Ever since Arthur Laffer doodled a parabola on a cocktail napkin in 1974, to the awed delight of Dick Cheney, Don Rumsfeld and Jane Wanniski, too many Americans have embraced the idea that cutting taxes, particularly on the wealthy, stimulates and grows the economy. Supply-side has become gospel truth for a good number of pundits, economists and Republican politicians seeking to gain or hold elective office.

But is it true? I thought April 15 might be a good date to look at some stats.

Please note: I am not an economist, econometrist or even that good at math. But I'm not an idiot.

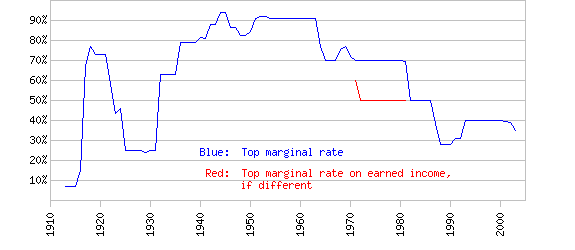

First, let's look at the top marginal tax rates over time. The table starts in 1913, the year the 16th Amendment was ratified and the federal government permanently authorized to tax American incomes. To make it easier to follow along, here's a graph of the year-by-year data in the table:

(from TruthandPolitics.org)

For the first four years after the 16th was ratified, federal tax on top incomes was relatively low, then more than quadrupled in 1917. Back then, the federal government held to the quaint idea that expenditures for wars were actual budgetary items.

After the Great War, top rates eased a bit, but stayed much higher than they'd started until the early-mid 1920s, when Republicans gained significant majorities in both houses in Congress and the White House. Predictably, top rates were cut dramatically. Still, with the rising incomes due to increasing consumer/industrial growth and stock prices, the federal government maintained a modest surplus in those years.

(Here's a handy little graph showing the US federal deficit from the turn of the 20th Century to the present for those who want to correlate between top margin tax rates, GDP growth and surplus/deficit states.)

Of course, when the stock market crashed in the midst of the 1920s banking crisis, real and artificial incomes withered, tax revenues plummeted and, with the federal government still stuck with such pesky tasks as maintaining the armed forces, building roads and trying to find some paying work for millions of citizens, the deficit soared.

The top marginal tax rates jumped in a somewhat futile attempt to close the budget gap. With the onset of another war, this one truly global in scope, deficits, and top rates, kept going up.

GDP growth, despite the astounding remobilization of the American productive base (plant + labor), wasn't great in the years during and just after the war, as we were mostly just building stuff to get blowed up. (Here's another handy chart, showing GDP in absolute and inflation (1983) adjusted dollars from the crash of '29 to 2004.) Top marginal tax rates also kept climbing, hitting 94% of earned income by war's end. Don't let anyone tell you the idle rich among the Greatest Generation didn't pull their weight.

After World War II, GDP didn't bust through the roof as you might expect, what with a lot of war debts to pay, a lot of returning warriors seeking non-existent housing and jobs and a general lack of demand for the stuff we'd been making (tanks, bombs, etc.). In fact, absolute GDP was markedly negative in the years just after the war (you guessed it, yet another handy chart). Top tax rates eased a little, but not much, hovering in the mid-80 percents.

Still, after the initial postwar recession, GDP grew steadily through the 50s and into the 60s, a time of growing, widespread prosperity for Americans, when the middle class expanded rapidly. Surely that was because of tax cuts for rich people, right?

Nope. As we entered the Golden Age of Ozzie and Harriet and drop drills, the top marginal rate actually went up, to its highest level in history, an amazing 91% and stayed there through 1963, when it dropped into the 70 percents, where it remained until a certain B-movie actor gained the White House and had his ear bent by a guy who'd drawn a stupid doodle on a cocktail napkin.

The top rates have been dropping like a rock ever since, except for a brief upswing in the 1990s (all hail Bill Clinton and, yes, Poppy "READ MY LIPS" Bush). Take a moment, if you're so inclined, to check back on those deficit numbers during that period.

Once Clinton was out of office, we all know what happened to tax rates for the rich, deficits and, eventually, growth. Ptoooie!

As I said at the beginning of this ramble, this is not my field. Heck, this field ain't even in my county!

That said, it doesn't take a Krugman to see that the top marginal tax rate has damn little to do with economic growth and a whole lot to do with federal receipts and the balance sheet (barring, of course, pesky little details like global war and economic collapse).

In fact, the argument could plausibly be made that the surest path to steady growth and economic stability is to return to the days of malt shops, Father Knows Best and taxing the living shit out of rich people.

Still, I'm not the stoutest of class warriors. I am susceptible to contrary facts, like this last handy chart showing the correlation of top marginal tax rates and GDP growth, both median and average growth rate per capita. That bit of data convinces me that, rather than returning to the days of Bel Airs and Big Bopper, when taxes on the rich were above 90%, we can settle on a nice, sweet spot where the richest pay between 60 and 75% of their income in taxes and we achieve a solid, steady 2.5 to 3% average growth rate.

Because, it turns out, big incomes are like big teenage boys. They have lots of strength and potential, but, unless forced to do real work (like income invested to avoid high tax rates), they just end up causing trouble for everyone.

There's my tax day screed. I know it's rather simplistic and ignores a lot of other variables, like domestic production with good wages protected by strong unions (I'll save that one for Labor Day) and the need to stabilize federal spending by not starting stupid, unnecessary wars (sounds like a good Veterans Day diary). Still, it's something to think about.