There's been a fair amount of debate about whether or not the Federal Reserve should start to cut the Federal Funds rate -- the rate banks charge each other when they borrow short-term loans. I have argued against this while (interestingly enough) "free market" conservatives have been arguing for a rate cut (help me -- I was really greedy and stupid and now I'm losing money). However, the central problem in the market isn't lack of funds: it's confidence. And there is nothing the Fed can do about this.

Here's the basic problem right now: even short-term commercial paper isn't getting traded. That means the really safe and conservative investors are balking at even some of the safest non-government investments out there:

From Bloomberg:

The $1.1 trillion market for commercial paper used to buy assets from mortgages to car loans has seized up just as more than half of that amount comes due in the next 90 days, according to the Federal Reserve. Unless they find new buyers, hundreds of hedge funds and home-loan companies will be forced to sell $75 billion of debt backed by mortgages, according to Zurich-based UBS AG, Europe's largest bank.

Those sales would drive down prices in a market where investors have already lost $44 billion, based on Merrill Lynch & Co.'s broadest index of floating-rate securities backed by home-equity loans. That may hurt the 38.4 million individual and institutional investors in money market funds, the biggest owners of commercial paper.

``We're dumping all this collateral into the market and it becomes a death spiral for the assets,'' said Brian McManus, head of collateralized debt obligation research at Charlotte, North Carolina-based Wachovia Corp., the fourth-biggest U.S. bank by assets. CDOs contain pools of mortgage securities that have been repackaged and sliced into pieces.

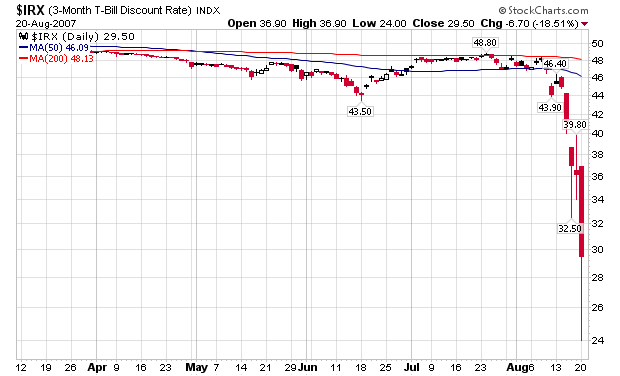

This is the big reason the Fed shouldn't lower rates. Just because banks have more money to lend doesn't mean they will be able to find borrowers or steer those borrowers to a certain type of asset. The bottom line is investors and borrowers aren't touching anything right now. No matter how much cash they have, they won't go near anything except T-Bills:

The bottom line is the only way for the system work is to let it feel the pain. And no -- I am not thrilled by that prospect. But the only way for anyone to learn their lessons right now is to let them learn their lessons:

AS CLSA's Wood put it last week in Greed and Fear, his investment letter: "It is crucial that market discipline is reasserted in the profligate behavior that had become commonplace in the credit world."

There's blame all around for this "profligate behavior." First, there's the mortgage banks that lent 100% of the purchase price of a home without demanding income and net worth statements from the buyer. Then there are the naive buyers who believed they'd get an easy ride on easy credit conditions.

Thirdly, there are the investment banks and commercial banks that gathered the lousy mortgages together and sold packages of them indiscriminately to investors. Finally, there are the rating agencies that were paid scads of money to give credit ratings without truly understanding the paper they were valuing.

This is an issue of confidence. The market doesn't have any right now and the Fed can't give it to the market. If they lower rates, all we're going to see is a further lowering of the short-end of the government yield curve. That's about it. No one has the confidence to move into the debt market right now -- and you can't make them.

For those of you who want to see a really funny argument, take a look at this from Crooks and Liars. Whenever anyone says "conservatives want the Fed to be their love monkey" I'm all ears. Thanks to John Campanelli below for the link.

New Deal Democrat also wrote a great article on this yesterday. Highly recomnmended.