As a former venture capital investment professional, I am disappointed by the recently released transcript of Mitt Romney’s 1991 statements, in which he discusses the “expert” valuation analysis he performed as part of Staples founder Tom Stemberg’s divorce proceedings. Looking at his statements in the context of the historical business performance metrics presented in the amended S-1 filing made by Staples in April 27, 1989, at the time of its IPO, cast doubts on Mitt Romney's statements as to the fair market value of Staples over the period in question.

Imagine if you invested in a retailer in September, 1987 that had $8.8 million of revenue, $1.8 million in gross margin, a footprint of 3 stores in the fiscal year ending May 2, 1987 and saw it grow dramatically to $39.7 million in revenue, $8.6 million in gross margin, and a footprint of 16 stores by April 30, 1988. While the net loss increased, that was driven by growth in store opening expenses, pre-store opening expenses, the opening of a distribution center (all costs associated with supporting rapid growth). Now, imagine that company was positioned for continued growth (and, in fact, had more than double the revenue in the first 9 months of the next fiscal year as it did in the entire fiscal year ending April 30, 1988). In Romney’s statements, he used the initial purchase price of the stock priced in September, 1987 as the baseline with which to value the stock as of February of 1988. He was even asked, point-blank, whether the stock increased in value during this period and he said it did not!

Q. Did the value change appreciably in your opinion between September [1987] and February of '88?

A. It did not change appreciably during that period, no.

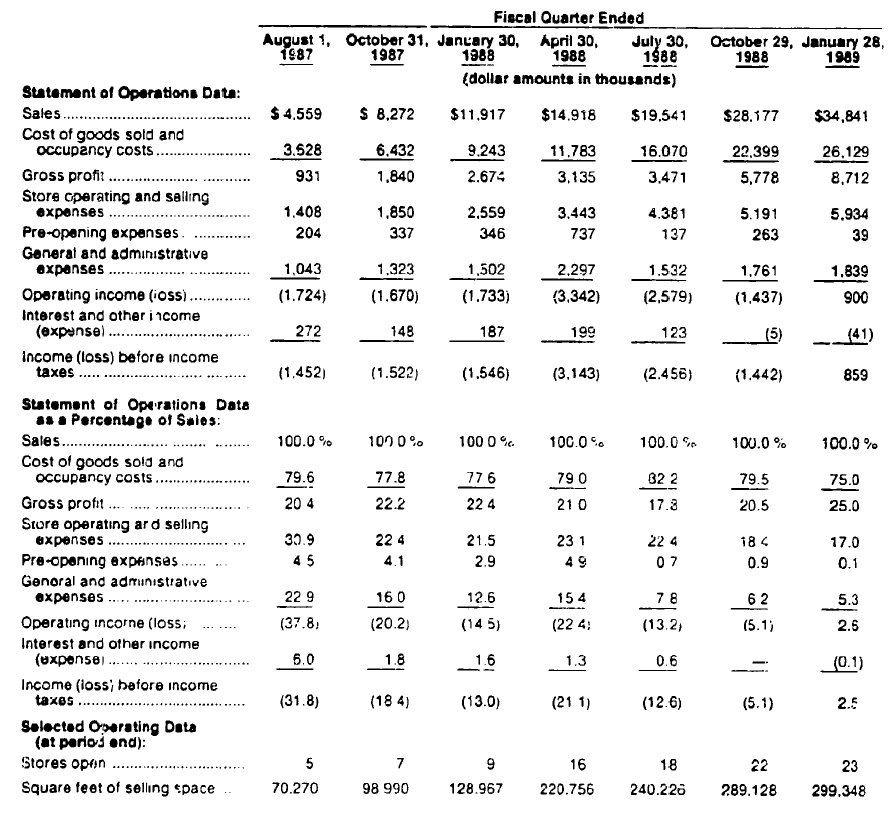

The S-1 makes it clear that the company was growing considerably each quarter during that period. In the quarter ending in August 1, 1987 (the quarter immediately prior to the offering), the company had revenue of $4.6 million; the quarter ending on October 31, 1987 saw revenue of $8.3 million; and, there was $11.9 million of revenue in the quarter ending January 30, 1988. There were also QoQ increases in gross margin percentage in each of those quarters. Below is the full table of quarterly performance around that period:

Even factoring in the declines in stock prices in October 1987, and the fact that the market had not fully recovered by February 1988, Staples considerable growth likely more than offset any decline in comparable retail valuation multiples over the period. Romney argued that such an analysis, where valuation multiples of similar companies are applied to actual business performance metrics to price the company being valued, is inappropriate to the situation given that the last transaction was priced as recently as the prior September. However, given the material change in business performance over the period, and the substantial change in overall market conditions, looking at a comp analysis would have been very useful and informative in this situation.

While there is no clear “smoking gun” in Romney’s recently released statements, his claim that the company had not increased in value between September 1987 and February 1988 is dubious and his refusal to consider an analysis of comparable company multiples is questionable.

UPDATE: Romney Transcript Link on TMZ