There’s been a lot of talk lately about a "credit crunch" in the financial markets. However, there really hasn’t been an explanation of exactly what is going on and why this is a bad thing for everybody. So, here is an explanation of what is happening along with a rudimentary diagram (forgive me, I’m not the greatest digital artist) to help explain the current structure of the credit markets and where the problems are.

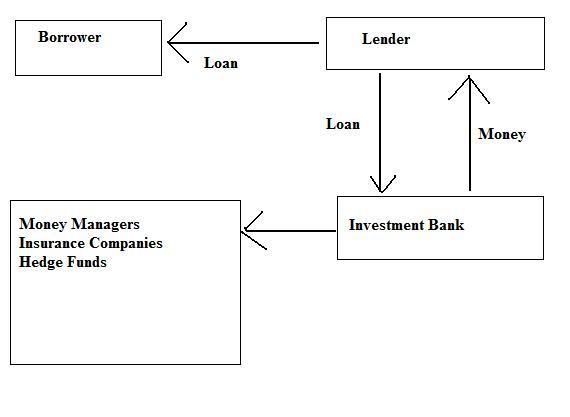

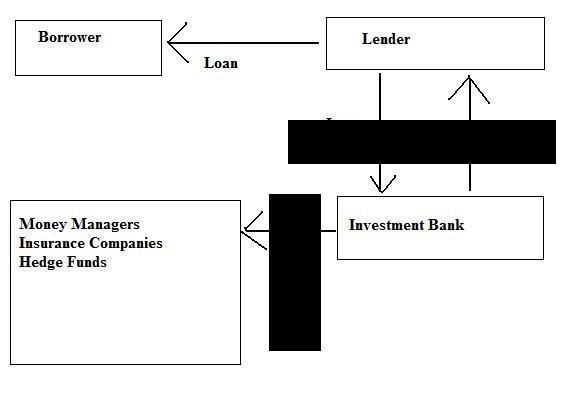

First of all here’s the diagram we’ll be working with:

However, to make this a bit easier, we’re going to break this down into a few smaller pieces.

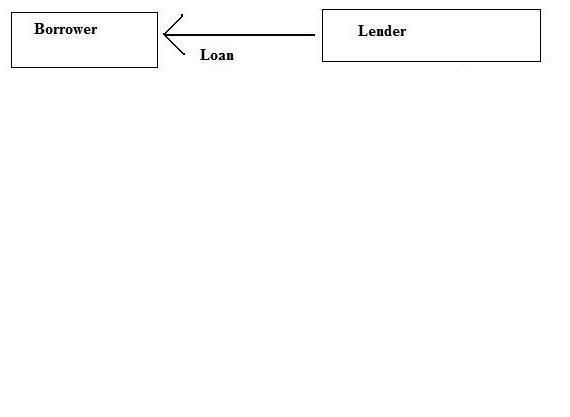

Let’s start at the beginning by looking at the top of the diagram.

Here we have a simple borrower and lender. The borrower goes to the lender and asks, "Can I borrow some money"? The Lender says, "sure", and makes a $100,000 at 5% loan for 30 years. We’ll assume this is your simple, run-of-the-mill mortgage.

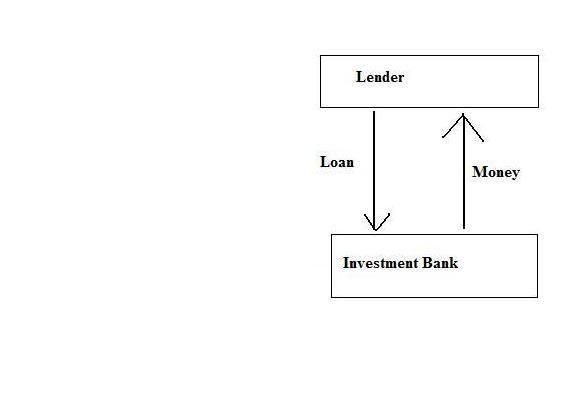

Now, the lender doesn’t keep the loan on his books. Instead, he sells them to an investment bank. The lender gets cash for the loan and the investment bank gets a mortgage. The investment bank then pools the mortgage with other similar mortgages. Remember at the beginning we got a $100,000 30-year loan at 5%. The investment banker will pool out loan with other 30-year, 6% $100,000 loans. Now we’re dealing with this part of the diagram:

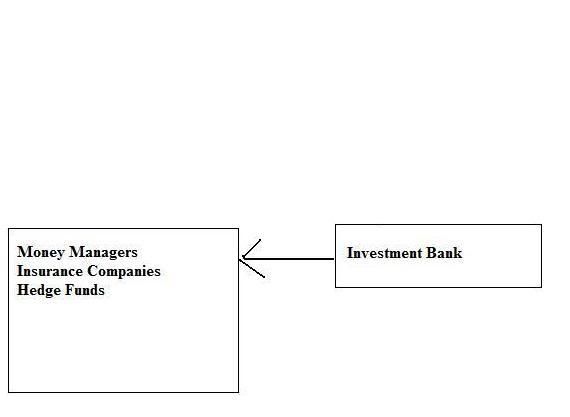

The investment bank then essentially makes a bond out of these pooled mortgages and sells these bonds to hedge funds, insurance companies, mutual funds and money managers who place the bonds in their portfolios. Now we’re in this part of the diagram:

OK – so what is happening in the credit markets right now? Investment banks aren’t buying loans. This part of the diagram is breaking down:

That means lenders – instead of getting money for the loans they make are having to keep the loans on their books. That also means that lenders can’t make as many loans. Investment banks area having a harder time selling loans/assets to money mangers, hedge funds and mutual funds. That means investment banks are having to keep assets on their books they would normally sell down the line. In short, the flow of funds throughout the financial system is at a standstill as all of the players reevaluate what they are doing.

In short, money is supposed to move pretty easily from the lender, through investment banks and into the portfolios of institutional investors. But that's not happening right now. The big guys are concerned about credit quality and excessive exposure to the subprime market. That's why they've stopped buying pooled mortgages.

So, instead of a nice flow of funds like the original diagram:

We get this:

This won't unfreeze until all of the players get a better handle on the amount of risk in the system. And that could take awhile.

Update [2007-8-13 8:47:54 by bonddad]:: A few people have asked the question, "what is a hedge fund". A hedge fund is essentially an unregulated mutual fund. They are unregulated because they are only sold to people who in theory don't need legal protection. These people are high net worth individuals ($1 million net worth, high annual income), corporations, partnerships and the like.

Actually, New Deal Decocrat offers a great explanation in a response below:

1. Hedge funds, as bonddad says below, are basically just unregulated mutual funds. Their investors are supposed to be large institutions and wealthy people (although $1million in investable funds - the minimum, isn't as wealthy as it used to be).

Hedge funds, unlike traditional mutual funds, can go both "long" (betting a stock price, for example, will increase) and "short" (betting it will decrease). Nowadays, though, hedge funds can pursue basically any strategy they want.

The theory is their investors are big,wealth Boyz and Girlz who ought to be able to decide for themselves how to risk their money.

2. One of the things hedge funds can do, is borrow money to make their investments. That's called "leverage." Let's say I think mortgage bond X, which is returning 5% interest, will increase in value, because prevailing interest rates will decline to 4.9%. That's a small return. So, I the hedge fund decide I want higher returns. So I borrow 4X the amount of my investment. If my bet is correct, I can collect 20% interest, and pay back the bank its principal (note: I'm really simplifying here, so my math may not be perfect).

All well and good. But suppose I bet wrong, and interest rates instead go up to 5.25%. Not only do I lose money, but my LOSS is also magnified 4x, and worse, I still owe ALL of the loan back to the bank.

Very bad.

Remember, that's the same situation that happened in 1929 with buying stocks on 90% margin. That is also the problem you've been reading about with a few hedge funds recently. Keep in mind that a lot of other hedge funds have "bet" correctly, and are making money.

3. If I'm a wealthy investor, how do I know that the hedge fund I'm in one of the hedge funds that is making money, or one of the ones that is about to blow up?

Answer -- the is the nub of the problem: I DON'T! Hedge funds, unlike mutual funds, don't have to frequently disclose their positions. So you really have no idea what your hedge fund manager has been doing recently with your money. Put yourself in the shoes of one of those big investors. How do you feel? A little queasy, maybe?

To make matters worse, a couple of the hedge funds that blew up have chosen to liquidate themselves in the Cayman Islands, which are notoriously friendly to managers as opposed to investors. So, by betting with other people's money, a successful hedge fund manager can make 20% a year; if he loses, he can liquidate in a friendly offshore court.

How do you feel now, Mr. and Mrs. hedge fund investor?

Conclusion: there are a lot of wealthy investors who don't know right now if they are making good money, or their assets are about to become worthless. Under such situations, a lot of people are going to get "cold feet" about loaning any more money to such risky ventures.