A headline earlier this week hit me right in the gut. It read "Fed to Provide Up to $540 Billion to Aid Money Funds" and it got me to wondering what has come of the Fed's fiscal largesse over the last several months.

A headline earlier this week hit me right in the gut. It read "Fed to Provide Up to $540 Billion to Aid Money Funds" and it got me to wondering what has come of the Fed's fiscal largesse over the last several months. Most of us consider that it started when the Fed announced in mid March of 2008 that it would lend J. P. Morgan Chase upwards of $28 billion dollars to rescue Bear Stearns. In return, J. P. Morgan would provide some of the riskiest debt (Mortgage Backed Securities) from Bear Stearns as collateral for the loan.

The Fed's more aggressive action actually started a few months earlier in December, 2007 when the Fed announced its Term Auction Facility as a means to auction funds to depository institutions as a more aggressive means of injecting liquidity into the market. In the ensuing months, the Term Auction Facility that few outside of the financial community are aware of has grown to $263 billion.

Over the next few months the Fed launched several other isolated bailouts including $25 billion to rescue Fannie Mae and Freddie Mac in July, an $85 billion lifeline to AIG in September and then the mother of all rescues, the $700 billion TARP (Troubled Asset Recovery Program) to be thrown over this entire stinking mess.

Now we don't really know how the TARP is going to play out, because it will be released by Congress in tranches, allegedly the first $250 billion to be drawn immediately, followed by an additional $100 billion upon request by the President and the final $350 billion tranch upon ratification by Congress. So now it looks like the first $250 billion is to be used to recapitalize the nine major banks in the country (and presumably to line their acquisition war chests to acquire the less fortunate unrecapitalized banks).

So where is this new $540 billion to aid the money funds coming from? The simple answer is 'thin air'. The more complicated answer is federal sanctioned money printing presses.

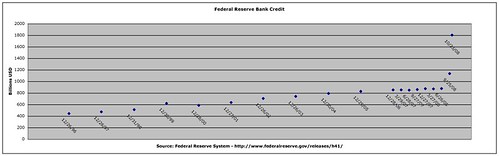

The Fed can issue unlimited amounts of credit, unlimited that is except for the fact that eventually devaluation hits the dollar like a bad tequila hangover and inflation launches for the moon. The Federal Reserve System publishes its weekly H.4.1 report that presents, as they refer to it, 'Factors Affecting Reserve Balances'. Without getting into the gritty details, let's focus on the top line number, a bucket known as 'Reserve Bank Credit' aka credit extended by the Fed. Looking at the statistics as far back as they are published on the web reveals that until very recently, Reserve Bank Credit has experienced a sleepy growth rate from just over $400 billion at the end of 1996 to $875 billion in June of this year. And then the Fed came to the rescue of the union. In the last two months, Reserve Bank Credit has exploded to $1,803 billion (1.8 trillion) ... doubling in 60 days time! To this, presumably this week's $540 billion will be added and who knows what they are going to throw in the pot next week.

I compiled a progressive time lapse look at the growth in Reserve Bank Credit, annually from 1996 through 2006, and then quarterly through September 2008, followed by the latest data point for October 23, 2008.

The chart, with its alarming 'hockey stick' slope is presented below.

Source: http://www.federalreserve.gov/...

OK. Point conceded. So the Fed has thrown some money at the problem. How bad can that be?

The short answer is 'Who knows?' I suspect the President's Plunge Protection Team would be unwillling to offer an answer at this point.

So I thought it might be instructive to compare the current levels of the Reserve Bank Credit with some other popular government statistics to see how it might stack up. Let's start with a deficit of $10.4 trillion where the RBC would represent 17.2%. Or the 2007 Gross Domestic Product of $13.8 trillion of which the RBC would represent 13%. Now neither of these are huge percentages, but as the accountants would say, they are material. And remember, the RBC is currently growing in leaps and bounds.

In comparison to the aggregate cost of the Iraq war at $565 billion, the RBC towers over it at 393%. And in comparison to the 2008 proposed federal budgeted receipts and expenditures, each in the range of $3.2 trillion, the RBC represents approximately 55% of those numbers.

But here is the final number we need to think about. Many people believe that the underlying cause of the need for this unprecedented level of intervention by the Fed is to prevent a domino like collapsing of the OTC derivatives obligations held by financial organizations world wide. According to the Bank for International Settlements, the total OTC derivative notational amounts (the amounts that come due when a contract is fulfilled) amounted to almost $600 trillion at the end of 2007 and they are most certainly larger today, but no one can say exactly how much. The $1.8 trillion band aid that the Fed has put on this economic mess represents a mere 0.3% of the OTC derivatives amount. If the OTC derivatives represents the threat, Federal Reserve Bank Credit certainly looks like an inadequate tool to address it.

It is time we start asking ourselves if the Fed can actually put out the fire with the tools that it has at hand. The full faith and credit of the United States government may hang in the balance.