Either we're in a recession or we're about to start one. Either way, the latest expansion is over. While there may be some question about when it happened (the expansion, that is) the reality is it was the least impressive expansion since WWII. Below I will explain why.

Before I move forward, let me address specifically any readers who still think the last expansion was "the Greatest Story Never Told." I am going to use facts to demonstrate why the latest expansion was terrible. If you don't like the facts please feel free to present you own facts. In fact, please do so. But please only use facts from reliable sources. Reliable sources would be the government agencies that collect and present this data. To sit at this table, you must bring data (properly adjusted for inflation) that is from sources used by all economists not from sources whose credibility is non-existant.

That being said (and I can't believe I even have to address this issue).

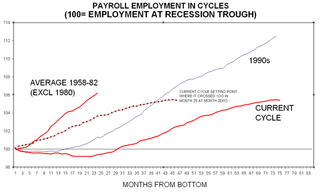

Let's start with the consumer side of the equation. First , job growth during this expansion is the weakest of any recovery since WWII. (This information comes from the National Bureau of Economic Research and the Bureau of Labor Statistics)

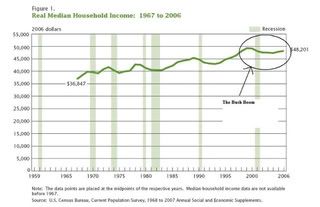

As a result, real median household income (income adjusted for inflation) is now lower than it was at the beginning of this expansion (this is the first time this has happened in 40 years) (This information comes from the Census Bureau).

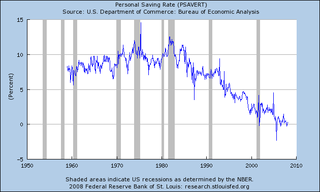

So -- where did the money for consumer spending come from? Part of it came from savings. Here is a chart from the St. Louis Federal Reserve of US national savings. Notice this number has been decreasing for the last 25 years and is currently hovering around 0%.

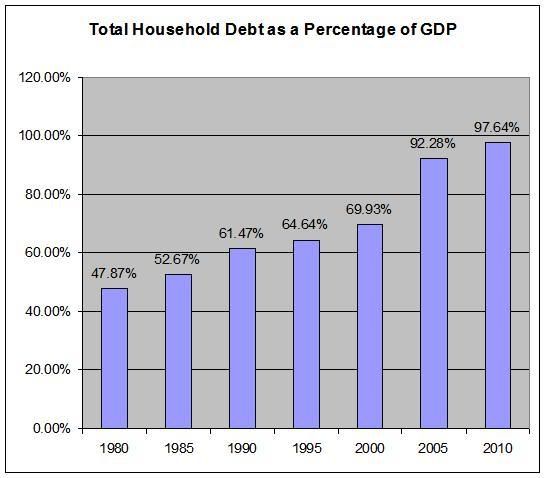

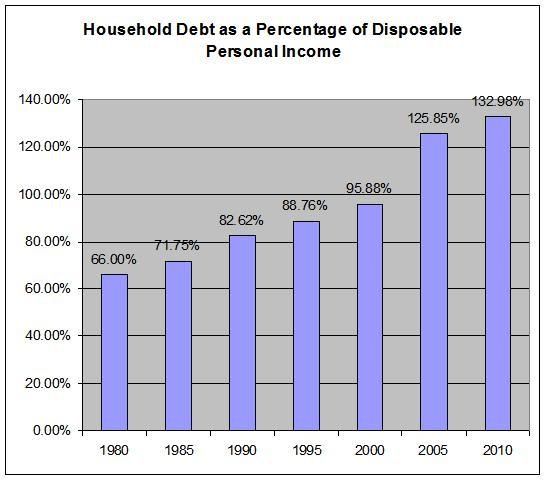

Debt is the real source of funds for this expansion (this information comes from the Federal Reserve's Flow of Funds report and the Bureau of Economic Analysis).

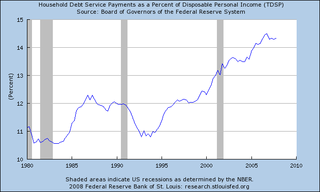

As a result of this increased debt load, a larger portion of consumer's income (which has been stagnant for this expansion) is going to debt payments:

So looking at the consumer we see the following picture emerge.

1.) Job growth was the weakest of any post WWII recovery.

2.) Real median income actually dropped for the duration of this expansion.

3.) To sustain consumption, consumers went on a mammoth debt acquisition binge, so that now

4.) Debt payments are as high as they have ever been on a percentage of disposable income basis.

So after 7 years of economic expansion we have lower incomes and more debt.

However, the consumer isn't the only person who ran up a ton of debt.

The Bush White House has again run up the national credit card. Here is a list of total debt outstanding at the end of the government's fiscal year:

09/30/2007 $9,007,653,372,262.48

09/30/2006 $8,506,973,899,215.23

09/30/2005 $7,932,709,661,723.50

09/30/2004 $7,379,052,696,330.32

09/30/2003 $6,783,231,062,743.62

09/30/2002 $6,228,235,965,597.16

09/30/2001 $5,807,463,412,200.06

09/30/2000 $5,674,178,209,886.86

The current debt outstanding is $9,437,425,175,221.31

Notice that since 2002 the Federal Government has issue over $500 billion of net new debt per year. And yet, we have continually been told the budget deficit is getting better. Let's ask a fundamental question: if you continually spent less than you made, would you have to borrow money?

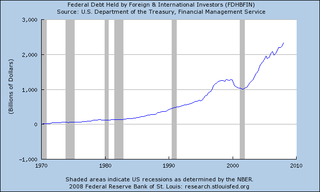

As the US has become more reliant on debt financing it has also become more reliant on foreign governments for its financing. Here is a chart from the St. Louis Federal Reserve of the total US debt held for foreign investors:

In short, growth at the national level is dependent on the issuance of debt. And we are now reliant on foreigners for an increasing percentage of our growth. A former Federal Reserve Chairman (Paul Volcker) explains why this is a bad development:

More recently, we've become more dependent on foreign central banks, particularly in China and Japan and elsewhere in East Asia.

It's all quite comfortable for us. We fill our shops and our garages with goods from abroad, and the competition has been a powerful restraint on our internal prices. It's surely helped keep interest rates exceptionally low despite our vanishing savings and rapid growth.

And it's comfortable for our trading partners and for those supplying the capital. Some, such as China, depend heavily on our expanding domestic markets. And for the most part, the central banks of the emerging world have been willing to hold more and more dollars, which are, after all, the closest thing the world has to a truly international currency.

The difficulty is that this seemingly comfortable pattern can't go on indefinitely. I don't know of any country that has managed to consume and invest 6 percent more than it produces for long. The United States is absorbing about 80 percent of the net flow of international capital. And at some point, both central banks and private institutions will have their fill of dollars.

Finally, the US trade deficit has exploded. Here is a chart of from the St. Louis Federal Reserve:

The St. Louis Reserve published a report in late 2006 that showed how important oil was to this figure. This indicates how important energy independence would really help with the trade deficit.

So let's sum up.

1.) The weakest job growth since WWII led to a declining median family income.

2.) In order to keep spending the US consumer continued to save less and borrow more.

3.) At the national level, the US government has issued over $500 billion dollars of net new debt per year since 2002. This has led to an increased reliance on foreign investors to finance our way of life.

4.) The trade deficit has continued to expand, although oil is responsible for a fair amount of that increase.

5.) In short, the US continues to consume more than it produces.

At some point, we will have to pay the bill.

This is the end result of the "Bush boom" or "the greatest story never told."

If the story was so great, we wouldn't need people to remind us of how good it is.