Have you noticed the recent roller-coaster ride in the Stock Market?

Have you any idea what's behind it?

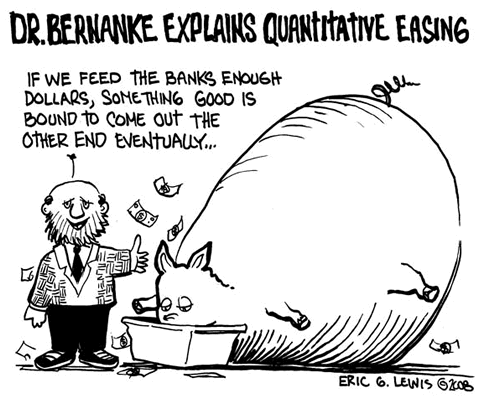

Well, not much except the Federal Reserve Chairman Ben Bernanke suggesting (and then later un-suggesting) that he might soon dial back his third round of Quantitative Easing (QE).

Institutional Investors like Ease; and they were not well pleased -- initially. ... SO the Fed recanted his warnings -- and as a direct result the Dow sets new record highs.

Strange animal -- this roller-coaster that gets built day-by-day. That reservoir of wealth, upon which so many future dreams, go along for the ride ... if you have a 401k or a Pension plan, well hold on your future hats.

Here's how Round Three QE quietly began last September ...

Begin Quantitative Easing, Phase III

Fed Undertakes QE3 With $40 Billion Monthly MBS Purchases

by Joshua Zumbrun, Bloomberg.com - Sep 13, 2012

The Federal Reserve said it will expand its holdings of long-term securities with open-ended purchases of $40 billion of mortgage debt a month in a third round of quantitative easing as it seeks to boost growth and reduce unemployment.

[...]

Stocks jumped, sending benchmark indexes to the highest levels since 2007 [...]

“Open-ended purchases of mortgage-backed securities will politicize the Fed and add substantially to its balance sheet risks, but it will not help our economy’s long-term growth prospects,” Corker said.

[...]

The Fed has argued he is doing this to promote

Job Growth -- which is among the goals of its multi-pronged

mission: promote full employment.

Fine, but what exactly happens when the Federal Reserve 'buys mortgage debt' anyways? Why is the buy-back program shrouded in so much free market-mystery?

Is there a 'yard-sale' somewhere where I can buy a MBS home on the cheap, from the Fed?

Is there a ghost town of properties just waiting to be flipped? or demolished? or rented? Or maybe even loaned out to the homeless?

Inquiring minds should want to know ...

FAQs: Agency MBS Purchases

New York Federal Reserve -- data.newyorkfed.org

The following frequently asked questions (FAQs) provide further information about the Federal Reserve's additional asset purchases of agency mortgage-backed securities (MBS) announced by the Federal Open Market Committee (FOMC) on September 13, 2012, and the reinvestment of principal payments from agency securities.

Effective September 13, 2012

[...]

Who is eligible to transact in agency MBS with the Federal Reserve?

The New York Fed's primary dealers are eligible to transact in agency MBS directly with the Federal Reserve. Primary dealers are expected to submit bids or offers for themselves and for their customers.

How will agency MBS transactions be conducted?

Agency MBS transactions will take place in the secondary market through a competitive bidding process and in line with standard market practices. At this time, the Desk plans to continue to conduct agency MBS transactions over TradeWeb's electronic trading platform, though trading may occur by other means if desirable.

[...]

Will the Federal Reserve use investment managers, or other vendors, to conduct agency MBS transactions?

The New York Fed will use internal staff to execute agency MBS transactions. Wellington Management Company will continue to provide investment management services and JPMorgan Chase will continue to provide custodial services.

[...]

How are the Federal Reserve's agency MBS holdings reported?

Agency MBS transactions are reported after settlement occurs on the H.4.1. statistical release titled "Factors Affecting Reserve Balances of Depository Institutions and Condition Statement of Federal Reserve Banks." This report also includes information on total outstanding commitments to buy and sell MBS in a supplemental table entitled "Supplemental Information on Mortgage-Backed Securities." Trade settlements may occur well after trade execution due to agency MBS settlement conventions. [...]

OK, this FAQ raises a few more questions, than it answers. For instance:

-- Who are these “primary dealers” with whom the Fed "transacts with" for mortgage-backed securities?

-- What is “the Desk” the Fed keeps talking about?

-- Where are these "Reports" which document the Fed's buyback "agency MBS holdings"?

Inquiring economically-literate minds should want to know ...

First the easy QE question -- the Fed's MBS report:

The Fed's Transparency Report

Federal Reserve Banks -- www.federalreserve.gov

FEDERAL RESERVE statistical release

H.4.1

1. Factors Affecting Reserve Balances of Depository Institutions

Millions of dollars --

Week ended

Averages of daily figures Jul 10, 2013

Reserve Bank credit 3,456,317

Securities held outright (1) 3,225,347

U.S. Treasury securities 1,948,028

[...]

Federal agency debt securities (2) 69,180

Mortgage-backed securities (4) 1,208,139

[...]

Net portfolio holdings of Maiden Lane LLC (8) 1,414

Foreign currency denominated assets (14) 23,170

Gold stock 11,041

[...]

Treasury currency outstanding (15) 45,167

[...]

4. Guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. Current face value of the securities, which is the remaining principal balance of the underlying mortgages.

[...]

3. Supplemental Information on Mortgage-Backed Securities

Millions of dollars

Account name Jul 10, 2013

Mortgage-backed securities held outright (1) 1,208,152

Commitments to buy mortgage-backed securities (2) 106,766

Commitments to sell mortgage-backed securities (2) 200

[...]

1. Guaranteed by Fannie Mae, Freddie Mac, and Ginnie Mae. Current face value of the securities, which is the remaining principal balance of the underlying mortgages.

2. Current face value. Generally settle within 180 days and include commitments associated with outright transactions, dollar rolls, and coupon swaps.

Those are millions of millions, by the way -- or in other words $1.2 Trillion of "agency MBS holdings" so far, as of this week's QE3 tally.

And what is this “the Desk” the Fed keeps talking about?

The Desk

The Announcement Effect:

Evidence from Open Market Desk Data (pdf)

New York Federal Reserve -- newyorkfed.org

[...]

Most of the time, open market operations conducted by the Trading Desk of the Federal Reserve Bank of New York (“the Desk”) are designed to accommodate variations in the reserve needs that stem from a variety of factors, such as changes in currency holdings, float, and large Treasury balances; to manage currency in circulation; and to accommodate other variations in the supply of reserves

Who are is these “primary dealers” the Fed keeps talking about?

The Big Banks Expect Quantitative Easing Into Early 2014

Business Insider -- 01/04/2013

[...]

The New York Fed’s primary dealers, the 21 banks with which it carries out transactions, expect quantitative easing to continue until 1Q 2014. This is according to a Dow Jones Business News report. The primary dealers’ median expectation is that the Fed will continue to purchase $45 billion worth of Treasuries each month throughout 2013, and cut that to $35 billion per month in early 2014. These findings come from a survey of primary dealers that was conducted before the December FOMC meeting. [...]

Do these “primary dealers” on the receiving end of the Fed's charity revolving line of credit, do they have names?

Primary Dealers List

New York Federal Reserve -- newyorkfed.org

Primary dealers serve as trading counterparties of the New York Fed in its implementation of monetary policy. [...]

Bank of Nova Scotia, New York Agency

BMO Capital Markets Corp.

BNP Paribas Securities Corp.

Barclays Capital Inc.

Cantor Fitzgerald & Co.

Citigroup Global Markets Inc.

Credit Suisse Securities (USA) LLC

Daiwa Capital Markets America Inc.

Deutsche Bank Securities Inc.

Goldman, Sachs & Co.

HSBC Securities (USA) Inc.

Jefferies LLC

J.P. Morgan Securities LLC

Merrill Lynch, Pierce, Fenner & Smith Incorporated

Mizuho Securities USA Inc.

Morgan Stanley & Co. LLC

Nomura Securities International, Inc.

RBC Capital Markets, LLC

RBS Securities Inc.

SG Americas Securities, LLC

UBS Securities LLC.

New primary dealers will begin transacting with the New York Fed upon completion of legal, operational and technical setup.

Designation of an entity as a primary dealer by the New York Fed in no way constitutes a public endorsement of that entity by the New York Fed, nor should such designation be viewed as a replacement for prudent counterparty risk management and due diligence.

SO, what does this all mean? -- this 3rd round of Fed Quantitative Easing,

that can turn markets on a dime; that gives those MBS toxic mortgage owners, 'a buyer of last resort' --

still. Even after those two record-setting Wall Street Toxicity bailouts, that have

already been paid by the U.S. Taypayers.

The Agency Mortgage-backed securities

What the Fed Move Means

by Joe Light, wsj.com -- Sep 21, 2012

[...]

The Fed says it plans each month to buy $40 billion of agency mortgage-backed securities, which are supported by government-sponsored enterprises such as Fannie Mae and Freddie Mac. The Fed says the buying will continue until the labor market improves substantially.

Unlike mortgage-backed securities that hold jumbo or subprime loans, agency mortgage-backed securities carry at least the implicit backing of the government. That means that if the home market soured and owners defaulted on their loans, mortgage-bond holders would still get their money back.

[...]

If the American People, by virtue of the Federal Reserve, are quietly being made the 'bag-holders last resort'

-- So, who are the 'bag-sellers' of last resort, receiving so far $1.2 Trillion in Round Three compensation, from the People's representative?

Who are these "mortgage-bond holders" that keep tossing the Fed (ie. us, "the guarantors of Fannie Mae, Freddie Mac, and Ginnie Mae" buybacks) -- all these MBS 'hot potatoes' -- that no one cares to hold -- still?

In other words, who are these high-rollers in the wall street woodwork ...

The MBS Mortgage Bondholders

Mortgage Bondholders Get Legal Edge, Buybacks Seen

by Reuters, news.investors.com -- 07/22/2010

[...]

U.S. mortgage bond investors have quietly banded together to gain the long-sought power needed to challenge loan servicers over losses the investors claim resulted from violations in securities contracts.

A group holding a third of the $1.5 trillion mortgage bond market has topped the key 25% threshold for voting rights on 2,300 "private-label" mortgage bonds, said Talcott Franklin, a Dallas-based lawyer who is shepherding the effort.

Reaching that threshold gives holders the means to identify misrepresentations in loans, and possibly force repurchases by banks, he said.

[...]

...

Or repurchases by the Fed, as the case has now turned out to be.

You see, that accountability 'audit trail' on these MBS "mortgage-bond holders" can be bit hard to untangle.

In the recent MERS-era of no rules followed, no local fees paid, no clear Chain of Title established,

-- in that anything-goes era, such tedious chores of liability record-keeping was kind of handed off to the signators of Foreclosure Document Mills, and the Collateral-Risk-swappers who dominated those boom-days.

The refrain of the day was "No one will notice. And besides no one's is guarding the farm ... except for us, the oh-so clever free-market foxes" ...

The MBS Trustees and Trustors

Mortgage bondholders gain key ally in putback fight

by Tom Hals, Reuters -- Mar 15, 2011

U.S. banks may be turning on one another in the legal battle over losses on mortgage-backed bonds.

Big pension funds and other investors are demanding compensation from banks that sold them supposedly low-risk mortgage-backed bonds that disintegrated in the housing crisis, a fight that ultimately could cost Wall Street $100 billion or more.

One big legal obstacle for investors has been getting documents they say will prove those bonds were anything but low-risk. Demands for documents have to come from the trustees who administer the bonds, and until recently trustees have stayed out of the legal fray.

[...]

The legal battle is complex, in part because the trustees themselves are often from big Wall Street banks, such as Wells Fargo, Citigroup and Deutsche Bank (DBKGn.DE), which also sold mortgage-backed bonds that went bad.

[...]

Mortgage bonds were at the heart of the financial crisis. Banks and mortgage companies such as Countrywide assembled the bonds from pools of thousands of home loans, often "subprime" mortgages with high rates of default. The loans were placed in trusts, which in turn issued bonds, some portions of which were given top-quality ratings.

If investors can get documents such as credit reports, details on borrowers' reported income and home appraisals, they expect to prove that banks breached their own guidelines for writing mortgages.

[...]

Fast forward to today. NOW those MBS-burdened U.S. banks are just 'turning' to

the Fed instead, lobbying them to continue to back-fill

their 'breach' of sound business practice; just for another 6-18 months, or so.

Wink, wink.

Afterall it would be SOOOO counter-productive for those “21 primary dealers” -- to sue each other into oblivion, wouldn't it? They found another eazy-mark to off-load their bad-assets to; someone who would quietly pay off their bad gambling debts, month after month. SOOO that they could survive to "invest" again, another grand free-market hey-day ... someday soon.

"It's Simply Priceless!" ... as the dispensers of consumer credit often remind us.

What in the world would we do without them? Without all their creative, cross-dealing, risk-shunning "financing"?

Maybe WE -- the aspiring home owners -- would actually live to survive, another roller-coaster building day ... without them, constantly re-leveraging our futures in their never-ending money-changing card games ...

We the Wall Street Bag-holders of Last Resort ...

Someday, may we no longer -- fill their bill ...