Freddie Mac reported today that 30-year mortgage rates have hit 6-month highs.

(Bloomberg) -- Fixed U.S. mortgage rates jumped to the highest level this year, signaling the Federal Reserve’s plan to lower borrowing costs has stalled.

The average 30-year rate rose to 5.29 from 4.91 percent a week earlier, Freddie Mac, the McLean, Virginia-based mortgage buyer, said today in a statement.

...

"That’s quite a jump," said Donald Rissmiller, chief economist at New York-based Strategas Research Partners. "The more rates go up, the more we need home prices to go down to equalize consumers’ payments. It’s those payments that have brought about a level of stability in housing unit sales."

This is despite, or maybe because of, the Fed's massive monetization of bonds. The interest rate of 10-year Treasuries and Fannie Mae mortgage bonds are higher now than when the Fed began its intervention in the market.

Fannie Mae and Freddie Mac are government-chartered mortgage companies that are being supported by $400 billion of backup taxpayer capital. The Fed has bought a net $507.1 billion of mortgage bonds so far, including $25.5 billion in the week ended May 27, according to Bloomberg data.

After Fannie and Freddie were nationalized, our Asian creditors became net sellers of those agency bonds. However, this doesn't explain why Treasury rates are higher.

What does explain it is the massive deficit spending around the world.

As governments worldwide try to spend their way out of recession, many countries are finding themselves in the same situation as embattled consumers: paying higher interest rates on their rapidly expanding debt.

...

Even a single percentage point increase could cost the Treasury an additional $50 billion annually over a few years — and, eventually, an additional $170 billion annually.

This could put unprecedented pressure on other government spending, including social programs and military spending, while also sapping economic growth by forcing up rates on debt held by companies, homeowners and consumers.

"It will be more expensive for everybody," said Olivier J. Blanchard, chief economist of the International Monetary Fund in Washington. "As government borrowing in the world increases, interest rates will go up. We’re already starting to see it."

Since the end of 2008, the yield on the benchmark 10-year Treasury note has increased by one and a half percentage points, rising to 3.54 percent from 2 percent, the sharpest upward move in 15 years. Over the same period, the yield on German 10-year bonds has risen to 3.57 percent, from 2.93 percent. And British bond yields have increased to 3.78 percent, from 3.41 percent.

It's simply a matter of supply and demand. The more debt that nations issue, without an increase in demand, means the price of that debt falls. In the bond market, price and interest rates are directly inversely related.

The governments of America, Britain, Japan, and elsewhere have tried to compensate for that dearth in demand by monetizing the debt. However, that caused the other supply and demand problem - more money printing without more goods means the value of the currency drops.

In 2009 and 2010, Washington will sell more than $5 trillion in new debt, according to Citigroup. A decade from now, according to the Congressional Budget office, Washington’s outstanding debt could equal 82 percent of G.D.P., or just over $17 trillion.

...

"It’s an exaggeration of course, but it’s a little like what happened to the subprime borrowers," Mr. Rogoff said. "People are just assuming the funding will always be there."

On the demand side of this issue is the simple lack of enough capital in the world. Bill Gross of Pimco had this to say on the matter.

The immediate question is who is going to buy all of this debt? Estimates suggest gross Treasury issuance of up to $3 trillion this calendar year and net offerings close to $2 trillion – almost four times last year’s supply. Prior to 2009, it was enough to count on the recycling of the U.S. trade/current account deficit to fund Treasury borrowing requirements. Now, however, with that amount approximating only $500 billion, it is obvious that the Chinese and other surplus nations cannot fund the deficit even if they were fully on board – which they are not. Someone else has got to write checks for up to $1.5 trillion additional Treasury notes and bonds.

Gross goes onto say that if the governments continue to try and spend our way out of the recession there are only two possible outcomes: 1) an immediate and enormous rise in interest rates, or 2) massive debt monetization by the central banks.

It appears that, because of a lack of clear vision and plan, we are seeing a combination of those two things. No one wants to make the tough choices, thus we will get a little bit of all the possible problems.

Trying to make 2 plus 2 equal 5

"The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin. But both are the refuge of political and economic opportunists."

- Ernest Hemingway, "Notes on the Next War: A Serious Topical Letter" , 1935

All sorts of justifications have been made for the massive federal deficit spending. People with a superficial understanding of Keynesian economics think that all deficit spending in a depression is good.

These people ignore a) Keynes advocated targeted countercyclical deficit spending designed to increase demand, not just any deficit spending, b) Keynes' theories were proven inadequate by the stagflation of the 1970's, and c) deficit spending is what got us into this mess. Is it logical to think that more of the same can be expected to get us out of it?

On the other end of the curve are the opportunists, who look at federal deficit spending as an opportunity to make a profit. These people ignore the damage done to the economy and currency by runaway deficits far outweighs any potential profits.

These discussions ignoring the glaring truth of what we are facing - the sheer size of the deficit spending precludes it from working.

We are failing to see the forest through the trees.

If this was a horror movie we would be guilty of worrying about a relationship problem instead of focusing on the axe murderer in the next room. If this was a car crash we would be guilty of worrying about our auto insurance rather than focusing on surviving the crash.

The Big Picture: 2 plus 2 still equals 4

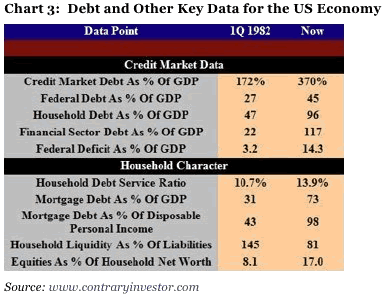

The country was more than 200 years old before America's public debt hit $1 Trillion. It hit $6 Trillion in early 2002, and then $10 Trillion in 2008.

By the end of this year it will climb over $13 Trillion. The CBO estimates nearly $10 Trillion in new debt by 2019. In economics this trend is considered "parabolic", and all things that go parabolic are unsustainable.

It begs the question - where will the money come from?

Sometimes people ask that question, which is a very good question, but stop there.

An even better question to ask is - is there enough money?

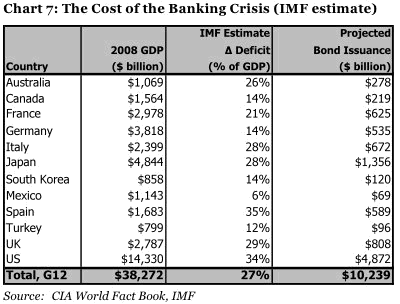

The IMF, which has repeatedly underestimated the economic crisis, has produced some numbers which are scary in and of themselves.

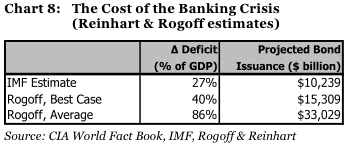

Fortunately, Carmen M. Reinhart and Kenneth S. Rogoff have studied dozens of historical examples since 1800 and tried to answer that question by basing it what that history teaches us.

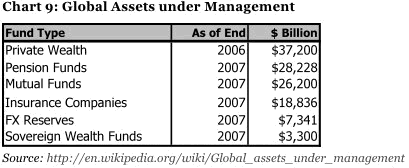

If you are like me, $33 Trillion are so far above my ability to imagine that they may as well be using another language. That's why it is important to put things into perspective by comparing this number to other asset classes.

If you understand the significance of these numbers you have arrived at the "Oh, shit" moment. The amount of money required to bail the world out of the current economic crisis, if this crisis plays out at a historical average, is nearly equal to all the private wealth currently in the world.

To repeat the obvious, this doesn't add up. What about the capital needed to fund the businesses of the world? What about the capital needed for private consumption?

Britain is trying to bail out their economy. The Euro nations are bailing out their economies. So is China and Japan. There isn't enough capital in the world for all these bailouts.

Kyle Bass from the US fund Hayman Advisors said the markets were choking on debt.

"There isn't enough capital in the world to buy the new sovereign issuance required to finance the giant fiscal deficits that countries are so intent on running. There is simply not enough money out there," he said. "If the US loses control of long rates, they will not be able to arrest asset price declines. If they print too much money, they will debase the dollar and cause stagflation.

"The bottom line is that there is no global 'get out of jail free' card for anyone", he said.

The numbers simply don't add up. Everyone can't do this at the same time. Two plus two are not going to equal five now matter how hard you try to make it happen.

To argue otherwise is to tilt at windmills.

There is no "what if". The odds of all this deficit spending getting financed at an affordable rate is zero. It's simply not going to happen. You can close your eyes and cross your fingers. You can pray to your gods. You can chant "I believe" all you want, but at the end of the day the laws of supply and demand will win as surely as Galileo's physics.

Once you wrap your mind around this horrible fact, you realize that we are in for a world of hurt.