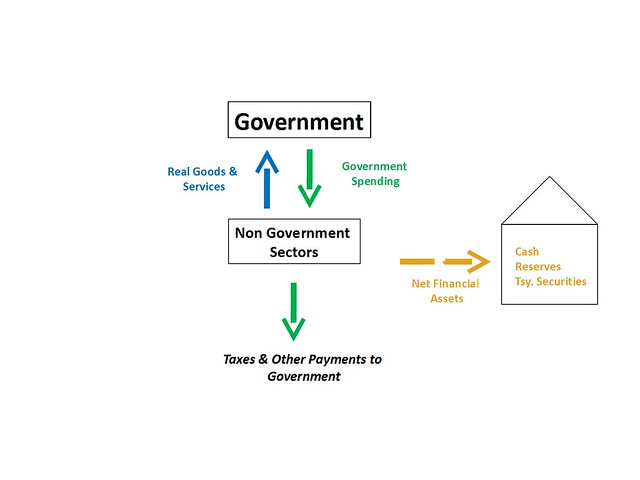

“A little diagram to explain it here: to see how it works, just to make it graphic, that I did a long time ago. It appears in Randy’s book Understanding Modern Money. Up at the top, you have (I’ll do it from here so I have the microphone I guess). In the middle you have the non-government sectors; that’s all of us, everybody except the government. Now let’s start at the bottom: the government imposes a tax. We have to pay this tax or we can’t get out of the room; we’re going to lose our house and our car. When I say tax, just think of a property tax, because that’s easy. If you start thinking of an income tax, what if you work, what if you don’t work, it works, but you’ll lose track of the rest of what I’m saying. Trust me, it does work, but think of it as a head tax or a property tax, just to keep it simple.

“So the government levies a tax, and now we need the money to pay the tax. Notice I have taxes going out — down into the drain. I don’t circulate them back. There is no such thing. We ship real goods and services to the government — the government’s doing this because it wants to provision itself — and the government gives us the money we need to pay the tax. Goods and services to the government, money to pay the tax, some gets paid in taxes, some gets saved. Where does it go? It goes to the tin shed in Canberra — the warehouse over on the right. In Australia, it’s this tin shed; over here we’ve got a big concrete building. And that’s how it’s held: it’s held in one of those three forms: cash, reserves, or Treasury securities. All that Fed operations do is shuffle around the difference between cash reserves and Treasury securities. When the Fed buys securities from the private sector their securities go down and their cash reserves go up. When the public wants more cash the reserves [sic] go down and the cash goes up. The total is always the same; it’s always equal to the deficit.

“The only place that net financial assets can come from is government deficit spending. This is all accounting; no theory, no philosophy; ask anybody at the CBO, and they’ll say, yeah, that has to add up to the penny, or we have to stay late and find our arithmetic mistake.

“So last year the government spent a trillion and a half dollars more than it taxed, that money went into the warehouse, it’s now held as Treasury securities, reserves, or cash, otherwise known as savings, and sure enough last year savings went up by exactly that amount, to the penny, when you include all the non-government sectors.

“Deficit spending adds to our savings. I think I just said that.”

LetsGetItDone Comment: Sorry for the long quote. But my appreciation for this passage is boundless. It is so clear and down to earth. And it has both the virtue of simplicity and the ring of truth. If you study it and comprehend it, you will have gone a long way toward understanding MMT.

Warren continues his presentation with a simple illustration. I'll skip it here, but you can go to the transcript for it. The bottom line is: “Government deficits add to savings, to the penny. The deficit clock could be renamed the savings clock. This has already been covered — the same thing.” This last is a reference to Stephanie's presentation and her world savings clock.

Warren then goes on to review the fiscal sustainability implications of what he says echoing both Bill Mitchell's and Stephanie Kelton's views covered in Part Two and Part Three.

“Fiscal sustainability review: Spending is not constrained by revenues. Spending is changing numbers up; putting numbers into our checking accounts. Taxing is changing numbers down, taking numbers out of our checking accounts. Borrowing is moving numbers from our checking account to our savings account. There is no numerical limit to any of this. Paying interest is changing the number up in our savings account. The government can always make any payment of dollars it wants to make. This is all we’re talking about; it’s a nominal system; we’re talking about there are no nominal constraints.

“The risk is inflation, and not insolvency or not-solvency; there’s no solvency risk.“

And then he briefly reviews the self-imposed political constraints discussed in the first two presentations.

LetsGetItDone Comment: So, Warren's telling us that there is no problem of nominal fiscal sustainability at all. The level of debt, and the level of the debt-to-GDP ratio don't count at all. And deficits also don't count from a solvency point of view. Where they count is with respect to inflation. As he says: “WARNING! OVERSPENDING CAN CAUSE INFLATION!!!”

This highlights the more general MMT point about Government spending, including deficit spending. What counts is the impact of such spending on a variety of things including employment, inflation, poverty, crime, social integration, energy foundations, education, and so on. We have to evaluate Government spending by its impact on the real world, not by its impact on purely nominal indicators like the debt subject to the limit and the debt-to-GDP ratio that have no economic importance for a nation sovereign in its currency.

Having said that however, it's important to emphasize that people have a visceral reaction to the “national debt” notion and the idea of “borrowing” because of the false analogy between everyone's household budget and the Government's budget, so even though the debt and the debt-to-GDP ratio aren't economically important from the MMT point of view they are politically very important because of the way people react to them. It will take years for people to accept that the national debt doesn't mean anything economically if persuasion alone is involved. But if we can demonstrate that the national debt isn't important by paying it off using the unlimited currency creation power of the Federal Government, then that will do more than anything else to persuade people that the Government's budgetary and spending capabilities are very different from their own because the Government is the currency issuer and not just a user of its own currency.

As it happens, and paradoxically, this demonstration can be performed at any time by the President, if he has the courage to do it. All he has to do is use current law to order the US Mint to produce a $60 Trillion dollar coin and deposit it at the Fed. I've written about this many times; for example, here and here. The eventual result of his action would be to fill the Treasury General Account with $60 T in electronic credits. This amount can then be used to eliminate the national debt as a political issue and can probably cover all deficit spending for the next 15 – 20 years.

These points also have implications for REAL fiscal sustainability. One of the real effects of misconceived fiscal policy such as austerity, is that if it is applied over a number of years it can degrade the capacity of the economy to produce real goods and services domestically. If that happens then the output gap, the space between what we can produce and what we are failing to produce due to unemployment and inadequate demand, can close over time by destroying our capacity to produce. If that happens, then the capacity of the Government to add nominal wealth to the private sector without causing inflation declines.

So, austerity in Government spending can create REAL fiscal unsustainability, in the sense that lack of Government spending when it's needed to create full employment can shrink the amount of Government deficit spending that can later be applied without experiencing serious demand-pull inflation. REAL fiscal sustainability is government spending whose effects maintain or increase the ability of the government to spend without causing inflation or other side effects that compromise our economic future. Unfortunately this is not what the President and the other members of “the Peterson Party”, whether Republican or Democrat mean when they talk about fiscal sustainability. Their theory of fiscal sustainability is about the wrong problem. It is about the problem of running out of money. For the US, that can happen. But what can happen is that Government austerity can produce idle and decaying productive capacity, so that the ability of the Government to spend to help create full employment without causing high inflation is severely damaged.

Getting back to Warren's presentation, he says:

”So now we can get to the main thing, to why we’re here: is Social Security broken? Well, we have to define what broken is: first, what’s the public purpose? What’s the presumed problem; what is the real problem?

“Public purpose of Social Security: Well why do we do this? To provision seniors at a level that makes us proud to be Americans.

And he goes on to talk about the real issues and choices involved in allocating nominal wealth to seniors, pointing out that we have no shortage of food, no high standard of living provided by SS, no housing problems, but many vacant homes, and he points out that we want to provision our seniors at a level that makes us proud to be Americans, but not at a level so high that it's embarrassing. He also points out that seniors aren't happy when they to tap their children for money, and their children aren't happy either. Also, SS gives seniors a feeling of independence, even though they're getting money from us collectively, and that means some consumption is being shifted to them. And he says that he likes collective provisioning for seniors rather than individual provisioning, and points out that this is a political choice. But he asks:

”So what is the presumed problem? Are they living too well, which is what I was just talking about? Are the opportunity costs too high, that is, are they using resources we need? And the answer to those are no.”

“Is the trust fund a limiting factor? Absolutely not.”

Why not? Because the Trust Fund is just a record resulting from the man at the IRS debiting a private sector checking account and crediting the “Trust Fund.”

”But it’s not “the money”. The government never has or doesn’t have “the money”; there isn’t any such thing; those are not dollars. “Accounting” means a count; it’s record-keeping, it’s a record, it’s not a constraining factor. If it goes negative, it goes negative; a light doesn’t go on and — you know — something breaks open and Bill gets drowned in the flood.”

The real problem, if there is one, is the dependency ratio. That’s the ratio of workers to retirees. “If, in thirty years, we’ve got three hundred million people retired and one guy left working, that guy’ going to be really busy. [laughter] “. . . And so, what do they say, and the mainstream economists agree, they say, therefore, we’ve got to make sure everybody’s going to have enough money to pay this guy, but, uh uh, that’s not going to matter.” The only real thing that will be useful in 50 years is our knowledge and our education. Hardly anything we produce now physically will be “of any value fifty or a hundred years from now. The one thing that we have, that people left us from fifty or a hundred years ago, is our technology, our know-how, our software, and that type of thing. It’s not the hardware.”

However, because we think it’s a money problem, we think the problem is these guys are all going to need a lot of money, because look at how high the prices for laundry services are going to be when there’s only one guy doing it for three hundred million people, we need to cut back and sacrifice today and run surpluses and tax more than we spend, put twenty percent of our people out of work, and, ironically, the very first thing we cut is the only thing that they would agree they’re going to need, which is education.

“More on Social Security: The trust fund is record-keeping. Social Security contributions are regressive taxes that function to reduce take-home pay and aggregate demand. Why is a Democratic administration supporting a tax that taxes those people at the lowest income levels the most? It’s not even a fair tax, it’s completely regressive. Why are they doing that? They’re not trying to do that, it’s not their agenda. They believe we’ve run out of money.

“Social Security payments are progressive distributions that add to take-home pay and aggregate demand. Why are they cutting these? Why did they just cut 500 billion out of Medicare? Not because they think we shouldn’t have it, or because they think there’s something wrong with a progressive distribution to help aggregate demand. Because they think we’ve run out of money.

“Why are they contributing to the unemployment problem? Who is unemployed? We just grew at 5% for a quarter, at six percent, maybe another five percent this quarter. That’s very high real growth. Well, who’s getting all that real wealth? It’s sure not the people who’ve been losing their jobs or seeing real wages fall. It’s not the lower income group. Well then, who is it? It’s somebody else.

"We’ve seen a Democratic, populist administration preside over the largest upward transfer of real wealth from low-income to high-income people in the history of the world. That is not what they were elected to do, and not what they intended to do. It’s because they don’t understand the monetary system and monetary operations. It’s not even theory. They don’t understand actual operations.”

Warren then moves to inflation, and says that right now (end of April 2010) the risk is deflation in the CPI and in the housing market, and points out that “. . . hyperinflation because somebody spent an extra dollar. . . “ isn't how it works. And then he drops a bunch of facts.

”If you look at the worst financial collapses in the last twenty years, let’s look at Mexico in approximately 1995, I forget the dates. The peso was three-to-one, something like that, three and a half to one, absolute collapse, the currency up in smoke, no faith in government, no faith in everything, and it went to nine. They had about a sixty percent drop. It didn’t drop to zero, the peso didn’t go to a million-to-one. Russia totally collapsed. The ruble machine was shut down. Everybody turned out the lights, pulled out the plug, and left the central bank for six months. The ruble went from 645 to 28, a seventy-five percent drop. It didn’t hyper-inflate, or do anything like Zimbabwe, or Germany, which Marshall explained, which were entirely different situations. So even in situations far more extreme than anything we can imagine, which were fixed-exchange-rate regimes blowing up, which we don’t have, you don’t get sudden jumps in inflation; there just is no such thing.

“What happens if Social Security checks get too high? What happens if we are over paying? How would we know? Well, unemployment would get too low from all the spending, whatever that means. The economy would grow too fast, whatever that means. Seniors would be living too high. Prices would start going up, we’d start seeing the inflation. And then what happens?”

Then it might make sense to raise taxes or cut benefits, but not right now. He says we only do that when it doesn't make sense to spend any more. It's a political choice and doesn't have anything to do with running out of money. Why are SS cutbacks on the table?

”Our leaders don’t understand the monetary system. They don’t know spending is not constrained by revenues. The think that to spend what we don’t tax we have to borrow from the likes of China, for our grandchildren to pay back. It’s all a tragic mistake of epic proportions.”

And that's his transition to discussing the issue of “borrowing” from China, and the grandchildren. He asks how China gets their dollars, and then explains that they sell goods in our department stores and the money they get paid goes into their checking (reserve) account at the Fed. At this point we owe them “. . . . a bank statement that shows how much they have in their checking account. Then Treasury auctions off Treasury securities which China buys.. And the Fed do? They move the money from China’s checking account to China’s savings (securities) account at the Fed. So, now we owe China all that money with all that interest.

“How can we pay back the whole 13 Trillion in savings accounts? Just like we do every week when tens of Billions come due: we transfer that balance plus interest back to the checking accounts at the Fed. Paid debt paid back. They have three choices with what they can do with that checking account: leave it alone, put it back in the savings account or spend it.”

LetsGetItDone Comment: Not many know just how much debt we pay back every year.

Ben Strubel shows that $437 Trillion was paid back between 2001 and 2011.

Warren goes on. If they spend it they'll buy something. If they buy other currencies then we transfer their dollars to the reserve account of someone else, and their central bank transfers the currency bought by China into China's account at that central bank.

”So, what is the problem? What are we leaving to our children and grandchildren? They’re just going to need one accountant like we do to debit and credit these accounts. The whole thing could be done on one spreadsheet. You could run that whole part of the Fed with about $100,000 out of your budget if you wanted to. There’s nothing to it.

“People say, “Well, what happens if China dumps all their dollars and the dollar goes down? Whatever are we going to do?” At the same time, the same people are saying that we need China to revalue their currency. Their currency is under valued by 50%. On the one hand they want us to revalue their currency up, which means have the dollar go down by 50% and on the other hand they are panicked over what will happen if the dollar goes down by 50%. Guys, you can’t have it both ways. Figure out what you want.”

LetsGetItDone Comment: Warren put his finger right on it. Our policies towards China are often schizophrenic. We can't decide whether we want them to devalue their currency relative to ours and cut those cheap exports, allowing some private sector jobs to come back; or whether we want them to help us maintain “a strong dollar,” to help us fight our wars, import all those cheap goods, keep gas prices down here, and enrich our elites who are benefiting from international trade and finance. So we talk out of both sides of our mouths all the time. We're as silly as the French and German elites who want to impoverish Greece, but also want to keep exporting goods to the Greeks.

I know what I want. I want us to take that cheap real wealth from abroad, but only on the condition that we implement a job guarantee at a living wage with full fringe benefits here, and only on the further condition, that we don't allow free trade in industries important for future innovation and national security.

Right now we're practicing “trade unsustainability.” Not because, it's financially unsustainable. It is fully sustainable as long as people in foreign nations want to send us real wealth in return for electronically marking up their accounts at the Fed. However our patterns of trade are politically, socially, economically, and culturally unsustainable in that they are causing decay in our politics, our local communities, our economic futures, our levels of social and economic justice, our levels and quality of education, and even our national security, since we have been hollowing out our heavy manufacturing base.

So, in short, while it's true that in the aggregate, over a specific relatively short period of time, imports are real benefits and exports are real costs, there is an issue of societal sustainability here in the broadest sense of the term. And the side effects of the kind of trade policies we've been following aren't accounted for by the truth that when real wealth is given up in exchange for nominal financial assets in one's own fiat currency; it's the real wealth that counts, at least in the short run.

Warren next moves on to “What’s wrong with the euro zone?” He starts by pointing out that Greece is not like the US, UK or Japan, because it is a currency user like all the other euro nations, “. . . revenue dependent like US States, businesses and households.” Warren points out the US has recovered better than Europe, because it had not only a central bank, but also a Congress/Treasury to run deficits which went to the States and the people in them. Without these federal deficits, the deficits of state governments would have been much higher. He points out that the States could not have sustained the kind of deficit spending done by the federal Government.

But the Eurozone States have had to do that. “They’ve been in true ponzi. Ponzi is when you have to pay somebody back from getting the funds from the next person.”

”The US government, Japan — Japan with 200% debt to GDP is not in ponzi — they don’t pay people by getting the money from somebody else. They just change the numbers up like we do. That is not ponzi. Ponzi is when you have to get it from somebody else.

“Europe has put themselves in ponzi from day one. And we’ve been pointing it out from day one. Now, ponzi works on the way up. Madoff went a long time before he collapsed. So did Stanford. It’s on the way down where it all comes apart.

“We’re seeing the back end of this coming apart. . . . “

Warren continues with an account of some the details of the faulty Eurozone structural defects and then ends with:

The shoes will have to fall. They don’t have credible bank deposit insurance. If Greece goes down and people realize they are going to lose their 50,000 euros in their bank account, the rest of Europe can be in a big problem. They are already having runs on the banks and it gets a lot worse. It shuts the whole payment system down.

There is no credit worthy government entity to act counter cyclically…

LetsGetItDone Comment: It's two years later, now, and Europe's even worse off that it was then. The ECB and other Eurozone authorities have tried to bail out creditors in various nations while imposing austerity on the other citizens of various nations. Now, all the PIIGS nations are facing increasing difficulties and some are close to collapse. The ECB still seeks band-aids, and there are no proposals on the table yet, that can stabilize market lending to the Eurozone members. Warren recently produced

his own proposal for ending the crisis, but it's too early to say whether it will break through elite filters in Europe.

Warren Mosler's wide-ranging presentation was followed by a Q and A session. I'll go through that and add comments. But before I do, I'll provide some follow-up references on the subjects treated in Warren's presentation appearing since the Fiscal Sustainability Teach-In. The most important from Warren include the revised version of The 7 Deadly Innocent Frauds of Economic Policy. Warren blogs nearly every day, providing news articles on significant world financial events and policies, and his commentary on them. He emphasizes Eurozone events very heavily, and his evaluations and qualified predictions are always pretty much on target. Here, here, here, here, here, here, here, and here. are updates on the subject matter from Warren.

And: here, here, here, here, here, here, here, here, here, here, here, and here, are contributions from Bill Mitchell, Stephanie Kelton, Scott Fullwiler, Pavlina Tcherneva, and Randy Wray.

And finally, several of my own: here, here, here, here, here, and here.

SESSION 2: “The Deficit, the Debt, the Debt-To-GDP Ratio, the Grandchildren, and Government Economic Policy” - Q&A

Maurice Sanders: “Just a quick question for you, Warren. When you describe the moral hazard in the Eurozone, would your description then be different if there were a political superstructure to encompass all those nations in one political structure?”

Warren Mosler: “Yeah, if the deficit spending was done at the new fiscal authority, call it the European Parliament, then you don’t have the race to the bottom. It’s when you split things up, it makes them compete with each other. For example, if you have federal pollution control laws you don’t have a race to the bottom, but if you have state pollution control laws then the state that allows the most pollution gets the most business. So yeah, that consolidation would take care of it.”

Joe Bongiovanni, Kettle Pond Institute: “When you floated your proposal on your blog about the European central bank paying out a trillion dollars, I asked you the question, “Is anybody going to issue any debt to do that?” And eventually you answered me back and said, “No, there would be no debt issued.” Am I right about that?”

Warren Mosler: It’s just a payment. It’s not a loan, it’s a payment.”

Joe Bongiovanni: “So, does that hold true for deficit spending by us, then? That is to say, our central bank, when we’re going to deficit spend, can they also just make the payment without issuing any debt?”

Warren Mosler: “What I’m saying is, if the federal government pays you money, it can either pay you money or loan it to you. If it pays it to you, you have no debt. If it lends it to you, you have a debt. So when the European central bank pays… makes a per capita distribution of a trillion euro [to] the member nations, it’s not added to their debt, they don’t owe it back to the European central bank. When the Federal Reserve makes a payment, it goes into someone’s checking account. We can call that a debt, if we– it’s how you define which account that money is in. We don’t count that as…”

Stephanie Kelton: “It’s like helping our state governments.”

Warren Mosler:

“Right, right. But if the Federal Reserve makes a payment to anybody, whether it’s a payment to the state of Connecticut or a payment that goes out and buys a box of pencils, it goes into somebody’s checking account. It goes into a reserve account at the Fed, through your member bank. We don’t call that “debt.” It’s only when we move the money from the checking account to the savings account that we call it “debt.” So, what’s called “debt” at the Federal level I would not call it “debt.” I never would have called it “debt” from the beginning. It used to be called “debt” because we owed the gold that were in reserves. Once the gold was gone, it’s no longer debt, it’s payment in kind. It’s just a store of nominal wealth for the other guy. It’s not a debt. The European central bank hasn’t started on a gold standard, so they don’t automatically call something debt that isn’t debt, so they don’t have the problem of creating debt when they spend. It’s a little bit of a technical answer, but the answer is that a payment from the European central bank is not booked as debt anywhere, because they never have booked it as debt. We book it as debt because we have a gold standard tradition that caused us to book it as debt. It’s both– they’re all the same thing.”

LetsGetItDone Comment: I find this an enormously interesting comment. Its implication is that if the European Central Bank does begin to “deficit spend” on direct payments to the member States, then it will not incur any debt in doing so, as other sovereign fiat currency nations do because of their silly hold-over views from gold standard days. So, in that case, the national Governments in the Eurozone will raise taxes and borrow money to fund their spending. And they will also get direct payments from the ECB. The member nations will have “national debts” and debt-to-GDP ratios; but the Eurozone itself will maintain a debt-to-GDP of zero due to its “printing money.” Wanna bet that won't be a source of inflation in the Euro?

Unidentified: “Question for Warren Mosler: since I’m a foul-mouthed leftist blogger, I’m going to frame this as polemically as I can. Speaking to the question of the Tragic Mistake theory, is there a reason to choose the theory of the Tragic Mistake, as opposed to a theory that this is a deliberate act of policy that’s meant to cause as many people as possible to suffer and die? How would I choose one theory as opposed to the other?”

Warren Mosler: I forget the saying, but it’s better to presume innocence than to– how does that go? You know, my book up there that I’ve got, called “The Seven Deadly Innocent Frauds,” it’s John Kenneth Galbraith’s last book. “The Economics of Innocent Fraud,” and he said it more eloquently than I did, but it’s the idea that when you presume innocence, you’re making a much stronger statement than imputed guilt.

Unidentified: "You would have evidence to back this up?"

Warren Mosler: "Which?"

Unidentified: "Why should we p

resume innocence, based on the record of the last thirty years or so?"

Warren Mosler: "Only as a point of logic, that you’re better off presuming innocence. As part of the argument."

Unidentified: "As a rhetorical tactic?"

Warren Mosler: "To say the person is… I’m not sure how to… Yeah, sure, as a rhetorical tactic, you presume innocence."

Unidentified: "As a foul-mouthed leftist blogger I can completely accept that."

Warren Mosler: “Presuming innocence is more powerful, is a far superior rhetorical technique. Especially if it’s something that’s really simple to understand, because then you’re really throwing the onus on the other guy: “You’re either a complete idiot, or you’re subversive, which is it?””

Bill Mitchell:

“Someone asked me at lunchtime whether the European leaders knew about options to solve their current issue, and I said to them that if you read the documents, and the debates going back to the Delors papers, and then subsequently, you will be left with the unambiguous impression that they know all the options. Most recently, the German Finance Minister was interviewed and it was in German, I couldn’t find it in English. I was going to try to put it in the English version, but it was in German, but fine.

“And what he said in the interview was that when they framed the common currency system, they had a choice. And they had a choice to add elements that would have made the current crisis much less a crisis. And those elements were a system to deal with asymmetric shocks, in other words, a fiscal redistribution system; and also, as Warren said, a single fiscal authority. And he said that that was debated, and if you go back to the original debates you see the debate there. And they chose, as an explicit choice, to exclude those characteristics from the system, the very characteristics that would have made the current crisis significantly less severe. They chose explicitly to exclude them from the system.

“And as soon as the common currency came in, Germany then introduced their so-called Hartz reforms. And these were reforms that — because previous to that, they were able to maintain their export competitiveness through exchange rate movements. Once they lost that capacity because of the common currency, they had to work out another way to stay one up on the other countries, and so they brought in the significant deflationary measures in their labor market: casualized significant sections of their labor market, reduced workers’ real wages and conditions, the whole Hartz agenda. And these were all very explicit choices and decisions they made within the context of the institutional system they were setting up. They knew the alternatives. And they knew that once the crisis hit, then the weaker countries — in a trade sense — would melt down, as they are. So, I’m not so sure I agree with Warren in emphasis. I think that they…”

Warren Mosler: “It’s rhetoric, though, just rhetoric.”

Bill Mitchell: “I understand the rhetoric. I think that I prefer to say that they aren’t innocent. They took an ideological decision. They were scared to death. There’s a cultural animosity within Europe stemming back to the Latin and the Germanic cultures. The second World War’s had an incredible influence on the way they’ve structured the evolution of the European community, and now the EMU, and the ideology surrounding all of that led them … The Germans dominate, they don’t trust the Italians and the Spanish, and particularly the Greeks. And they set up a system that would punish those countries in the event of a crisis, and they deliberately did it, and they know the options. They know all of the options that could reduce the pain, but they don’t want to do it.”

Warren Mosler: “There have been statements out of Greece that they owe us these loans for war reparations. . . . “

LetsGetItDone Comment:Based on what Bill said; perhaps Greece and some of the other PIIGS should sue the Euro zone in the International Court of justice for allowing them to join it while knowing full well that the system would punish them in the event of a crisis?

Bob Hahl, Kilowatt Cards:

“You said that, and it’s pretty clear, that raising taxes reduces demand for goods and services, but it also seems to reduce other kinds of things like greed, or power, unbalanced power — very rich people have enormous influence. I think back to the situation after World War II when the upper tax rate was 90%, and people always talk about that as if there were a lot of people paying 90% marginal rates, and I don’t think very many, if anyone, ever did. I don’t think anyone made that much money. What happened was, faced with a choice, if you’re an employer, of taking money out of your company and giving 90% of it to the government, or distributing some of it to the workers instead, and getting something for it, that was a better choice. And so I can understand the idea of lowering taxes, but at the same time you’re also unbalancing society, and you’re letting people accumulate so much money and we don’t know what kind of crazy thing they’re going to do with it.

“How do you control that? We don’t let people keep bazookas and land mines to protect themselves, but we’re letting people get rich enough to compete with countries.”

Warren Mosler: “Second amendment. No, those are all very legitimate political decisions. Those are political decisions. Those are the consequences of policy, but it doesn’t mean the government’s going to run out of money.”

Unidentified: “How does that jive with the notion that tax rates should be used to regulate aggregate demand?”

Warren Mosler: “We didn’t say tax rates– . . . “

Unidentified: “Ok, taxes. The tax code has been used to redistribute income, and in my opinion, right now it has been hijacked to favor upper-income households. Now we have huge income inequality in this country, so again, how does that jive with this notion of regulating aggregate demand?”

Warren Mosler: “There’s a bigger problem with that, because what also tends to happen is people wind up with the same after-tax money, so when you raise tax rates, and let’s say wages stay the same, tax rates go up, and government stays the same size, that means the higher incomes go high enough to adjust for the taxes. So after the Clinton years, you see, “Oh gee, look, we collected an extra trillion in taxes because of the higher rates.” Yeah, but those people earned an extra $5 trillion in income. So, it’s a moving target as well. There’s a lot of intuition, I guess we called it, and illusion as to what’s going on, when you dig down into it. Everything government does has distributive consequences, and those should be the first and foremost political decisions, not whether we’ve run out of money or not, or whether we’re going to borrow from China.

“What these myths have done is taken our eye off the ball of what I would consider are the important decisions. I did a paper with Randy and James Galbraith, we gave it to the GAO and FASB on sustainability, and we said, “Look, the problem is 100% of your time, money and effort is going into figuring out government solvency, and none of it’s going into the inflation problem. So what you’ve got is 100% of your resources going into the thing that doesn’t exist, and nothing going into the thing that could actually be a problem.” And that’s indicative of what’s going on at all levels of government, because they don’t understand the monetary system.”

Unidentified: “But this is more than hypothetical, more than just political, we are talking economic. Income inequality is an economic issue that is challenging… In my opinion, it’s one of the biggest challenges to our democracy.”

Warren Mosler: “Right. But what I’m saying is it’s not getting the attention it deserves because they’re worried things that shouldn’t be getting any attention. We’re not going to get attention to those issues until we get rid of the things that are taking all of our attention, like China, and the budget deficit. If we stop thinking about those, we’d have time in Congress to talk about something else.”

L. Randall Wray: “I want to add a couple of things. So, we’re arguing taxes drive money, taxes don’t pay for government spending. So that’s the fundamental point. And then the question is, “What kind of taxes?” And Warren said the head tax is actually the best thing to drive currency from inception. But once we–“

Warren Mosler: “I said it’s the easiest thing to understand.”

L. Randall Wray: “It’s also the best thing to drive it. But once we’ve got a monetary economy, then we can use an income tax, we can have an inheritance tax, and so on. So then the question is, “What other things can taxes do?” And so yes, we use taxes to punish certain kinds of behavior, “bads.” And then we can use tax breaks to encourage other kinds of behavior. We could use inheritance taxes to try to prevent accumulation of dynasties of wealth. We could try to use taxes to address income inequality. One word that you said that I don’t like is “redistribution” because we can always raise the income of people at the bottom, without taking from income at the top. The reason is because we don’t really take income and give it, because taxes don’t pay for the government spending. We can always have as much welfare as we want without taxing the rich at all.

“Then just the final point I would make, I’ll just state it as a claim, and I think that you said this: in fact, taxes never reduced income at the top. It does not work. They have too much political power. They get the exceptions written into the tax laws. So you never achieve the 50% tax rates on the rich. So we should think about a different way to prevent income inequality, I don’t think the tax system will work. Prevent the income in the first place, that’s the best way to do it.”

The next issue raised was how there could be a stronger voice out there to spread the word about MMT. Marshall Auerback then proceeded to outline what MMT advocates had been doing up to that time to get MMT views “out there.” I'll leave you to read that exchange in the transcript. But since the FS conference, efforts to spread the word have accelerated along with the number of people blogging about MMT and the number of MMT videos and presentations being created. In the two years since the conference, MMT has received some mainstream attention, some of it dismissive; some of it favorable, but either way the frequency and intensity of MMT-related communications seem to be increasing exponentially.

The Q & A session ended with this statement of Roger Erickson's

Roger Erickson:

“I want to get back to the question that was raised by the person that was behind me, “How do we protect our systems against these kinds of disconnects?” And actually, if you go outside the narrow field of economics, there is very rich literature on this very question. If you look at the field of ecology, systems theory, anthropology, many others, and all the way up to military operations, there are literally thousands of tomes and books and theories, mathematical models, physics models written about this, and what ties them all together is system stability. So eventually, as people are saying, we’ll wake up and we’ll realize that things are going south. The general response about how you protect it is, the simple answer is, that in any complex system, what keeps system stability is eventually interaction, and the knowledge throughput, the data shared throughout the system.

“So the simple mantra that comes out of this is “Interaction drives awareness.” Until we have more crosstalk among these different professions, our electorate and our elected officials are not going to have a general consensus on it.”

LetsGetItDone Comment: I think this comment is very important because it emphasizes the complex adaptive system context of macro-economics, and also suggests that spreading the MMT paradigm in such a way that it can replace the destructive neo-liberal paradigm may well depend on our creating new systems of interaction that allow both distributed problem solving and rapid communication of the new knowledge created to all in the complex adaptive system who need it. Roger Erickson

posted more on interaction and awareness very recently,

and I've done some posts on this in the series ending

here, as well.

Conclusion

In the introduction, I pointed out that Warren's presentation refutes a large number of popular austerian myths including: the government is running out of money; the Government can only raise money by taxing or borrowing; We can't keep adding additional debt to “the national credit card”; We need to cut spending and entitlements; our main creditors, like China will cease to buy our debt making it impossible for us to raise money; our grandchildren must have the heavy burden of paying our national debt; Government deficit spending isn’t sustainable because the Government is like a household and that since households sacrifice to live with their means, Government ought to do that too; and “printing money,” i.e. deficit spending without selling debt instruments in corresponding amounts is necessarily inflationary. These myths are at the heart of the austerian message being delivered by the deficit hawks and the whole range of Peterson efforts including his annual fiscal summit conferences.

So, the importance of Warren's presentation to the counter-narrative cannot be over-estimated. His refutation of so many myths, along with his placing them in the context of both the buckaroo experiments and so many real world events, provides a great deal of the counter-narrative needed to defeat the austerian paradigm and adopt a more rational economics as the framework for policies that will help us build a society that delivers social justice, and turns away from plutocracy and back towards democracy.

The presentation and Q & A thereafter also reinforce the aspects of the counter-narrative given previously by Bill Mitchell and Stephanie Kelton, so all three together provide a coherent view in opposition to the Peterson/neoliberal line, showing that there is no fiscal sustainability problem for the US in the sense that insolvency can involuntarily happen because of accumulated debt or present deficit spending. Instead, if there is any REAL fiscal sustainability problem at all it lies with the possible effects of government austerity, since it can reduce the room for future deficit spending by destroying real private sector productive capacity, so that fiscal efforts produce inflationary effects sooner then they would have, before austerity was implemented.

In Part Five I'll cover Marshall Auerback's presentation on “Inflation and Hyper-inflation.” We'll see how his version of the MMT counter-narrative strengthens and extends what we've already learned from the proceedings of the first three sessions of the Teach-In, while also responding to one of the most common attacks on MMT, which is: “OK, OK, so there is no solvency problem, but continued spending and “printing money” will surely lead to the kind of hyperinflation we've seen in Weimar and Zimbabwe, so we still can't keep on running deficits. Marshall's presentation will directly confront that very popular criticism.

(Cross-posted from Correntewire.com)